版权所有 © 2023 CDP Worldwide。保留所有权利。

2023年CDP水安全调查问卷预览和填报指南 - 版本控制

| 版本号

|

发布/修订日期

|

修订摘要

|

| 1.0

|

发布于:2023年1月11日 |

发布2023年调查问卷预览和填报指南。

|

请注意,您已经选择查看水安全问卷 - 完整版。

您已经选择查看以下行业的行业相关特定内容:

CDP披露周期-2023年

访问问卷预览、报告指南和评分方法

可以通过CDP网站的公司指南页面访问CDP的气候变化、森林和水安全企业调查问卷预览、报告指南和评分方法。

提交问卷回复。

调查问卷的回复必须通过CDP的线上回复系统(ORS)提交,该系统是CDP线上披露平台的一部分。请参阅使用CDP的在线披露平台了解更多详细信息。请注意,虽然问卷预览中的问题与在线回复系统(ORS)的相同,但其格式可能有所不同,特别是下拉选项和表格。

特定行业问题

高影响力行业内的公司除了回答一般问题外,还需要回答具有行业针对性的问题。已在相关行业简介内说明为各个行业开发精简调查问卷的基本原理。

向各公司分配的行业特定问题由CDP活动分类系统(CDP-ACS)确定。该系统通过关注公司的收入来源活动并将这些活动与气候变化、水安全和森林砍伐对公司业务的影响相联系,进而对公司进行分类。

请注意,由于每个问卷都包含特定行业问题,并非所有问题都适用于贵组织,因此可以跳过某些问题。

问卷的完整版和最简版

所有完成了气候变化、森林和水安全问卷的组织都可以进一步填写问卷的完整版。

在某些情况下,组织可以仅填写完成最简版问卷,其中包含的问题更少,且不涉及特定行业问题或数据点。

如果组织的年收入低于2.5亿欧元/美元*,并且这些企业是回复来自客户(即CDP 供应链合作伙伴), CDP 银行项目成员,RE100 倡议或者净零资产管理者(NZAM)倡议的邀请,那么他们将有资格填写简版问卷。

如果组织是受到投资者的邀请进行披露,则没有资格填写简版问卷。

有关评分资格及其影响的信息,请参阅评分简介。

* 对于之前已回复问卷的年收入低于2.5亿欧元/美元的组织,根据其对环境可能产生或已产生的影响,CDP将保留取消该组织填写最简版问卷选项的权利。

时间线:

2023年1月

|

- CDP网站发布2023年调查问卷预览和填报指南(英文版)。

|

| 2023年3月

|

- CDP网站发布2023年调查问卷预览和填报指南(翻译版)。

|

| 2023年4月

|

|

| 2023年7月

|

- 公司必须通过ORS向投资者和/或客户提交自己的回复,否则将无法取得评分资格以及(在适用时)被纳入报告中。

|

任何披露相关的咨询,请联系CDP帮助中心或您的CDP区域联系人。

CDP水安全调查问卷

本调查问卷是CDP Worldwide的财产,未经CDP Worldwide许可,禁止全部或部分(包括在软件平台内)复制。有关这方面的更多信息,请联系[email protected] 。

CDP水安全调查问卷简介

CDP利用透明化和问责制推动企业、金融市场和政府将增长表现与淡水资源耗减脱钩,并将资本朝向确保更高的水资源安全性的经济发展分配,以实现可持续发展目标。我们通过为投资者、客户和政策制定者收集有关公司管理、治理、使用和管理水资源的信息来实现这一目标。

CDP水安全调查问卷向CDP的数据用户和各个公司提供针对目前和未来水相关风险和机遇的深入分析。根据CDP的水资源评分方法学,本问卷还可以帮助公司改善水资源管理,并可以为企业提供给对标领先水资源管理实践的基准。

自2010年制定以来,水安全计划无论是在公司数量、资产价值还是要求数据的投资人和客户数量方面都取得了长足的发展。CDP现在拥有世界上最大型的公司水资源数据库,参与披露的公司数量达到前所未有的新高。

一般水安全调查问卷的结构

水安全调查问卷的结构和内容反映了企业水资源填报的发展趋势、对特定行业数据的需求演变、公共政策议程的发展以及与CDP的气候变化问卷和森林调查问卷更强的一致性。

模块结构整体反映了 CEO Water Mandate Guidelines的内容,帮助公司进行水资源管理并向投资者和政策制定者等提供相关数据。

包括签核在内,水安全调查问卷中有12个模块,另外还有一个供应链模块,仅提供给为CDP供应链项目的企业合作伙伴供给商品或服务的供应商。

CDP水安全问卷(一般行业版)包括以下内容:

- 水核算指标

- 价值链参与活动

- 业务影响

- 风险评估程序

- 风险、机遇及其应对措施

- 设施用水核算指标

- 水资源管理和商业战略

- 目标

- 核查

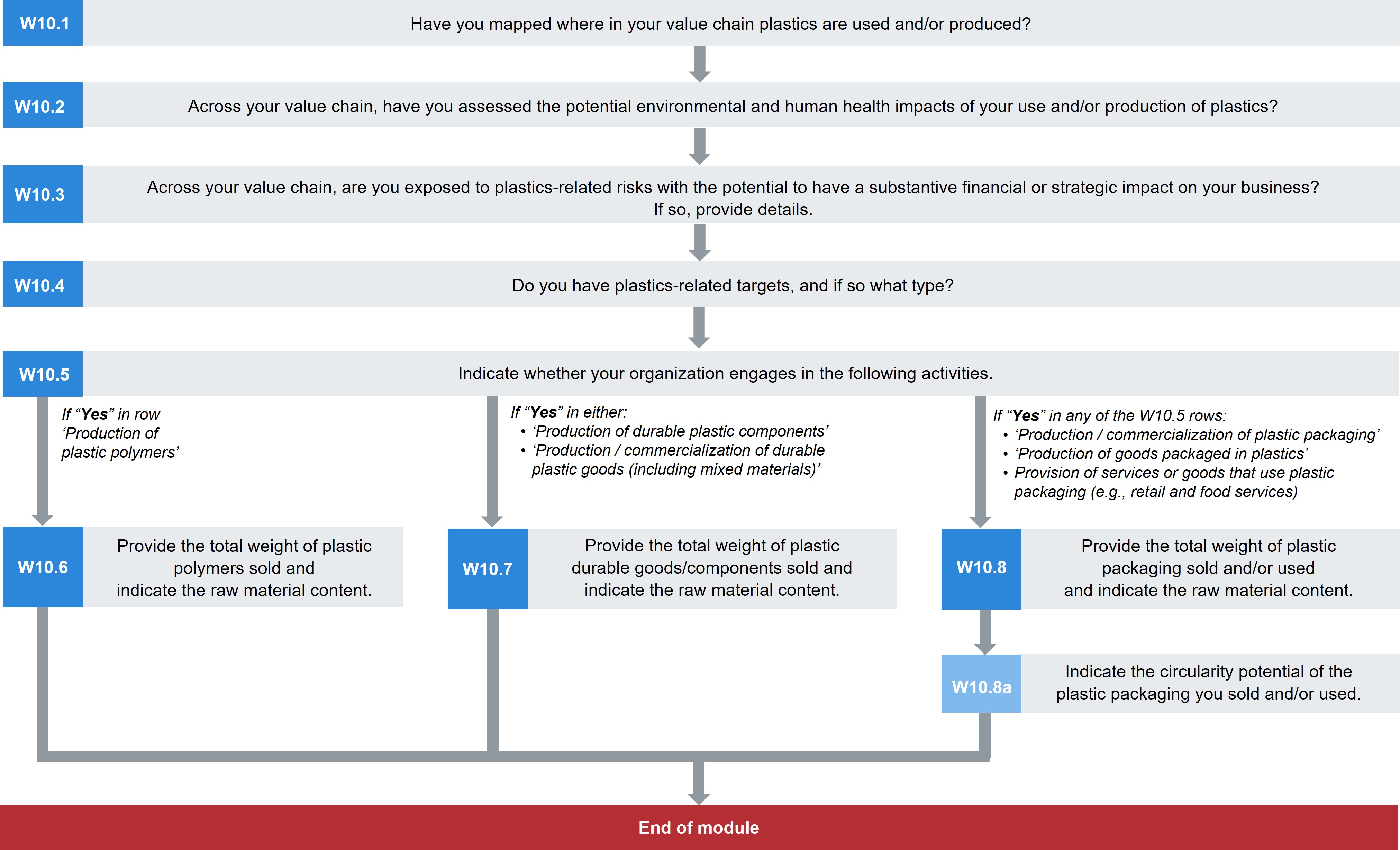

- 塑料

行业方法

- 对水资源有高影响的行业内的公司会收到行业特定的信息采集要求,新增或替代一般水资源数据点。

- 在每个章节的简介部分罗列了为各个行业制定更详尽问卷的原因。

- 只针对特定行业公司的问题,问题编号处会标注两个字母的行业名缩写(如下)。一些以W开头的一般水资源问题可能会包含针对行业的数据要求。在披露平台上,这些问题只会向相关行业内的公司展示。

2023年水资源相关行业:

- 农业:农业商品(AC);食品、饮料和烟草(FB)

- 能源:公共电力 (EU);石油和天然气(OG)

- 材料:化学品(CH);煤炭(CO);金属和采矿(MM)

关于2023年度水安全问卷的变更

对于2023年,2022年版本问题中的73%以上没有改变,或者只是稍加修改。一些问题已被修改,一些已被删除,一些新问题已被添加。

增加了14个问题,当前问题总数为85个(不包括行业特定问题或供应链模块)。请注意,每个公司都有一个独特的途径来完成问卷调查,例如,在每个模块中,这是由该公司部门及其回复决定的。没有一家公司会涵盖所有问题。

关键变更包括:

所有公司

- 塑料新模块

- 9个新问题,包括塑料在价值链的分布、影响评估、业务风险以及目标。对于有具体塑料生产和/或使用活动的公司,有关于总重量、原材料来源和循环潜力的问题。

- 4个被删除的问题:

- W1.4a (2022)、W1.4d (2022)、W8.1b (2022)、W10.2 (2022).

- 9个新问题

- 在W1的“当前状态”中:6个新问题 - 1个关于向水体的排放,2个关于有害物质,3个关于价值链参与。

- 在W3的“过程”中:2个关于水污染物管理的新问题

- 在W8的“目标”中:1个关于水相关目标类别的新问题。

- 修订了5个问题的问题相关性:

- 问题不再取决于对W1.1的回答:W1.2、W1.2b、W1.2d、W1.5 (2022 W1.4).

- 修订了19个问题:

- 9个问题在W1“当前状态”中:W1.2、W1.2b、W1.2d、W1.2h、W1.2i、W1.2j关于水核算量;和W1.5 (2022 W1.4)、W1.5d (2022 W1.4b)、W1.5e (2022 W1.4c)关于价值链参与。

- 1个问题在W2“业务影响”:W2.2关于罚款和强制执行令

- W3“过程”里有1个问题:W3.3b关于风险评估过程。

- W6 治理W6.1a, W6.2a, W6.3, W6.4a关于水政策、董事会监督、管理职责和员工激励措施。

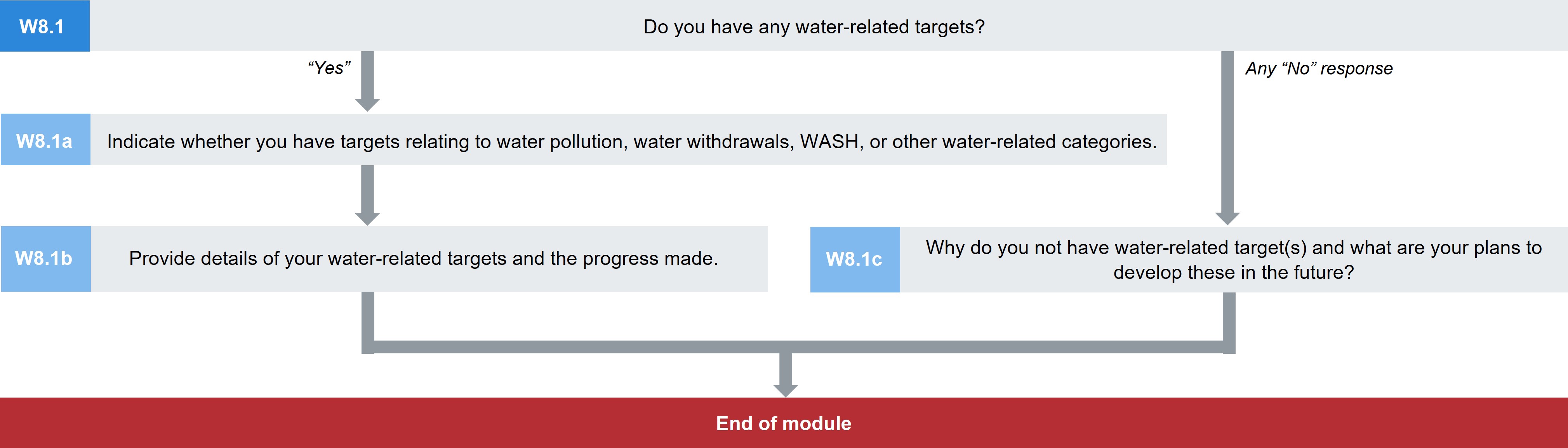

- 3个问题在W8“目标”中:W8.1、W8.1b、(2022 W8.1a)、W8.1c关于目标类别和详情。

- 8个问题有已修改指南: W2.1a, W4.1b, W4.1c, W4.2b, W4.2c, W4.3a, W4.3b, W7.4.

- 3个问题有新增指南(回答示例、术语解释、附加信息):W3.3a, W6.6, W7.4.

- 细微修改了5个问题:W2.1a, W3.3a W4.2, W4.2a, W6.2b.

特定行业

- 被删除的问题:

- 2个普适问题(2023 W3.1 and W3.1a)替代了8个特定行业污染物管理问题:

- 化学品行业:W-CH3.1 (2022)和W-CH3.1a (2022)

- 公共电力行业:W-EU3.1 (2022)和W-EU3.1a (2022)

- 食物、饮料和烟草行业:W-FB3.1 (2022)和W-FB3.1a (2022)

- 石油和天然气行业W-OG3.1 (2022)和W-OG3.1a (2022)

- 新问题:

- 8个关于农产品行业的问题:

- W-FB0.1a/W-AC0.1a, W-FB1.1a/W-AC1.1a, W-FB1.2e/W-AC1.2e, W-FB1.2f/W-AC1.2f, W-FB1.2g/W-AC1.2g, W-FB1.3/W-AC1.3, W-FB1.3a/W-AC1.3a, W-FB1.3b/W-AC1.3b

- 针对煤炭行业的7个问题:

- W-MM0.1a/W-CO0.1a, W-MM1.3/W-CO1.3, W-MM1.3a/W-CO1.3a, W-MM3.2/W-CO3.2, W-MM3.2a/W-CO3.2a, W-MM3.2b/W-CO3.2b, W-MM3.2c/W-CO3.2c

- 修订了8个问题的问题相关性:

- 特定行业的问题不再取决于对W1.1的回答:

- 化学品行业:W-CH1.3

- 公共电力行业:W-EU1.2a, W-EU1.3

- 食物、饮料和烟草行业:W-FB1.2e/W-AC1.2e, W-FB1.3/W-AC1.3

- 金属和采矿行业:W-MM1.3/W-CO1.3

- 石油和天然气行业W-OG1.2c, W-OG1.3

- 修改了2个问题:

- W-FB1.1a/W-AC1.1a, W-OG1.2c

- 细微修改了4个问题:

- 关于煤炭的W-MM0.1a/W-CO0.1a, W-MM3.2a/W-CO3.2a, W-MM3.2b/W-CO3.2b, W4.1c

问卷里的修订和变更以下列短语表示:无修改、细微修改、已修改问题、新问题、已修改指南、新增指南或修订问题相关性。“细微修改”表示对下拉选项的措辞编辑和修改或简单说明,而修改表示请求的数据有所修改。

1份详细文档,关于 可在网站上的指南页面查看有关2022至2023年水安全问题变更的详细文件。

准备您的CDP回复

请在下方查看关于公司可用支持材料和选项的信息,以及完成披露所需的重要说明。即使您在之前的年度已经参与过问卷回复,请在准备回复该问卷时,仔细阅读这些说明。

CDP披露支持材料

CDP为帮助组织通过调查问卷进行披露提供了各种支持材料。在公司填写调查问卷前,我们强烈建议您首先阅读填报指南、评分说明以及相关的评分方法。登录网站后,请参考CDP技术说明和指南工具提供的其他指导材料,并查看网站上的常见问题。

填报指南

本文件中的填报指南包括以下几部分:

- 模块级别指南:对于部分模块,本指南提供主要更改的概述、特定行业内容以及重要的披露说明。本节还介绍了问题路径图,显示了每个模块的问题流程。

- 问题级别指南:在问题级别,指南分为以下几个部分以明确问题、术语和要求:

-理论依据:说明纳入该问题的理由。

- 与其他框架的联系:说明水安全调查问卷中每个相关问题与可持续发展目标(SDG)、全球报告倡议标准303-3、CEO水资源管理倡议、标普全球企业可持续发展评估以及艾伦·麦克阿瑟基金会全球承诺的联系;

- 要求内容:根据每个问题和要求标准提供上下文;

- 术语解释:提供特定术语的详细定义;

- 回复示例:对于选定的问题,提供了一个包含所有请求需求信息的回复示例;以及

- 附加信息:对于选定的问题,提供了与要求披露主题相关的可选上下文信息和来源。

- 术语表:可在报告指南末尾查看,术语表包含“术语解释”的一个子文件

- 附录:流域列表和南非水资源管理区域,按国家/地区

如果您在填写问卷时,报告指南、下述附加指南或常见问题都无法解决您的疑问,请联系您当地的CDP联系人,或访问CDP帮助中心。

线上线下研讨会

CDP将主办各种线上线下研讨会,以助您进行环境信息报告。

如需了解详细信息,请访问CDP网站的研讨会和网络研讨会及水安全网页。

CDP报告者服务

CDP报告者服务为贵司管理和报告环境风险提供定制化的支持、更丰富的数据资源以及思想领导力的培育。利用您所需要的工具实现从披露气候、森林管理和水安全信息,转向领导其融入更广泛商业战略的角色转换。如需要获得CDP客户经理为您提供全年的、个性化信息披露支持,对您之前的回复进行差异分析,进行提交前的最终检查,并提供分析工具,以便您与同行进行对标和了解最佳措施,请联系[email protected]。如需获取更多信息,请访问CDP网站的报告员服务页面

CDP水资源咨询方案提供方

CDP认可的水资源咨询方案提供方将为希望改善水资源管理的公司提供支持。合作伙伴必须经过筛选,经过审批后可与公司密切合作,就重要主题提供专业意见,包括但不限于:水核算,水风险评估,制定水资源策略以及管理计划的制定和实施。访问CDP网站的合格的方案提供方页,或者联系[email protected]获取更多信息。

问卷填写重要说明

首字母缩略词

避免使用特别编写的内部缩写词,除非贵组织在回复中必须用到,在这种情况下,请提供它们的含义解释,以便能够进行正确的分析和评分。

空白回复

将回复留空则被解释为不披露。对于数字字段,零(0)值表示已经进行相关测量,且其值为零(0)。对于未进行测量的数字字段,请将字段留空,并在该问题的开放文本字段中提供解释(例如“备注”(可选)或“请解释说明”(已评分))。如果问题没有开放文本域,您可以于披露结束时在在线回复系统(ORS)的“更多信息”一栏中提供说明。回复留空并输入零(0)值会产生不同的评分含义。有关更多详细信息,请参阅评分方法。

字符限制

报告指南和在线回复系统中注明的字符限制包括了空格。

“备注”栏

有些问题包括“备注”栏。请注意,这些分栏的填写为可选项。

公司特定信息

有些问题需要提供公司特定的信息、理由、案例研究和/或例子。这些详细信息能让数据用户相信回复机构已将自有业务与当前问题相结合并进行了周密考虑,而不只是按照一般惯例进行简单评估。

- 请确保在内容中包含公司特定的详情,例如贵公司特有的业务或运行相关的活动、项目、产品、服务、方法论或经营位置等的参考信息。公司特定信息应包括能证明填报公司的答案真实可信,且有别于同行业和/或同地区其他公司的详细信息。

- 清晰明确的理由指的是针对方法、描述、决策和行动提供具有逻辑的说明。

- 案例研究应针对公司具体情况展开,并应遵循“情境-任务-行动-结果”(STAR)的方法:1) 情境:什么样的背景环境?2) 任务:需要完成什么/需要解决什么问题?3) 行动:已采取什么行动?4) 结果:最终结果是什么?

- 例子不需要遵循STAR方法,可以比案例研究短,但应该包括一些公司特定详细信息。

如需了解更多详细信息,请参考CDP网站上的评分说明。

一致性

CDP鼓励全面且一致的回复。请确保您在单个问题以及整个问卷中的回复中没有相互矛盾的信息。

复制回复

只有在之前的报告年使用ORS向CDP披露过的公司才能选用“复制回复”功能。此功能会自动将您上一次回复的答案填入本次的调查问卷中(如果适用)。

请注意,修订后的数据点可能无法使用该功能。填报指南将对进行了修订的问题进行说明。CDP网站指南版块的问卷变更文件列出了较前一年的所有修改之处。

请仔细检查自动填入的答案。您有责任对答案进行更新,从而确保答案的准确性和完整性。

数据准确性

CDP承认数据可能会带来不确定性。这种不确定性可能来自数据缺口、假设、计量/测量限制,包括设备精度等。CDP允许提交预估数据。但是,需要特别强调的是报告的透明性。这意味着公司在报告预估值时一定要对其进行说明,并详细描述其不确定性(使用问题中的“请详述”或“备注”栏)。

下拉选项(“其他,请说明”)

请尽可能从提供的选项中进行选择,只有当所列选项都不合适时,才选择“其他,请说明”。这对数据分析很有帮助。如果选择“其他,请说明”,您必须增加一段说明,以描述您将提供数据的选项。

“更多信息”区域

在调查问卷的最后,您有机会提供您认为与贵组织的回复相关的其他信息或背景。此区域属于选填,不会进行评分。

兼并与收购(并购)

所有披露应由所述报告期内适用的组织边界确定。(请注意,CDP在披露工作中鼓励组织使其报告周期和组织边界与其财务报告保持一致)。

关于前瞻性披露,组织应包括在所述报告周期内正确的信息(例如,涉及未来或“未来两年”的数据点)。正在进行(或已进行)并购的组织需要考虑并购和报告周期的时间安排,如下:

- 在本报告周期结束后被收购的组织:这些组织应回复收购之前(即在报告周期期间)的计划内容(战略、目标等)。为保持透明性,在可能的情况下,他们会说明他们认为前瞻性信息可能会因最近的收购而发生变化的地方。

- 在报告周期内收购的组织:在报告周期结束时,这些组织应提供其所知适用的正确信息。提交CDP回复时,由于企业收购后仍在进行的变化,提交信息可能无法反映最新的情况。为确保透明,在可能的情况下,公司可以在披露中说明这一点。

个人数据

请您务必在作答时不要包含个人名称或其他个人数据。对于要求提供员工职位的问题,出于对个人数据隐私的尊重,我们只询问职位而不涉及个人姓名或任何与个人有关的其他信息。

向CDP提供反馈

您可以通过我们的在线一般反馈表,向CDP提供关于调查问卷和支持文件的反馈。

我们无法对所有反馈进行单独回复,但是请放心,所有提交的表格都将经过审核,以帮助我们不断改进。

但是,如果您代表某家填报组织,并希望获得回复,请联系您当地的CDP联系人。

An introduction to the CDP Water Safety Reporting Guide

Water information filling

Water resources face a unique set of measurement and reporting challenges, both locally and globally.

- First, water management is a local or regional issue. Therefore, local environmental factors are extremely important. Challenges and opportunities depend on local rainfall, watersheds, aquifers and the nature and extent of local water use, as well as the scope and effectiveness of water governance and laws and regulations. Unlike a tonne of CO2, which affects Stockholm and Sydney in the same way, the geographical scale, location and timing of water use have an important impact. The impact of using one cubic metre of water in Sydney is very different from that in Stockholm. This makes it difficult to develop a common approach to water management and meaningful corporate water indicators for progress towards water security.

- Water reporting standards have not yet been established as consistently or widely as greenhouse gas emissions.

- Although greenhouse gas emissions are uniformly used metric tons of CO2e, but there is no single or interchangeable unit of measurement that can track all water-related risks and impacts. A variety of factors must be considered, including availability, water quality, degree of competition in the region concerned, future realities, regulatory, market and technological changes.

- The global nature of commerce and industrial chains means that water use will involve multiple terrains, which exacerbates this complexity. Even when their actions or assessments are not affected, many businesses may be affected by changing patterns in water availability. For large companies with complex supply chains (thousands of potential suppliers), assessing water use and related products or supply chain issues can be complex.

CDP's approach to water reporting

consistency

To develop standards that are important to both parties and provide useful information to investors, policymakers, and other data users, CDP works with organizations such as CEO Water Mandate, World Resources Institute, WWF, World Business Council for Sustainable Development, and Global Reporting Initiative (GRI), Alliance for Water Stewardship (AWS), Ceres, Sustainability Accounting Standards Board (SASB), etc. Standardization is to promote transparency, facilitate reporting, and maintain consistency and comparability for data users.

CDP's water security requirements and our reporting guidelines utilize reporting principles, framework definitions, and standards to align as much as possible. If there are still inconsistencies, it needs to reflect the company's unique approach and goals.

Note on consistency with GRI 303: Water and Wastewater 2018: Organizations using GRI Standards for disclosure will find it helpful to refer to the link between GRI and CDP. It establishes a link between the information required for the GRI 303 standard and the information required for the CDP's 2018 Water Security Questionnaire. Since there are few sections of the revised questionnaire, it will still be helpful for your organization's 2023 CDP disclosure.

W10 Plastics Module Description: These questions reference some existing frameworks, including the Alan MacArthur Foundation and UNEP's Global Commitment Framework. Please refer to the CDP Plastics Technical Disclosure NoteCDP Plastics Technical Disclosure Note section, which lists the links between the W10 plastic module and the Global Commitment.

Overview of the Water Safety Questionnaire

The entire structure of the Water Security Questionnaire is designed as a framework to help companies advance water management and improve the maturity of corporate reporting. The questionnaire concerned water management and water security.

Collect and disclose information on risk and opportunity management, governance responses, and integrating water into long-term strategic goals, and provide decision-making data to facilitate corporate action. That's what disclosure is all about.

Water accounting

To advance water security for all companies and reduce water-related risks in the future, companies must remove all negative impacts on water ecosystems and resources. There are impacts and risks when water flows in and out of company boundaries, so CDP collects information to determine how aware companies are of these flows. Companies are encouraged to consider all water interactions and to minimize such interactions (e.g., by reducing water withdrawals, improving efficiency, or changing business activities). This means that CDP wants to get more specific information than the reduction in freshwater withdrawals. The most important thing is that the company implements strong monitoring and accounting for all aspects of the company's hydrology to demonstrate its understanding of water dependence.

When water resources involve company boundaries, companies need to count water withdrawals, discharges, and water consumption at the company or facility level. Provide a concept of corporate boundaries at the company and facility level in accordance with our disclosure requirements.

Background and geographic scope

Water issues here represent issues that need to be understood and managed locally; It's usually basin size, or at least country, rather than just company size. Today, investors are increasingly paying attention to this level of information when assessing the water risks in their investments.

Some CDP data users want to assess an organization's ability to obtain granular data needed to understand mature water management and sound risk management across all its operations and locations. This practice is considered a best practice. A separate module (W5) to fill in any facility water accounting data that may pose a substantial water-related risk to the company (please note that we are not asking for data for all facilities).

In addition, CDP invites companies to report risks at the basin level and answer questions so they can indicate where the data is relevant. Without taking into account the local watershed environment and conditions, an organization cannot have a comprehensive assessment of risk exposure and the most appropriate response approach. Basin-level risk assessment is closer to a water management approach to ensuring water security, as collaboration with other basin users and external stakeholders is central to understanding and managing water risks.

Report risks

CDP provides data users with information about the inherent risks faced by the organization. This allows users to independently assess the correctness and adequacy of the organization's response to understand the residual risks and resilience of the business.

In order for data users to confirm the company's disclosures, responding organizations are encouraged to fully explain their risk assessment approach and how to successfully integrate water-related issues into the company's strategy.

Report the impact

When it comes to "impact," there are frameworks and structures that use the term to denote the impact of the business on communities and ecosystems, such as the CEO Water Mandate Guidelines and the GRI Standards. CDP uses the term "impact" to refer to impacts on communities and ecosystems, or the impact of water-related challenges on operations, i.e. "business impacts," whether they are caused by physical, regulatory, or market drivers.

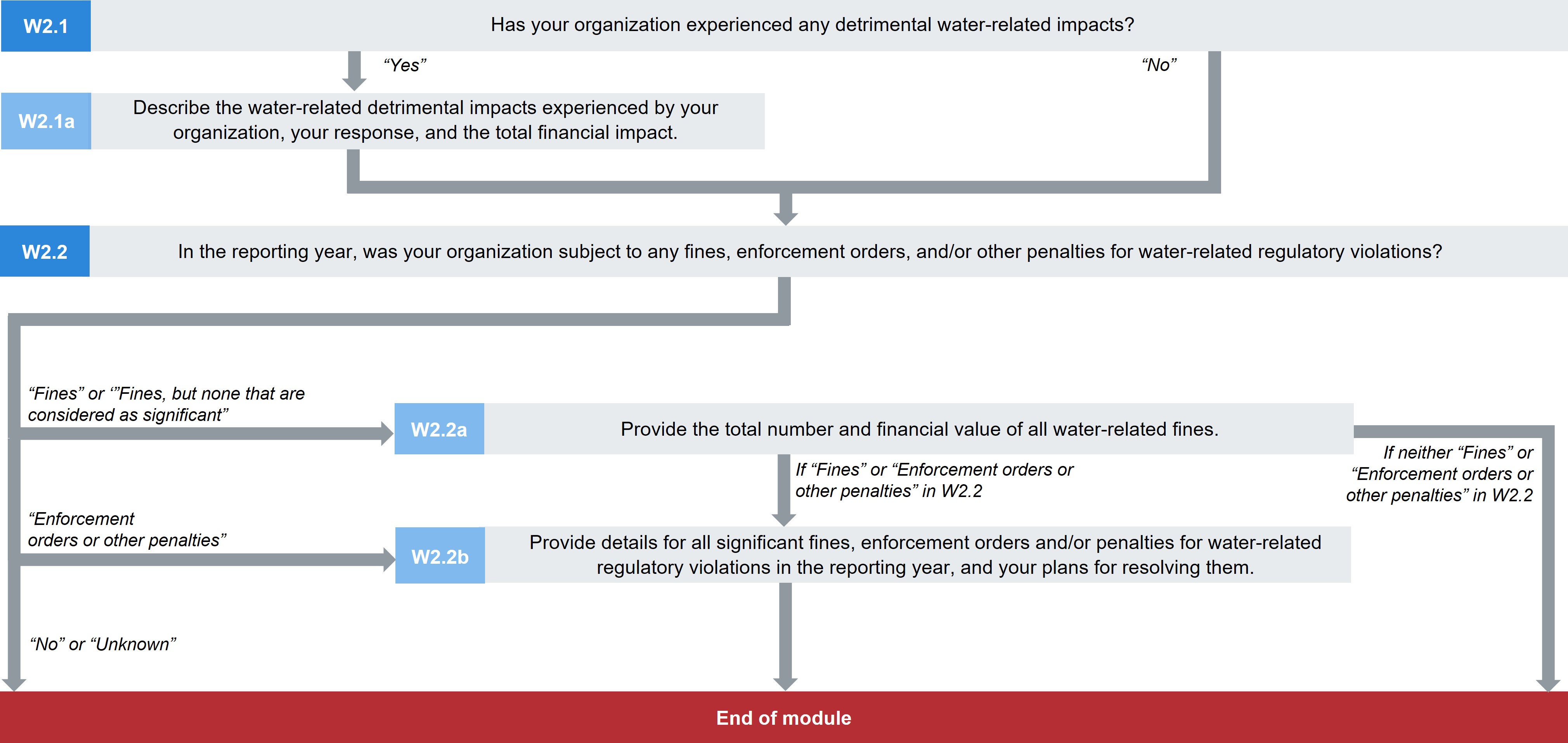

The questionnaire details the impact on business or water security in different situations. For example, in W2 "Business Impact," CDP asks for details of the water-related impacts a company has experienced in the past and how it has responded. Data users may use this data to judge the company's future performance.

Reporting principles – truthfulness and impartiality

The GHG Protocol lists 5 principles to ensure the authenticity and fairness of a company's greenhouse gas emissions (see The Greenhouse Gas Protocol: A Corporate Accounting and Reporting Standard.) , developed by the World Resources Institute and the World Business Council for Sustainable Development). CDP recommends applying all of these principles to water reporting. These principles include the following:

-

Relevance: Ensure that water use inventories appropriately reflect actual utilization and meet the needs of users for internal and external decision-making.

-

Completeness: Accounting for and reporting of all water activities within the boundaries of the selected list. Disclose specific information about any exceptions and explain them.

-

Consistency: Use a uniform methodology to make meaningful chronological comparisons of a company's water use.

-

Transparency: Handle all relevant issues in a true and consistent manner based on clear audit records. Disclose any relevant assumptions and cite appropriately the accounting and calculation methods used and data sources, etc. Transparently and chronologically record any changes to data, inventory ranges, methods, or other relevant factors.

-

Accuracy: Ensure that water use is quantified accurately enough to enable users to make decisions with reasonable assurance of the integrity of the reported information.

如果信息包含了公司内部用户及外部用户做决策所需的详情,则此类信息就可视为相关信息。当考虑披露内容时,请区分并报告那些对要求获得信息的读者(例如投资者和客户)有用以及有益的信息。

回复水安全问卷的说明

1.单位:所有问题中的体积必须使用兆升/年为单位(1兆升=1百万升或1,000 m3),除非另有说明。

2.数值为0:输入数字0(零)意味着进行了该项计量,需要披露的数字为0(零)。如果您没有数据可披露,请不要输入零。

3.流域:从具体问题的下拉列表中选择披露的流域,或者选择“其他,请说明”,并提供流域名称。(请参见CDP的附录:流域列表和南非水资源管理区域,按国家/地区)。

CDP的流域下拉列表与CEO Water Mandate的Interactive Database of the World’s River Basins一致。对于在南非运营的公司,该列表也包括9个南非水资源管理区域。您可能希望输入所列流域的子流域。这时,按下列格式使用“其他,请说明”选项:“亚马逊,普图马约”。

对于从不流入当地流域的大型封闭蓄水层(例如美国的奥加拉拉蓄水层)取水的公司, 请选择“其他,请说明”并输入当地蓄水层的名称。

如果您不知道披露数据与哪个流域相关,下列工具能够识别设施所在的流域,您只需输入地理位置坐标,例如:

- The CEO Water Mandate Interactive Database of the World’s River Basins

- The Water Footprint Assessment Tool - Water Footprint Network

- The Water Risk Filter - WWF

- The WRI Aqueduct Water Risk Atlas Tool - the World Resources Institute

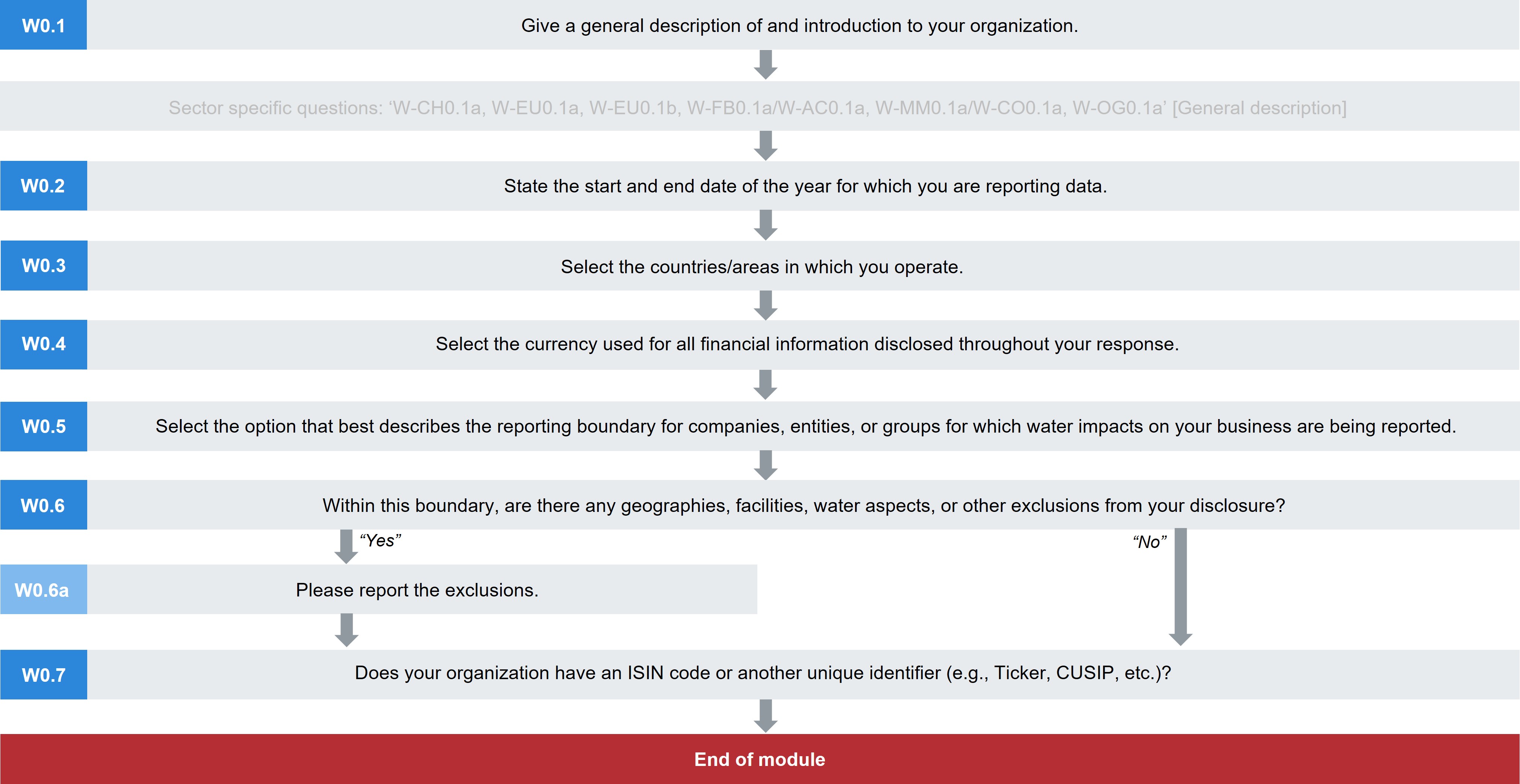

W0 简介

Module Overview

This module requests information about your organization’s disclosure to CDP and will help data users to interpret your responses in the context of your business operations, timeframe and reporting boundary.

The information provided here should apply consistently to your responses throughout the questionnaire and be complete and accurate as it may determine response options presented in subsequent modules.

For this reason, you should respond to every question in this module and save your response before accessing the rest of the questionnaire.

Key changes

Sector specific changes only

- New questions:

- One for the Agricultural Commodities sector: W-FB0.1a/W-AC0.1a

- One for the Coal sector: W-MM0.1a/W-CO0.1a

- Click here for a list of all changes made this year.

Sector-specific content

- Additional questions for: Chemicals, Electric Utilities, Food, Beverage & Tobacco, Agricultural Commodities, Metals & Mining, Coal, and Oil & Gas.

Pathway diagram - questions

This diagram shows the questions contained in module W0. To access question-level guidance, use the menu on the left to navigate to the question.

简介

(W0.1)请提供贵组织的大致说明及介绍。

对比上一年的变化

没有变化

理由

这将有助于数据用户结合您的业务活动和行业背景理解您的回复。

回复意见

这是一个开放文本问题,字符限制为5,000字符。

要求内容

通则

- 提供有关运营和商业活动的信息,来帮助数据用户理解公司业务以及业务与水风险和公司战略的联系。该信息为整体披露提供了背景。

Explanation of terms

- Organization: Throughout this information request, “your organization” refers collectively to all the companies, businesses, other entities or groups that fall within the definition of your reporting boundary (provided in W0.5). This term is used interchangeably with “your company”, but CDP recognizes that some disclosing organizations may not consider themselves to be, or be formally classified, as “companies”.

(W0.2)请对贵组织填报数据所涉及的起止年度进行说明。

对比上一年的变化

没有变化

理由

这将帮助数据用户理解与报告的时间段相关的回复内容。

回复意见

请完成下方表格:

| 起始日期

|

结束日期

|

|

自:[月/日/年]

|

至:[月/日/年]

|

要求内容

通则

- 该报告年份将应用于您对整个问卷的回答。

- 当前报告年度指的是报告数据的最近12个月。

- 投资群体通常希望公司的披露时间能够与其财政年或其财政辖区相匹配。这有助于哟用户根据公司的财务绩效数据评估其环境绩效数据。

- 如可能,CDP建议公司提供自己有完整数据支撑回复内容的年份。如果您没有报告年的完整数据,可以选择推测或预估整个报告年的数据。

(W0.3)选择您开展业务的国家/地区。

问题依赖关系

- 您在W0.3的回答将决定在该部分后面出现哪些国家和流域选项。若修改W0.3的回答,可能会删除相关问题已输入的数据。在这种情况下,请务必重新输入所有相关问题的数据。

对比上一年的变化

没有变化

理由

这可以帮助数据使用者理解您的回复。

回复意见

请完成下方表格:

要求内容

通则

- 请从所提供的下拉列表中选择运营所处的所有国家/地区。

(W0.4)请选择在整个回复中用于金融信息披露的货币种类。

问题依赖关系

- 文件中披露的所有经济数据均要使用同样的货币。该问题所选的货币将应用于所有上报数据。

对比上一年的变化

没有变化

理由

CDP鼓励公司报告与影响、风险和机遇相关的财务数据。实行单一货币将有助于收集可对比财务信息。评估贵组织报告的成本和利益,将令投资者和其它数据使用者受益。

回复意见

请完成下方表格:

要求内容

通则

- 所选货币适用于披露报告中的所有财务信息和财务指标。

- 例如,如果您选择美元($),那么W2.1a“财务影响”中的数据应使用该货币单位。

(W0.5) 请选择最能描述您正在填报的、对您的业务造成水相关影响的公司、实体或集团的填报范围的选项。

对比上一年的变化

没有变化

理由

这能帮助数据用户理解贵组织的回复如何与商业运营联系起来。

回复意见

从下列选项中选择一个:

- 整体进行财务控制的公司、实体或集团

- 整体进行经营控制的公司、实体或集团

- 内部持有股票的公司、实体或集团

- 其它,请说明

要求内容

通则

- 财务控制权:如果一个组织有能力管理一项业务范围内的财务和运营政策,并且希望从中获取经济利益,那么该组织对该业务项目拥有财务控制权。 一般来说,如果一个组织以财务整合为目的将负责GHG核算的业务视为集团公司或子公司,则该组织对该业务拥有财务控制权。

- 运营控制权:如果一个组织或者其附属子公司在一项业务中能全权引入和实施其运营政策,那么该组织对该业务拥有运营控制权。

- 股权份额:从股权份额方面看,一个企业根据其在运营业务中的股份占比对运营的GHG排放数据负责。股权份额反映经济利益,即企业对于业务运营的风险与回报所持的权利范围。通常情况下,公司在一项运营业务中所占的经济风险与回报的份额与其在该项业务中的所有权比例是一致的,而股权份额通常与所有权比例是相同的。如果不是这种情况,企业与运营关系的经济实质总是超越法定所有权形式,以确保股权份额反映经济利益的百分比。经济实质优先于法律形式的原则符合International Financial Reporting Standard(国际财务报告标准)。

-其他,请说明:只有在其他选项都不适用的情况下才能选择该选项。如果您选择该选项,请在文本域中进行说明。

- 请注意:在整个问卷中,除非另有说明,公司层面报告的数据计算方法均采用“整合法”。贵组织报告的信息应该是用“整合法”整合后的结果,并应该涵盖报告界限内所有的公司、实体或业务且集合更多设施/业务层面的粒状数据。除非有特别要求提供另一类别活动的数据,否则在回复问题时请使用一致的公司界限。

- 请注意:在W0.6a中,您可以说明任何没有包含在所选报告界限中的数据。

Explanation of terms

- Company: throughout this information request, “your company” refers collectively to all the companies, businesses, organizations, other entities or groups that fall within the definition of your reporting boundary. It is used interchangeably with "your organization".

- Organization: this term is used interchangeably with “your company”. CDP recognizes that some disclosing organizations may not consider themselves to be, or be formally classified, as “companies”.

- Reporting boundary: this determines which organizational entities, such as groups, businesses and companies, are included in or excluded from your disclosure. These may be included according to your financial control, operational control, equity share, or another measure.

Additional information

- Determining the organizational boundary: When determining the organizational boundary for reporting purposes, CDP recommends that companies consult their legal or accounting advisors. For more guidance on determining reporting boundaries, particularly where joint ventures or complex operational structures are concerned, refer to the GHG Protocol. Although the protocol refers to GHG emissions reporting, the general definitions may be applied to water reporting.

- The GHG Protocol defines two approaches: the control approach and the equity share approach, which will lead not only to different organizational boundaries, but distinct ways of consolidating the figures at the corporate level.

- Control approach: An organization measures the volume of its water withdrawals/discharges from operations over which it has financial or operational control. The following text is adapted from the GHG Protocol to refer to water:

- An organization has financial control over an operation if it has the ability to direct the financial and operating policies of the operation with a view to gaining economic benefits from its activities. Generally, an organization has financial control over an operation for water accounting purposes if the operation is treated as a group company or subsidiary for the purposes of financial consolidation. An organization has operational control over an operation if the organization or one of its subsidiaries has the full authority to introduce and implement its operating policies at the operation.

- Equity share approach: Organizations can also report their water data based on their economic share. The following text is adapted from the GHG Protocol to refer to water:

- Under the equity share approach, a company accounts for its water data from operations according to its share of equity in the operation. The equity share reflects the economic interest, which is the extent of rights a company has to the risks and rewards flowing from an operation. Typically, the share of economic risks and rewards in an operation is aligned with the company’s percentage ownership of that operation, and equity share will normally be the same as the ownership percentage. Where this is not the case, the economic substance of the relationship the company has with the operation always overrides the legal ownership form to ensure the equity share reflects the percentage of economic interest. The principle of economic substance taking precedence over legal form is consistent with international financial reporting standards.

- The table below clarifies how water accounting data should be consolidated and reported in certain situations. The table below is based on page 19, Chapter 3 of the GHG Protocol (Revised Edition). It has been adapted to refer to water accounting instead of GHG accounting.

|

Accounting category

|

Financial accounting definition

|

Accounting for GHG emissions according to the GHG Protocol Standard:

Based on equity share

|

Accounting for GHG emissions according to the GHG Protocol Standard:

Based on financial control

|

Group companies/subsidiaries

|

The parent company has the ability to direct the financial and operating policies of the company with a view to gaining economic benefits from its activities. Normally, this category also includes incorporated and non-incorporated joint ventures and partnerships over which the parents company has financial control.

|

Equity share of volumes of water withdrawn/ discharged/etc.

|

100% of volumes of water withdrawn/ discharged/etc.

|

Associated/affiliated companies

|

The parent company has significant influence over the operating and financial policies of the company, but does not have financial control. Normally, this category also includes incorporated and non-incorporated joint ventures and partnerships over which the parent company has significant influence, but not financial control. Financial accounting applies the equity share method to associate/affiliated companies, which recognizes the parent company’s share of the associate’s profits and net assets.

|

Equity share of volumes of water withdrawn/ discharged/etc.

|

0% of volumes of water withdrawn/ discharged/etc.

|

Non-incorporated joint ventures/ partnerships/ operations where partners have joint financial control

|

Joint ventures/ partnerships/ operations are proportionally consolidated, i.e., each partner accounts for their proportionate interest of the joint venture’s income, expenses, assets and liabilities.

|

Equity share of volumes of water withdrawn/ discharged/etc.

|

Equity share of volumes of water withdrawn/ discharged/etc.

|

Fixed asset investments

|

The parent company has neither significant influence nor financial control. This category also includes incorporated and non-incorporated joint ventures and partnerships over which the parent company has neither significant influence nor financial control. Financial accounting applies the cost/ dividend method to fixed asset investments. This implies that only dividends received are recognized as income and the investment is carried at cost.

|

0%

|

0%

|

Franchises

|

Franchises are separate legal entities. In most cases, the franchiser will not have equity rights or control over the franchise. Therefore, franchises should not be included in consolidation of GHG emissions data. However, if the franchiser does have equity right or operational/ financial control, then the same rules for consolidation under the equity or control approaches apply.

|

Equity share of volumes of water withdrawn/ discharged/etc.

|

100% of volumes of water withdrawn/ discharged/etc.

|

(W0.6)在填报范围内,贵公司的披露中是否有地理、设施、水指标或其他排除项?

对比上一年的变化

没有变化

理由

CDP希望获得全面和富有代表性的水资源数据。如果公司披露报告中确实需要排除某些业务,必须告知数据用户各排除项,否则会影响到用户分析。

回复意见

从下列选项中选择一个:

要求内容

通则

- 问卷中对“贵组织”的引用是指您要为其提供信息的组织范围内的实体。请在回答问题时遵循这一逻辑。但是,在水资源影响非常小的情况下,您可以排除某些很难收集数据的特别地理位置、商业活动、和/或小型设施。这也适用于进水量/出水量。

- 在任何情况下,所有披露信息都必须符合以下相关性和透明性原则(改编自温室气体协定):

-相关性:确保披露信息正确反映公司的水资源利用情况,满足用户进行公司内外部决策的需求。

-透明性:根据清晰的审计记录,以真实连贯的方式处理所有相关问题。披露任何相关假设,并适当引用所使用的核算和计算方法以及数据来源等。

- 任何属于组织范围内,但不包含在您的披露范围内的集团、公司、企业或组织应在W0.6a列出。

- 请注意,在有些问题中(例如设施层面的水核算章节),我们只要求提供具有重大水资源风险的设施数据,而不是报告范围内的所有设施。

Explanation of terms

- Facilities: “Facilities” may be used throughout this questionnaire as a broad term and not restricted to a particular site or grouping of fixed buildings and factories. For example, if your organization is in the extractive industries you might normally collate business information for assets or business units, and so you may wish to define ‘facility’ information in this way.

Additional information

The GHG Protocol states that an acknowledgement of all exclusions should be made each year to enhance transparency despite disclosure of the same exclusion in previous years. This ensures all data users are always aware of what data has been included in your response.

For further information on allowable exclusions, please refer to the GHG Protocol and the CDP Water Security Scoring Methodology.

(W0.6a)请填报排除项。

问题依赖关系

对比上一年的变化

没有变化

理由

CDP希望获得全面和富有代表性的水资源数据。需要告知排除项以避免影响数据用户的分析结果。

回复意见

请完成下方表格。您可以使用表格下方的“添加行”按钮来添加新的行。

| 排除项

|

请详述

|

|

文本字段[最多2,500个字符]

|

文本字段[最多2,500个字符]

|

[添加行]

要求内容

通则

- 若不披露以下内容,请进行说明

- 地理位置,例如低耗水量或者数据限制可能无法填报某一国家/地区/区域的运营情况。

- 活动,例如某项产品线、业务流程类型或者供应商类型可能因为有限的数据或报告可行性被排除。

- 设施可能因为近期发生的合并、收购(报告年度内发生的事件)和剥离、外包和内包而被排除(目前无法跟踪用水情况的较小型设施也可以考虑排除);和

- 水输入和输出,例如,某家公司可以在一些设施上利用雨水,但无法追踪水量或水质,在这种情况下可以考虑排除。

- 集团、公司、企业或组织若属于组织范围但不包含在披露报告中可排除。

- 详细解释所有排除项未被披露的原因。并对如何确定排除项给出合理解释,例如通过高层面风险排查决定。

Example response

| Exclusion

|

Please explain

|

| Distribution Centers

|

Our company has not yet implemented a system to track the water impact in its distribution centers. We expect this to be a small fraction of our total water consumption and provide little exposure to water risk. This will be incorporated from 2019.

|

| Offices

|

Small leased office spaces (fewer than 50 employees) where water use is minimal. It is provided through the lease and managed by our landlord.

|

(W0.7)您的组织是否有ISIN代码或其他唯一标识符(例如,Ticker、CUSIP等?)

对比上一年的变化

没有变化

理由

ISIN编码和其他市场识别码可用于识别全球范围内的债券、期货和股票等证券。提供贵组织的独特的识别码将提高您的回复的透明度。

回复意见

请完成下方表格:

(*栏/行的出现取决于该问题或其他问题中的选择)

| 注明您能否为贵组织提供一个独特的识别码

|

提供您的独特识别码

|

请选择:

- 是的,一个ISIN代码

- 是的,一个CUSIP编号

- 是的,一个股票代码

- 是的,一个SEDOL代码

- 是的,其他独特识别码,请说明

- 无

|

文本字段[最多50个字符]

|

[添加行]

要求内容

通则

- 如果您的组织有多个独特的识别码,请为每个识别码添加一行。

提供您的独特的识别码(第2栏)

- 确保为独特的识别码输入正确的格式。例如,ISIN代码包括一个两个字母的国家/地区代码,后面是九个字符的字母数字标识符和一个校验位。

Explanation of terms

- ISIN: International Securities Identification Number, a 12-character alphanumeric code used to identify a security, such as a stock or bond. It is structured with the first two letters referencing the country/area of origin of the issuer for the security, in accordance with ISO 3166. The second grouping consists of nine characters made up of digits and letters, which is the unique identifying code for the security. In the U.S. and Canada this is known as the CUSIP number (see below). The final digit is the check digit, which ensures the authenticity of the code.

- CUSIP number: Committee on Uniform Security Identification Procedures number, a 9-character alphanumeric code that identifies a security for the purposes of facilitating clearing and settlement of trades. CUSIPs are used to distinguish, among other reasons, between multiple share classes or bond tranches. CUSIPs are mostly used in the United States and Canada.

- Ticker symbol: A ticker symbol, also known as a stock symbol, is a unique series of letters assigned to a security for trading purposes. Ticker symbols are usually related to the organization’s name, and additional letters denote additional characteristics such as share class or trading restrictions.

- SEDOL code: Stock Exchange Daily Official List code, a 7-character identification code consisting of two parts: a 6-character alphanumeric code and a trailing check digit. SEDOLs issued prior to January 26, 2004 were composed only of numbers. SEDOLs serve as the National Securities Identifying Number for all securities issued in the United Kingdom.

W1当前状况

Module Overview

The promotion of water security for all is supported when companies:

- Reduce their dependency on fresh water sources and track their progress; this is additionally important where fresh water scarcity may pose water quality risks and impacts.

- Collect and share volumetric data on their interactions with water resources.

- Are aware of the water intensity of their value creation.

- Consider water throughout their value chain, beyond the fence-line of their direct operations.

Clean freshwater is becoming increasingly scarce, and this can impact operations relying on large volumes of water – either through absolute availability or through rising costs for water. The information in this module allows CDP data users to build a picture of the dependence of your direct operations and your wider value chain on sufficient amounts of water of a particular quality, currently and for future growth, and where in the value chain most dependence on water lies. To understand an organization’s resilience, it is important to understand the potential to reduce reliance on freshwater sources.

The questions allow your company to demonstrate how well it understands its corporate hydrology by providing information on the monitoring of relevant water aspects, and volumetric data on withdrawals - including withdrawals in water stressed areas, discharges - including discharges by level of treatment, and consumption. CDP also requests companies to comment on their projections for water accounting data.

In addition to volumetric data, in order to protect water quality, companies are requested to report on their emissions to water and their use of hazardous substances.

The module also asks about your engagement activity around water in your value chain and a rationale for it. In regions where water sources are highly restricted, your organization’s water consumption patterns can influence relations with other stakeholders and your access to water can be dependent on those relationships. Engagement can also identify opportunities, such as innovation in your supply chain to reduce dependency and in product design to reduce water-related impacts.

Investors use this current state information to better assess the adequacy, robustness and relevance of your water governance, management and stewardship activities, as well as your disclosure of your water risks and opportunities.

The information requested in sections W1.1 and W1.2 may help companies with their climate-related disclosures in line with the TCFD recommendations which recognise that a reliance on the availability of water exposes a company to climate-related, financial risk.

Note:

- Throughout the water security questionnaire, CDP has broadened the scope of questions about the supply chain to include other phases of the value chain. This will be particularly relevant to companies whose activities may be constrained or otherwise affected by water related issues beyond their direct operations and supply chains. It reflects a widening of company focus to, and greater investor interest in, risk exposure, opportunities and impacts within the value chain.

- W1.2 requests water accounting information at the corporate level. Module 5 asks for facility-level volumetric data - only for facilities that expose your organization to substantive financial or strategic risks, and so it is requested after you have reported your risk exposure in W4.

Disclosure note

CDP’s approach to reporting water accounting data

- When reporting volumetric data please read the guidance for each question as well as the CDP Technical Note on water accounting definitions.

- To reduce their impact on water ecosystems and resources as well as their need to manage water-related risks, organizations should minimize and be able to account for all their interaction with water. For this reason, CDP’s focus is the collection of information to determine how well a company understands the flow of water into and out of its boundaries, and whether they have robust monitoring and accounting in place for all aspects of their water use.

- Definitions: CDP is looking for comparable data, reported against a standard methodology/definition. To ensure the quality of our data and a fair scoring methodology, CDP definitions should be used for all disclosures. This is particularly relevant where there is a lack of standardization. Companies must not provide water accounting data that does not align with the definitions given. Please refer to CDP’s Technical Note on water accounting.

- Units: Volumes must be reported in megaliters per year (1 megaliter = 1 million liters or 1,000 m3) in all questions, unless otherwise stated.

- Blank cells: Please ensure when responding to these water accounting questions that cells are only intentionally left blank if you have no data to disclose. Blank cells are interpreted as non-disclosure, i.e. information is not available due to lack of measurement or choosing not to disclose, and are therefore awarded no points by the scoring methodology.

- Values of zero: entering a zero implies a measurement has been made, and the value is zero. For example, a value of zero consumption reported indicates that no water is incorporated into products or waste products or lost by evaporation from the company. Do not use a zero to indicate a lack of data. If a company enters a zero for discharge, it should provide an explanation.

- Data accuracy: CDP recognizes that there may be uncertainty linked to water accounting information that could impact on data accuracy. Uncertainty can arise from data gaps, assumptions, metering/measurement constraints including equipment accuracy, data management, etc. The emphasis should be on reporting transparently and on providing an explanation for why reported data is uncertain or wholly or partially estimated or modelled, rather than sourced from direct measurements.

Key changes

- Two removed questions: W1.4a (2022) and W1.4d (2022) merged into other value chain engagement questions.

- Six new questions:

- W1.2k requests details of your organization’s emissions of nitrates, phosphates, pesticides, and other priority substances to water.

- W1.4 asks whether products contain hazardous substances.

- W1.4a requests the percentage of revenue associated with products containing hazardous substances.

- W1.5a asks whether suppliers are assessed according to their impact on water security.

- W1.5b asks whether suppliers have to meet water-related requirements.

- W1.5c requests details of water-related requirements for suppliers.

- Modified questions:

- W1.2 has been revised to include measuring and monitoring of emissions to water.

- W1.2b and W1.2d have been revised to request your company’s five-year forecast of water accounting volumes.

- W1.2h, W1.2i, W1.2j have a new column for companies to indicate the primary reason for changes in water accounting volumes.

- W1.5 (2022 W1.4) has been merged with (2022) W1.4d and modified to capture reasons for not engaging suppliers and other value chain partners.

- W1.5d (2022 W1.4b) has been merged with (2022) W1.4a and modified to update the types and details of supplier engagement and to focus on engagement with suppliers with a substantive impact on water security.

- W1.5e (2022 W1.4c) has been restructured from an open text field into a table to allow companies to report in a standardised manner.

- Questions with a revised question dependency:

- Questions no longer dependent on responses to W1.1: W1.2, W1.2b, W1.2d, W1.5 (2022 W1.4)

Sector-specific changes

- Nine new questions:

- Seven for the Agricultural Commodities sector:

- W-FB1.1a/W-AC1.1a, W-FB1.2e/W-AC1.2e, W-FB1.2f/W-AC1.2f, W-FB1.2g/W-AC1.2g, W-FB1.3/W-AC1.3, W-FB1.3a/W-AC1.3a, W-FB1.3b/W-AC1.3b.

- Two for the Coal sector:

- W-MM1.3/W-CO1.3 and W-MM1.3a/W-CO1.3a

- Modified questions:

- W-FB1.1a/W-AC1.1a response options were added to include more agricultural commodities with a critical impact on water security.

- W1.2 has been revised for CO to include measuring and monitoring of entrained water.

- W-OG1.2c has been revised to request your company’s five-year forecast of water accounting volumes.

- Questions with a revised question dependency:

- Questions no longer dependent on responses to W1.1:

- Chemicals sector: W-CH1.3

- Electric utilities sector: W-EU1.2a, W-EU1.3

- Food, beverage, and tobacco & Agricultural commodities sectors: W-FB1.2e/W-AC1.2e, W-FB1.3/W-AC1.3

- Metals and mining & Coal sectors: W-MM1.3/W-CO1.3

- Oil and gas sector: W-OG1.2c, W-OG1.3

- Click here for a list of all changes made this year.

Sector-specific content

- Additional questions presented in:

- W1.1 for Food, Beverage & Tobacco and Agricultural Commodities.

- W1.2 for Electric Utilities, Oil & Gas, Food, Beverage & Tobacco, and Agricultural Commodities.

- W1.3 for Chemicals, Electric Utilities, Food, Beverage & Tobacco, Agricultural Commodities, Metals & Mining, Coal, and Oil & Gas

- Additional response options presented in W1.2 for Oil & Gas, Metals & Mining, and Coal.

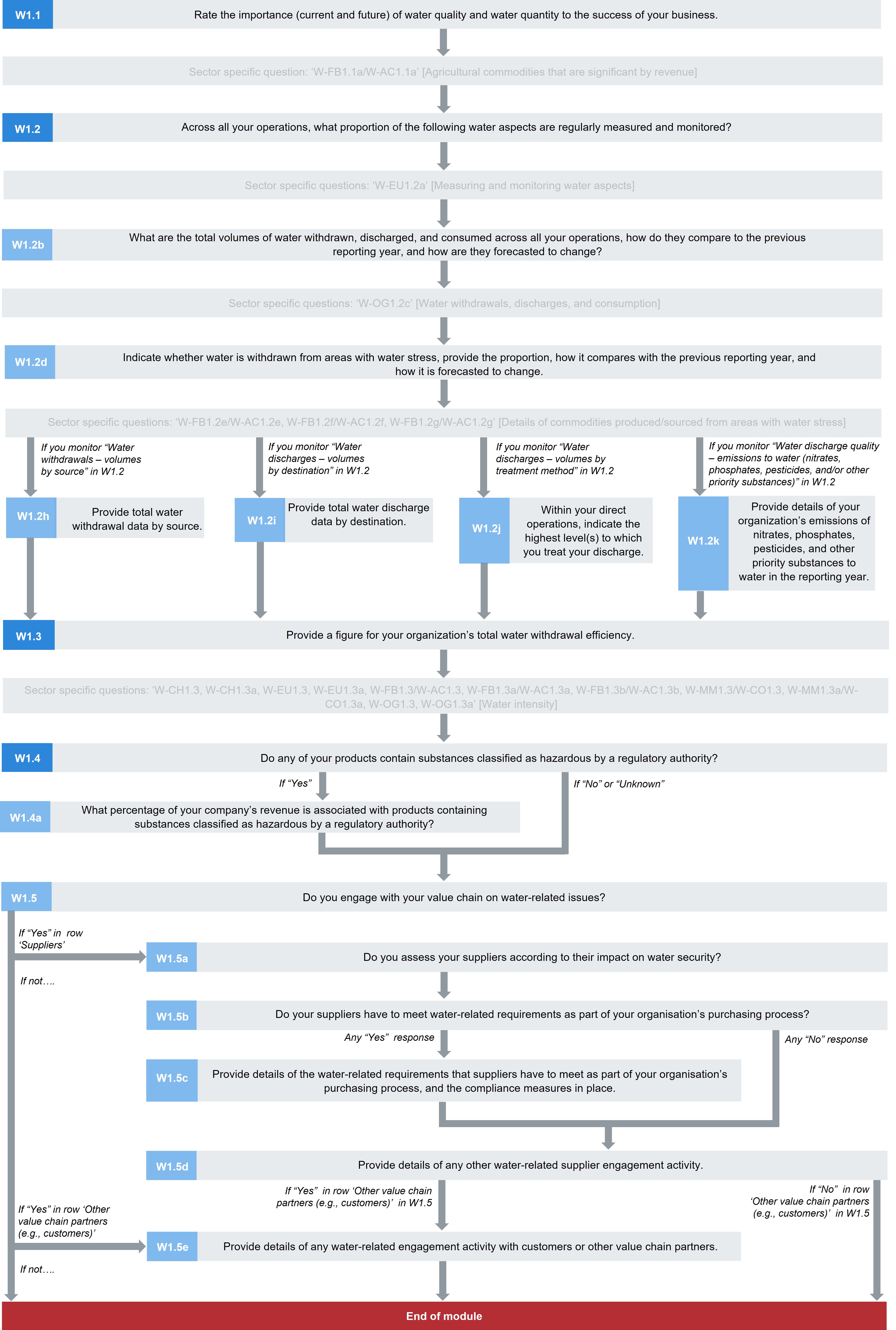

Pathway diagram - questions

This diagram shows the questions contained in module W1. To access question-level guidance, use the menu on the left to navigate to the question.

相关性

(W1.1)请为水质和水量对于贵公司成功的重要性(当前和未来)进行等级评定

对比上一年的变化

修订问题相关性

理由

在社会、生态或经济上存在对优质淡水水源的竞争,或者无法稳定供应的情况下,对这些水源的依赖性可能会给公司带来风险。转而使用低质水资源可以减轻这种依赖性,进而提高公司的水安全,减少淡水水源的压力。

该问题要求公司披露自己对优质淡水资源的依赖性,因为这种依赖将使其难以在不因处理水资源带来额外成本的情况下转而使用低质水资源。

重要性与绝对值无关。例如,公司某一生产环节可能只需要少量的水,但因为当地的其他需求,替代水源的使用受到限制。那么获取那一小部分水的相对重要性就会提高。

评估获得优质和低质水源对贵组织的重要性是判断水相关问题可能给贵组织带来哪些风险的第一步。

该信息帮助投资者了解您在后续的问卷中为什么要披露某些风险。也证明水资源可以限制或提高贵公司的商业战略。

回复意见

请完成下方表格:

| 水质和水量

|

直接使用重要性等级

|

非直接使用重要性等级

|

请详述

|

|

有充足的高品质淡水供使用

|

请选择:

- 一点都不重要

- 不是很重要

- 中立

- 重要

- 关键

- 没有评估

|

请选择:

- 一点都不重要

- 不是很重要

- 中立

- 重要

- 关键

- 没有评估

|

文本字段[最多2,000个字符]

|

|

充足的循环水,半咸水和/或采出水供使用

|

|

|

|

要求内容

通则

- 在回答该问题时,请考虑贵组织对优质淡水和低质水的依赖性,以及该依赖性已经发生或即将发生哪些变化。

- “优质淡水”指的是贵组织活动所用的优质水,这类水只需最简单处理就可用于生活、市政或农业活动,对淡水生态系统安全无害。如果不能使用低质水,那么该公司就具有依赖性。

- “重要性”应该考虑运营所耗水量(多或少)的安全获取需求和在某些时间的可用性;而不仅仅是净耗水量。因此,取水量大的活动应选择“关键”或“重要”,包括排水量也很大导致耗水量相对较少的情况。

- 使用低水质淡水(例如,对于采矿业,Water Accounting Framework from the Mineral Council of Australia的类别2和类别3)的组织应该在第2行说明依赖性(...循环、微咸水和/或采出水水源)。对低质水的依赖性可以降低优质淡水水源的压力。

重要性等级(第2-3栏)

- CDP认识到重要性的评级是主观的。以下类别的描述是为了方便对比,而不是给出严格定义,常见例子如下。

-

关键:若生产地或价值链供水不足(不论是量还是质)会影响未来生产以及公司层面的输出和财务情况,那么该水资源评级为“关键”。若水资源对产品用途有着关键意义,缺水可能会限制销量或者影响声誉。

-

重要:直接或间接运营需要获取充足的优质水资源,尽管这些运营可能用水量不大以及供应链的多样性能够降低风险。

-

一般:只要水量充足,使用水质较差的水资源也可以。

-

不太重要:水资源不是直接或间接运营的关键因素,但是一个地区问题,例如:旱灾、水质差或局部的洪涝都可能会影响当地的运营或供应链。但这并不会影响整体业务。

-

完全不重要:水并不是直接或间接运营中的重要组成部分,水量尤其不需要担心。

-

未进行评估:没有评估运营及价值链需要的水量和水质。

- 在考虑间接使用的重要性评级时,您应该纳入供应链所有阶段(直接业务的上下游)的水资源重要性;例如在供应链中,以及对产品或服务的使用/消耗。

请详述(第4栏)

- 说明价值链直接和间接环节中水资源的(包括优质淡水和低质水)主要用途。描述水资源在价值链中的分配;如果可能,请提供百分比。

- 描述如何确定上述水质和水量(包括优质淡水和低质水)的重要性评级。

- 请说明未来水资源依赖性将发生哪些变化,并加以解释。

Explanation of terms

- Direct operations: An organization’s operations include anything it does itself for the purpose of producing goods and services and maintaining the functionality of the business. This covers any internal supply chains between the organization’s business units. For example, a business unit within a company that supplies components to another business unit within the company would be considered part of the organization’s direct operations.

- Direct water use: Includes all water that is used for activities within your organization (as defined by your ‘reporting boundary’).

- Good quality freshwater: Any water used for your organization’s activities that must be of a quality requiring only minimal treatment to be acceptable for domestic, municipal or agricultural uses or safe for freshwater ecosystems. A company is considered dependent on this if it is not possible to use a lower quality water instead. Water quality can refer to physical, chemical, biological, and organoleptic properties of water. ‘High quality’ fresh water sources, of potable standard, are typically characterized as having concentrations of dissolved solids less than 1,000 mg/l.

- Indirect water use: Includes all water use that takes place anywhere within your value chain outside your direct operations and direct control. This includes water use upstream of your direct operations, use such as by your suppliers, and downstream, for example water needed for the use of your products.

- Sufficient amounts of recycled, brackish and/or produced water: This refers to any low quality water requiring significant treatment to be acceptable for human consumption or other purposes, and for which the source can be easily substituted. Water quality can refer to the physical, chemical, biological, and organoleptic properties of water.

- Water availability: The natural runoff (through groundwater and rivers) minus the flow of water that is required to sustain freshwater and estuarine ecosystems and the human livelihoods and well-being that depend on these ecosystems. Water availability typically varies within the year and also from year to year. Water availability might be reduced by decreases in both the water quantity and quality of water resources (Adapted from CEO Water Mandate's "Corporate Water Disclosure Guidelines").

- Water quality: Refers to the physical, chemical, biological and organoleptic (taste-related) properties of water (see CDP’s definition for “Good quality freshwater”) (adapted from CEO Water Mandate's "Corporate Water Disclosure Guidelines").

全公司范围水核算

(W1.2) 根据贵公司所有的运营活动,以下哪些水指标有进行定期测量和监测?

问题依赖关系

- 您对W1.2的回答将决定后面哪个问题会出现。若修改W1.2的回答,可能会删除相关问题的数据。在这种情况下,请务必重新输入所有相关问题的数据。

- 如果在W1.2选择“未监测”或者“不相关”,您将无法在本章节披露相关的体积数据。问题指南注明了该问题是否为依赖性问题。

对比上一年的变化

修改了问题;修订了问题相关性

理由

此问题允许贵公司向投资者、客户和其他数据用户说明各项用水指标的监测程度。全面的水资源核算是了解水资源对您业务的重要性以及任何水资源对您业务潜在影响的第一步。这些数据也可能与公司的合规性相关。

连接到其它框架

标准普尔(S&P)全球企业可持续发展评估

耗水量

用水

CEO水资源纲领

当前状况:成果

回复意见

请完成下方表格:

(*栏/行的出现取决于该问题或其他问题中的选择)

| 0

|

1

|

2

|

3

|

4

|

| 水指标

|

场地/设施/运营中所占比例%

|

测量频率*

|

测量方法

|

请详述

|

|

取水量 ——总量

|

请选择:

- 未监测

- 少于1%

- 1-25

- 26-50

- 51-75

- 76-99

- 100%

- 不相关

|

请选择:

- 持续不断

- 每日

- 月度

- 每季度

- 年度

- 未知

- 其他,请说明

|

文本域[最多500个字符]

|

文本域[最多1,000个字符]

|

|

取水量——按来源分

|

|

|

|

|

|

[仅限金属和采矿以及煤炭行业] 与您的金属和采矿和/或煤炭行业活动相关的夹带水——总量

|

|

|

|

|

|

[仅针对石油和天然气行业]贵公司石油和天然气行业活动的采出水——总量

|

|

|

|

|

|

取水质量

|

|

|

|

|

|

排水量——总量

|

|

|

|

|

|

排水量——按排放地点分

|

|

|

|

|

|

排水量——按处理方法分

|

|

|

|

|

|

排水质量——按污水处理后的标准出水参数分

|

|

|

|

|

|

排水质量——排放到水中(硝酸盐、磷酸盐、杀虫剂和/或其他优先化学物质)

|

|

|

|

|

|

排水质量——按温度分

|

|

|

|

|

|

耗水总量

|

|

|

|

|

|

循环/再利用水

|

|

|

|

|

|

向所有员工提供功能完善,经过安全管理的水、环境卫生和个人卫生设施(WASH)

|

|

|

|

|

要求内容

- 注:在公共电力、金属和采矿、煤炭或石油和天然气行业作出答复的组织应在“所要求的内容”一节末尾参考关于这一问题的其他行业具体指导意见。

通则

- 该问题要求提供针对各种水指标监测的全公司回复。“在所有操作中”是指包含在填报范围内的所有实体,如W0.5所示。

- 在回答这个问题之前,请参阅CDP的水核算定义(包含在 CDP技术说明 - 水核算定义中)。

- 如果您没有收集业务中有关这些水指标的数据,则只应选择“未监测”。如果您有来自任何信息来源的数据,则应通过在“场地/设施/运营的百分比”栏中指示代表的场地/设施/运营的百分比来反映这一点。

- 如果您的填报范围内有的业务无法提供水核算信息,请在第4栏中说明覆盖范围。

- 第1栏填报的场地/设施/运营的比例不被视为贵组织监测的总水量比例的指标。该比例仅提供监测工作的组织覆盖范围。

- 请注意,对于第1栏,“场地/设施/运营”可能包括各种各样的业务运营、资产、固定建筑、工厂或场地等。第4栏用于提供公司具体解释。

水指标(第0栏)

- 每种水指标的定义都包含在这个问题的“术语解释”中(并重复出现在词汇表中)。

场地/设施/运营的百分比(第1栏)

- 请选择贵组织定期(至少一年一次)测量和监测的设施每个指标的比例,例如一家公司整体运营100个设施,并定期测量和监测50%(50个设施)的取水总量,则选择“26-50”。

- 如果某项水指标只与贵组织部分设施有关,请填报贵组织测量和监测涉及该指标的设施所占的百分比,并在第4栏中作出解释。例如,一家公司在其全部业务中拥有100个设施,其中涉及到“按污水参数划分的排水质量”这一指标的仅与50%(50个设施)的运作相关。如果公司定期测量和监测所有相关设施(50个设施)的“按污水参数划分的排水质量”,则选择“100%”,并在第4栏说明已考虑该水指标的相关性。

- 如果贵组织在监测某一指标中存在技术上不可行或技术上不可取的情况,则选择“不相关”; 例如,运营不会消耗水,因此不需要进行测量,或您只需排放到一个目的地,因此不要监测排放目的地,或贵公司因为成本过高,不会对水资源进行回收/再利用。在第4栏中作出解释。

- 如果贵公司没有监测这方面的情况,请选择“未监测”,尽管技术上可行或可取。 例如,贵公司确实对水资源进行了回收/再利用,但尚未在企业一级进行监测。在第4栏中作出解释。

测量频率(第2栏)

- 如果在任何水指标行第1栏中选择了“未监测”或“不相关”,则该栏不显示。

- 如果您在不同的场所/设施/操作中有多个测量频率,请选择适用于您的大多数场所/设施/操作的频率。

- 请注意,本栏要求提供的是测量频率数据,而不是报告或信息汇编的频率。

测量方法(第3栏)

- 如果在任何水指标行第1栏中选择了“未监测”或“不相关”,则该栏不显示。

- 说明您水资源方面使用的测量方法,例如,通过直接监测、水文模型估计或其他二级信息来源。

- 如果您表明您监测“取水水质”以确定水是否适合其预期用途,您可以在此栏中填写一个测量参数列表。这一行为联合国环境淡水全球环境监测系统(GEMS/Water)提供数据支持,这是一个长期项目,用于生成全球水质数据流。

请详述(第4栏)

- 如果您在第1栏中选择了“不相关”,请简要说明为什么该水方面信息与您的公司不相关,以及该水方面信息将来是否会相关。

- 如果您在第1栏中选择了“未监测”,请简要说明贵组织为何未监测水方面信息。

- 如果您在第1栏中选择了一个百分比:

- 对第1栏的回复进行说明,例如为什么贵组织按照这样的比例计量/监测这些水指标,并说明排除了哪些场地/设施/运营以及原因。

- 如果您在第1栏中的回复涉及设施、场所或运营或其他类型的分组,请说明并解释您对于这些分组的定义; 例如“对我们公司而言,'设施'是指我们的仓库和零售店”; “我们在这一行的回复涉及到我们不同地理位置的业务。“我们没有设施或场所,因为我们提供了一系列不限于特定位置的服务”。

Explanation of terms

- Boundaries of your organization: This term is key within CDP water accounting definitions and is a management boundary, rather than a physical boundary or a legal entity. Water is considered to have crossed the boundary of your organization, at either the corporate or site level, when your organization in any way uses it, comes into contact with it, is required to manage it or when it becomes incorporated into your products. It therefore includes any water use and management by your organization outside of its physical corporate fence; for example, to provide a street cleaning service or in fields remote from a processing plant. The scope of this organizational boundary is defined by your chosen reporting boundary.

- Measurement: The collection of quantified data for a water aspect - either as a single volume/quality figure or an aggregation of volumes/quality figures.

- Monitoring: This is the tracking of measurements over time, i.e. a trend or indication of change in measured figures.

- Produced water: Water which enters the organization’s boundary as a result of the extraction, processing, or use of any raw material, so that it must be managed by the organization. When reporting to CDP, this water should not be counted as recycled water when put to use within a single cycle of a business process. Examples of produced water include moisture derived from vegetation such as in sugar cane crushing and the water content in crude oil. (Note that companies with oil and gas activities should refer to CDP’s sector specific guidance for this water aspect).

- Entrained water (Metals & mining and coal sectors only): In the mining industry, entrained water refers to the volumes of water in the raw material.

- Produced water (Oil & gas sector only): Water that is brought to the surface during the production of hydrocarbons including formation water, flow-back water and condensation water (adapted from IPIECA's "Oil and gas industry guidance on voluntary sustainability reporting", 4th edition, 2020).

- Recycled/reused water: Water and wastewater (treated or untreated) that has been used more than once before being discharged from the organization’s boundary, so that water demand is reduced. This may be in the same process (recycled), or used in a different process within the same facility or another of the organization’s facilities (reused). It can include wastewater re-used from household processes such as washing dishes, laundry, and bathing (grey water).

- Safely managed WASH services: The universal provision of safely managed water, sanitation, and hygiene services has dedicated targets within the Sustainable Development Goals (SDG 6.1 and 6.2). As a minimum, this disclosure refers to a company’s tracking of its provision of drinking water for all workers, available when needed and from sources compliant with faecal and chemical standards, as well as sanitation facilities where excreta are safely disposed in situ or transported and treated offsite.

- Water consumption: The amount of water that is drawn into the boundaries of the organization and not discharged back to the water environment or a third party over the course of the reporting year.

- Water discharges – total volume: The sum of effluents and other water leaving the organization’s boundary and released to surface water, groundwater water or to third parties over the course of the reporting year.

- Water discharges – volumes by destination: This refers to the proportion of your discharges that are tracked to different types of discharge destinations; e.g. freshwater, brackish surface water/seawater, groundwater, or third parties.

- Water discharges – volumes by treatment method: This refers to the proportion of your discharge that you track according to treatment method applied before being returned to the environment - primary, secondary, or tertiary treatment types etc. Different industries will have different requirements to meet compliance standards, or a company may have an internal standard they adhere to.

- Water discharge quality data – by standard effluent parameters: This refers to the quality of your discharged water/effluents tracked according to parameters such as Chemical Oxygen Demand (COD), Biological Oxygen Demand (BOD) or Total Suspended Solids (TSS). The specific choice of quality metrics will vary depending on the organization’s products, services, and operations but should be consistent with those used in the organization’s sector, and may need to vary depending on national or regional regulations.

- Water discharge quality – emissions to water (nitrates, phosphates, pesticides, and/or other priority substances): This refers to the

mass of any solid, liquid or gaseous pollutants or contaminants, such as

nitrates and pesticides, released to bodies of water by your organization.

- Water discharge quality data – temperature: This refers to the temperature of your discharged water/effluents. Though not yet a standard effluent parameter in many industries, thermal pollution can play a significant role in ecosystem degradation by altering levels of dissolved oxygen and harming wildlife.

- Water diversions (Metals & mining and coal sectors only): According to the Water Accounting Framework from the Mineral Council of Australia

water diversions are flows from an input to an output without being utilized by the operational facility. The flow is not stored with the intention of being used in a task or treated.

- Water withdrawals – total volumes: The sum of all water drawn into the boundaries of the organization (or facility) from all sources for any use over the course of the reporting period. (Source: adapted from GRI Standards Glossary 2016).

- Water withdrawals quality: This refers to the quality of raw water that your company draws into its boundary (from sources, such as rivers, lakes, groundwater and coastal zones).

- Water withdrawals – volumes by source: This refers to the proportion of withdrawals that your organization can trace to different types of water withdrawal source e.g. freshwater, brackish surface water/ seawater, produced water and third party sources, and a breakdown of groundwater by renewable and non-renewable sources.

- Water recycled/reused: Water and wastewater (treated or untreated) used more than once before being discharged from the organization’s boundary, so that water demand is reduced. This may be in the same process (recycled), or in a different process within the same facility or another of the organization’s facilities (reused).

- Water recycled/reused (Oil & gas sector only): Water and wastewater (treated or untreated) that has been used more than once, in order to reduce water withdrawals (adapted from IPIECA’s "Oil & gas industry guidance on voluntary sustainability reporting", 4th edition, 2020).

Example response

| 0

|

1

|

2

|

3

|

4

|

| Water aspect

|

% of sites/facilities /operations

|

Frequency of measurement*

|

Method of measurement*

|

Please explain

|

|

Water withdrawals – total volume

|

100%

|

Continuously

|

We measure water withdrawals in real-time, using "in-place" flow meters.

|

Total water withdrawal volume is one of our environmental key performance indicators and is used to track improvements in water efficiency. We report this information at an internal global level quarterly, and report data externally on an annual basis.

Our responses in this question refer to our sites, and for our company, ‘sites’ refer to where our mining, processing, and R&D operations take place. All of our sites are monitored for water withdrawal volumes.

|

|

Water withdrawals – volumes by source

|

100%

|

Continuously

|

The water sources are known and recorded for all of our sites. The majority of sites measure water withdrawal volumes in real time through “in-place” flow meters. For a few of our sites, water withdrawal volumes and sources data is obtained from water utility providers.

|

Water withdrawal volumes by source are monitored at 100% of our operations. Measuring this aspect allows us to identify priority areas and to further refine water-related targets and performance improvements. In addition, overall exposure to potential water risks (source dependency) can be quickly evaluated on a site by site basis with detailed information on water withdrawal volumes by source.

|

|

[METALS & MINING and COAL SECTORS ONLY] Entrained water associated with your metals & mining and/or coal sector activities – total volume

|

100%

|

Monthly

|

We measure the moisture content of the ore milled and the volumes of ore milled. The entrained water volumes can then be calculated using these two parameters.

|

Entrained water volumes are not relevant to all our operations. They are only relevant to our mining sites, and we monitor entrained water at 100% of these sites.

|

|

[OIL & GAS SECTOR ONLY] Produced water associated with your oil & gas sector activities – total volume

|

Question not applicable

|

Question not applicable

|

Question not applicable

|

Question not applicable

|

|

Water withdrawals quality

|

100%

|

Daily

|

Water withdrawals quality is monitored at the site level using automatic water samplers and lab testing.

Parameters measured include BOD, TSS, and temperature.

|

100% of our operational sites are monitored for this water aspect. The data is consolidated into local databases on a monthly basis. Due to environmental and water permits, figures are reported on an annual basis to the authorities.

|

|

Water discharges – total volume

|

100%

|

Continuously

|

We use flow meters to measure discharge volumes in real-time.

|

100% of our operational sites are monitored for this water aspect and this is considered part of the usual management for our sites.

|

|

Water discharges – volumes by destination

|

100%

|

Continuously

|

We use flow meters to measure discharge volumes in real time. The destination of the discharge is known and recorded for all sites

|

100% of our operational sites are monitored for this water aspect and this is considered part of the usual management for our sites.

This aspect is relevant because our sites treat and discharge water volumes to freshwater bodies. We are committed to reducing water pollution. As part of our compliance with standards and regulations, we monitor the volumes of our discharges by destination.

|

|

Water discharges – volumes by treatment method

|

100%

|

Monthly

|

We keep detailed records of the discharge treatment level and methods at all sites.

|

100% of our operational sites are monitored for this water aspect and this is considered part of the usual facility management for our sites. Our discharges are treated to secondary level or tertiary level, depending on the operations of the site.

This aspect is relevant because our sites treat and discharge water volumes to freshwater bodies. We are committed to reducing water pollution. For this, we are required to ensure that quality and quantity of discharged water complies with standards and regulations.

|

|

Water discharge quality data – by standard effluent parameters

|

100%

|

Daily

|

We monitor water discharge quality by standard effluent parameters at the site level using automatic water samplers and lab testing.

Key measures such as pH are monitored continuously through on-site monitoring systems and samples are collected on a daily basis to analyse metal concentration and load, 5-day biological oxygen demand (BOD), and total suspended solids (TSS).

|

These parameters are monitored daily/continuously (pH is monitored continuously and samples for other parameters are taken on a daily basis). It is considered part of the usual management for our sites.

This aspect is relevant because our sites treat and discharge water volumes to freshwater bodies. We are committed to reducing water pollution. For this, we are required to ensure that quality and quantity of discharged water complies with standards and regulations.

|

| Water discharge quality –emissions to water (nitrates, phosphates, pesticides, and/or other priority substances)

|

Not monitored

|

Question not applicable

|

Question not applicable

|

This water aspect is not monitored in our sites; discharge quality is only monitored by standard effluent parameters and temperature. We are planning to monitor this aspect in the next reporting year.

|

|

Water discharge quality data – temperature

|

100%

|

Daily

|

We use sensors specifically designed to monitor temperature in wastewater and industrial effluent treatment applications at all of our sites. The online sensors (thermometers) are factory calibrated and regularly maintained.

|

Each site controls the quality data of water discharged locally and measures this on a daily basis.

|

|

Water consumption – total volume

|

100%

|

Monthly

|

We measure our water consumption monthly using a water balance which considers water withdrawals and water discharges. Withdrawals and discharges are measured with flow meters.

|

Total water consumption is calculated monthly from water withdrawals volumes minus water discharges in all our operational sites and this is reported through our global performance reporting system.

|

|

Water recycled/reused

|

100%

|

Monthly

|

The method of measurement will vary depending on the site. Some sites use flow meters and others estimate the amount reused based on the reduction of water withdrawals.

|

Volumes of recycled/reused water are monitored at all of our sites and the annual inventory of water usage volumes is executed based on ISO 14046:2014 to confirm the data.

|

|

The provision of fully-functioning, safely managed WASH services to all workers

|

100%

|

Monthly

|

We use an internal audit excel tool to measure progress towards WASH services for employees.

|

This aspect is relevant because our company recognizes the importance of closing the gap on access to WASH and we are recognized as a WASH Pledge signatory. We are committed to implementing access to safe water, sanitation and hygiene at the workplace at an appropriate level of standard for all employees in all sites.

|

Additional information

The provision of safely managed WASH services at the workplace, and respecting the human rights to water and sanitation

The provision of safely managed WASH services at the workplace (and extending such expectations to other actors within its value chain) is aligned with the aims of the Sustainable Development Goals (SDG 6.1 and 6.2) and the UN Human Rights Council endorsed Guiding Principles on Business and Human Rights. These are established and authoritative global reference points on how companies should respect human rights in their own activities and business relationships, focusing on the risks to people rather than the risks to the business. Provision requirements may also be linked to Health and Safety regulations applicable to your operations.

In practice, companies need to implement due diligence to identify actual and potential impacts on human rights and to prevent, mitigate, and remediate them. This could mean a company may need to collaborate with others in the basin to reduce their collective water use when withdrawals limit the water availability for local communities in a way that impacts their right to water.

Water withdrawals quality and GEMS

The UN Environment Global Environment Monitoring System for Freshwater (GEMS/Water) provides the world community with sound data on water quality to support scientific assessments and decision-making on the subject. Surface and groundwater quality monitoring data collected from the global GEMS/Water monitoring network is shared through the GEMStat information system.

Within UN Environment, GEMS/Water was identified as being the mechanism to support countries/areas to fulfill their reporting obligations for the UN Sustainable Development Goals. GEMS/Water provides appropriate support, based on capacity needs at national and regional levels, and develops training for delivery in countries/areas all over the world.

(W-EU1.2a)

这个问题仅适用于在公共电力行业有活动的组织 - 除非您选择查看这些特定行业的问题,否则不会在此处显示。

(W1.2b)贵组织所有运营活动的取水总量、排水总量和耗水总量是多少,与上一报告年相比有何变化?以及预计它们将来会有怎样的变化?

对比上一年的变化

修改了问题;修订了问题相关性

理由

这个问题鼓励公司在公司层面全面了解其水平衡情况,并评估水需求的预期趋势,鼓励向不对河流、湖泊、含水层和溪流构成威胁的商业模式过渡。

总量可以体现组织作为水用户的相对重要性,并为其他计算提供基准数字。除了趋势数据外,这些数据还可以表明未来供水中断或水成本增加造成的风险等级。

耗水量测量报告周期内不可再供生态系统或当地社区使用的水量。填报用水量有助于组织了解由于取水对下游供水量的影响而产生的整体影响规模。

连接到其它框架

SDG

目标6:改善饮水和公共卫生

标准普尔(S&P)全球企业可持续发展评估

耗水量

用水

CEO水资源纲领

当前状况:成果

回复意见

请完成下方表格:

| 0

|

1

|

2

|

3

|

4

|

5

|

6

|

| 水指标

|

体积(兆升/年)

|

对比上一报告年

|

与上一报告年比较,产生差异的主要原因

|

五年预测

|

预测变化产生的主要原因

|

请详述

|

|

取水总量

|

数字字段[请输入

0到+/- 999,999,999,999之间的数字,最多保留小数点后两位]

|

请选择:

- 低很多

- 低一些

- 基本持平

- 高一些

- 高很多

- 首次度量

|

请选择:

- 核算方法的变化

- 撤消对水资源密集型技术/工艺的投资

- 设施关闭

- 设施扩建

- 业务活动增加/减少

- 效率提高/降低

- 投资智能水技术/工艺

- 已达到可减少量的最大值

- 兼并与收购

- 未知

- 其他,请说明

|

请选择:

|

请选择:

- 核算方法的变化

- 撤消对水资源密集型技术/工艺的投资

- 设施关闭

- 设施扩建

- 业务活动增加/减少

- 效率提高/降低

- 投资智能水技术/工艺

- 已达到可减少量的最大值

- 兼并与收购

- 未知

- 其他,请说明

|

文本字段[最多2,000个字符]

|

|

排水总量

|

|

|

|

|

|

|

|

总耗水量

|

|

|

|

|

|

|

要求内容

- 请注意:对公共电力、金属和采矿或石油和天然气行业的请求作出答复的组织应在“所要求的内容”一节末尾参考关于这一问题的其他行业具体指导意见。

通则

- 该问题要求您填报公司范围内的水量数据汇总。如果您没有汇总数据,如果您正在估计或推算完整的覆盖范围,请在第6栏(请详述)中给出解释。

-

请注意:只有填报数据为零而不是缺少数据的情况下,才可使用0(零)。

- 在完成这个问题之前,请参考CDP的水资源核算定义。请使用兆升/年为单位填报在报告年份的水量数据(您在回复W0.2时使用的时间段)。(1兆升=1百万升或1000 m3)

-

冷却水:冷却水(淡水或海水)通常抽取量大,并排放回其原始来源,损失或质量变化可以忽略不计。但是,这应该包含在您的水核算中。

-

雨水:如果公司管理雨水(例如收集雨水使用或储存,或者是防止水淹)或者依赖雨水进行产品生产或者是服务交付,就应该尝试预估雨水量,并将其作为水文系统在公司界限内提供的取水量进行披露。请注意,在一些管辖范围,雨水被视为取水来源,各组织必须填报其收集和使用情况。

- 只有在水量平衡误差小于5%的情况下,公司才可以选择将收集的雨水和生活污水从其取水/排水量中剔除。(这可以避免您的排水量大于取水量)。

- 包括雨水有助于企业更好地了解对水的依赖和风险。对于一些公司来说,降水/雨水量可能构成现场水位的主要来源。这包括需要管理的径流。在这些情况下,从取水量和排水量的水核算中排除雨水可能无法真实反映现场水平衡的情况。此外,使用雨水代替其他当地淡水资源可能会减少影响。

水量(第1栏)

- 请使用兆升/年为单位填报在报告年份的水量数据(您在回复W0.2时使用的时间段)。(1兆升=1百万升或1000 m3)

- 在取水方面,可以从几个来源收集数据,包括“水表、水费单、从其他现有水数据得出的计算,或组织自己的估计(在既没有水表,也没有水费单或参考数据的情况下)”。

- 在决定您的取水、排水或耗水是否可以报告为0(零)之前,请参阅CDP关于水核算定义的技术说明。

- 如果填报“零耗水”,请注意检查您的排水量。评分者将检查排水量和取水量的(大致)平衡。

对比上一报告年/5年预测(第2栏、第4栏)

- CDP并未针对“高得多”的水量定义阈值,而是仅仅定义“较高”的(或“低得多”/“较低”)阈值。CDP要求许多用水差异很大的不同行业提供这一信息,因此很难提供一个有意义的普遍阈值(因为比例将等同于不同的绝对值和影响)。

- CDP建议您为“高得多”(和“低得多”)的水量定义自己的阈值,并一直使用它,以便该问题的报告数据具有可比性,并且数据使用者可以每年更有效地跟踪您的水核算。应在第6栏(请详述)对这些阈值提供具有公司针对性的说明。

- 为“高很多”/“更高”(以及“低很多”/“更低”)定义的阈值应与第2栏和第4栏相同。

-

对比上一报告年:如果数据不是以前填报过的,而是收集的,您可以选择指出与前一年比较后的差异或选择“首次测量”。在这两种情况下,请使用“请说明”栏提供有关所报告信息的详细信息。

与上一报告年比较的主要原因/预测变化产生的主要原因(第3、5栏)

- 选择最重要的原因。

- “已达到可减少量的最大值”指的是已经达到节水极限的情况,例如已经建立了闭环水循环系统,并且无法实现进一步的减排。

请详述(第6栏)

- 列出必要的语境信息,以辅助理解与上一报告年度和五年预测进行比较差异产生的主要原因,以及列出水量数据是如何编制的,例如所使用的任何标准、方法和假设。

- 如果您因为没有数据而让第1栏留空,请描述报告数据遇到的障碍,以及收集和报告计划。

- 请描述每个来源的水量与上一年相比“高很多”和“低很多”的阈值。描述与五年预测相比,数量变化“高很多”和“低很多”的阈值。

- 如果在第1栏中的“总计”数字中有任何程度的不确定性,或者如果有一个估计的数字,您应该在这一栏中加以说明,并给出不确定的范围。不确定性可能来自数据缺口、假设、计量/测量限制,包括设备精度、数据管理等。

-

请注意:CDP预计取水、排水和耗水数据将保持平衡(大约;+/-5%),因此,如果有不能这样做的合适理由,请在此说明。

请解释-关于用水量的补充指南(第3行)

- 对于“耗水量”行,您应该指出您的数字是基于本地测量的汇总、本地计算的聚合,还是公司范围内的计算(例如,用提取量减去排放)。

- 如已知,请提供该数据的明细(参考CDP的耗水量定义)和简要解释。详细情况包括:

-纳入产品、作物或废物的水量;

-蒸发或泄露的水量;

-人类或牲畜的消耗量;

-以受控方式储存的净水量;

-储存供今后使用的净水量;

-排除公司界限外排水量的水量。

- 在这种情况下,解释负消耗数字是很重要的。这将表明,您在报告年份的排水量大于取水量-例如,由于储存水的净释放。

Explanation of terms

- Water balance: An account of the volumes of water flowing into and leaving an organization across its boundary. When the two volumes are equal, the net water balance will be zero.

- Water consumption: The amount of water that is drawn into the company boundary and not discharged back to the water environment or a third party. It is important to distinguish the term ‘consumption’ from the term ‘water withdrawal’ or ‘water use’. Water consumed is water that during the reporting year:

- has been incorporated into products, crops or waste;

- has evaporated or transpired;

- consumed by humans or livestock;

- has been stored in a controlled manner because it is polluted to the point of being unusable by other users, and so that it does not leave the organization’s boundary;

- has been stored during the reporting year for use or discharge in a subsequent reporting period;

- is otherwise excluded from discharges out of the organization’s boundary so that it is no longer available for use by the ecosystem or local community.

Consumption may be measured directly or modelled, or it can be calculated by subtracting the total water discharge from company boundary from total water withdrawn into the company boundary during the reporting period. As CDP data users require comparability, all disclosing companies should use this method.

If the company discharges more water than it withdraws, for example, because it has used and then discharged previously stored water, a negative consumption value is possible. This would indicate a net contribution to the water environment in the reporting year.

- Water discharges – total volumes: The sum of effluents and other water leaving the organization’s boundary and released to surface water, groundwater water or to third parties over the course of the reporting year. This includes all water leaving the company boundary, whether it is:

- considered used or unused;

- released through a defined discharge point (point source discharge), or;

- released over land in a dispersed or undefined manner (non-point source discharge), or as;

- wastewater removed from the organization via truck.

Water discharge can be authorized (in accordance with discharge consent) or unauthorized (if discharge consent is exceeded).

- Water diversions (Metals & mining and coal sectors only): According to the Water Accounting Framework from the Mineral Council of Australia water diversions are flows from an input to an output without being utilized by the operational facility. The flow is not stored with the intention of being used in a task or treated.

Example response

| 0

|

1

|

2

|

3

|

4

|

5

|

6

|

| Water aspect

|

Volume (megaliters/year)

|

Comparison with previous reporting year

|

Primary reason for comparison with previous reporting year

|

Five-year forecast

|

Primary reason for forecast

|

Please explain

|

|

Total withdrawals

|

32,596,140

|

About the same

|

Increase/decrease in efficiency

|

Lower

|

Investment in water-smart technology/process

|

Description for ‘’comparison with previous reporting year” and “five-year forecast” thresholds: Deviation +/- 5% = about the same; Deviation between +/- 5-15% = higher / lower; Deviation > +/- 15% = much higher / lower.

Water withdrawals remained about the same compared to the previous year despite an increase in production thanks to water efficiency measures and divestment from thermal coal operations. These actions form part of our 2020-2025 sustainability strategy.

In the future, we expect withdrawals to decrease with increased investments in water-smart technologies, water efficiency measures, and water circularity.

|

|

Total discharges

|

23,827,590

|

Higher

|

Increase/decrease in efficiency

|

Lower

|

Investment in water-smart technology/process

|

Description for ‘’comparison with previous reporting year” and “five-year forecast” thresholds: Deviation +/- 5% = about the same; Deviation between +/- 5-15% = higher / lower; Deviation > +/- 15% = much higher / lower.

The increase in total discharges can be explained by a decrease in water consumption as well as improved water efficiency.

In the future, we expect water discharges to decrease with increased investments in water water-smart technologies, efficiency measures, and water circularity.

|

|

Total consumption

|

8,779,710

|

Lower

|

Divestment from water intensive technology/process

|

Lower

|

Investment in water-smart technology/process

|

Description for ‘’comparison with previous reporting year” and “five-year forecast” thresholds: Deviation +/- 5% = about the same; Deviation between +/- 5-15% = higher / lower; Deviation > +/- 15% = much higher / lower.

Total water consumption figures are based on measured primary data on water withdrawal and water discharge at all operations (C= W - D).

The lower consumption volume can be primarily attributed to divestment from thermal coal operations. Increases in water efficiency measures have also contributed to the decrease in water consumption.

We expect water consumption to continue decreasing with the implementation of the remainder of our 2020-2025 sustainability strategy, including water-smart processes, water circularity and an optimized water management to achieve a continuous improvement of the water usage ration.

|

(W-OG1.2c)

这个问题仅适用于在石油和天然气行业开展活动的组织 - 除非您选择查看这些特定行业的问题,否则不会在此处显示。

(W1.2d)说明是否从存在水资源压力的地区取水,并提供取水比例、与上一报告年的比较情况以及预测变化情况。

对比上一年的变化

修改了问题;修订了问题相关性

理由