Copyright © 2023 CDP Worldwide. All rights reserved.

CDP Climate Change Questionnaire Preview and Reporting Guidance 2023 - Version Control

| Version number

|

Release / Revision date

|

Revision summary

|

| 1.0

|

Released: January 11, 2023

|

Publication of the 2023 questionnaire preview and reporting guidance.

|

| 1.1

|

Revised: February

10, 2023

|

- C6.1 and C-CE7.4/C-CH7.4/C-CO7.4/C-EU7.4/C-MM7.4/C-OG7.4/C-ST7.4/C-TO7.4/C-TS7.4: Guidance on the use of biogas certificates for scope 1 reporting has been updated.

- C8.2e: Question dependency updated so that C8.2e is not presented to companies who indicate in C8.2 that they do not consume any purchased or acquired electricity, heat, steam or cooling.

|

| 1.2

|

Revised: February 14, 2023

|

- C3.5: Companies in the financial services sector will not be presented with the option “At the company and activity level” in column 2 as these companies are not required to report alignment against the EU Taxonomy for Sustainable Activities until January 2024.

- C3.5, C3.5a, C3.5b and C3.5c: Guidance has been updated to clarify the data being requested, and to provide links to further external resources including new EU Commission FAQs on the EU Taxonomy.

- Connections to other frameworks: for financial services institutions, connections to the Net Zero Asset Managers (NZAM) initiative have been removed for C3.3, and added for C-FS2.2b, C-FS2.2e, C3.1, C3.5, C3.5a, C4.1, C4.3c, C11.2, C12.4, C-FS14.1, C-FS14.1c, and C-FS14.3a.

- FW-FS4.3: In column 2, agricultural commodities sugar, tobacco and rice will now only be presented to companies who indicate in C-FS0.7 that they finance or insure industry sectors with a critical impact on water security.

|

| 1.3

|

Revised: March 23, 2023

|

- C2.2: Guidance updated to request that companies include an explanation of the frequency of assessment and time horizons reported when describing their process for identifying, assessing and responding to climate-related risks and opportunities.

- C-CO4.2d and C-OG4.2d: Guidance updated to request that companies reporting a separate methane reduction target in C4.1a/b provide details of the target in C-CO4.2d/C-OG4.2d.

- C-CO4.8 and C-OG4.8: Guidance updated to request that where flaring is not relevant to a company’s operations, they include examples and timelines in their explanation to illustrate why it is not relevant.

|

| 1.4

|

Revised: April 17, 2023

|

- C3.5a and C3.5b: Example responses added for questions on taxonomy alignment.

|

| 1.5

|

Revised: June 9, 2023

|

- C3.2a: Guidance updated to specify that only companies with financial services as their primary sector should use the “NGFS scenarios framework" dropdown.

- C-FS14.3a: Drop-down added for companies to indicate if they do not have commercial/corporate/SME clients to report on in this question.

|

| 1.6

|

Revised: July 12, 2023

|

- C-OG9.5a/C-CO9.5a: Clarification of the requested content for column 2. This column requests CAPEX in the reporting year for the expansion activity as a percentage of an organization’s total CAPEX in the reporting year, not as a percentage of total CAPEX for power generation alone.

|

| 1.7

|

Revised: July 25, 2023

|

- C3.5b: The requested content has been updated for columns 26, 28 and 30 as it is not possible to upload attachments for these columns. Supporting documents may be uploaded in question C-FI if needed.

- C3.5c: The requested content has been updated as it is not possible to upload attachments for this question. Companies may upload attachments in C10.2a that relate to the verification/assurance of information provided in C3.5a and/or C3.5b. Other supporting documents may be uploaded in question C-FI if needed.

|

| 1.8 |

Revised: August 4, 2023 |

- C4.1a, C4.1b, C-FS4.1d, C4.2a,C4.2b: Updates to Chinese translations of column headings to fix errors and improve clarity.

|

Note that you have selected to view the Climate Change - Full version.

You have selected to view sector-specific content for the following sectors:

CDP disclosure cycle 2023

Accessing questionnaire previews, reporting guidance, and scoring methodologies

CDP’s corporate questionnaire previews, reporting guidance, and scoring methodologies for climate change, forests and water security can be accessed from the guidance for companies page of CDP's website.

Submitting a response to the questionnaire(s)

Responses to questionnaires must be submitted via CDP's Online Response System (ORS), which is part of CDP's online disclosure platform. Please refer to Using CDP's Online Disclosure Platform for more details. Please note that while the questions themselves are the same in the questionnaire preview as they are in the ORS, the display format of some questions may differ, particularly for drop-down options and tables.

Sector-specific questions

Companies in high-impact sectors, in addition to the general questions, will be presented with questions specific to that sector. The rationale for developing a refined questionnaire for each of these sectors is outlined in the relevant sector introduction.

The sector-specific questions allocated to companies are defined by CDP's Activity Classification System (CDP-ACS). This system categorizes companies by focusing on the activities from which they derive revenue and associating these with the impacts to their business from climate change, water security and deforestation.

Please note that since each questionnaire includes sector-specific questions throughout, as not all questions will be applicable to your organization, some question numbers may skip.

Full and Minimum versions of the questionnaire

All organizations completing the climate change, forests and water security questionnaires are eligible to complete the full questionnaire.

In some cases, organizations may be eligible to complete a minimum version which contains fewer questions, and no sector-specific questions or data points.

Organizations are eligible to complete the minimum version of a questionnaire if they have an annual revenue of less than EUR/US$250 million*, and are disclosing in response to a request from a customer (i.e. CDP supply chain members), the CDP banks program members, the RE100 initiative, or the NZAM initiative.

Organizations will not be eligible to complete the minimum version questionnaire if they are disclosing in response to an investor request.

For information on scoring eligibility and implications, please see our Scoring Introduction.

* CDP reserves the right to remove the option of completing a minimum version questionnaire for previous responders to a questionnaire with an annual revenue of less than EUR/US$250 million, on the basis of the organization’s potential or existing environmental impact.

Timeline:

For the latest information on the timeline, please refer to our website.

Jan 2023

|

- Preview of 2023 questionnaires and reporting guidance released on CDP website (English versions).

|

| March 2023

|

- Preview of 2023 questionnaires and reporting guidance released on CDP website (translated versions).

|

| April 2023

|

- Online Response System (ORS) opens.

|

| July 2023

|

- Companies must submit their responses to investors and/or customers using the ORS to be eligible for scoring and inclusion in reports (where applicable).

|

For any disclosure-related enquiries, please contact the CDP Help Centre or your regional CDP contact.

CDP climate change questionnaire

This questionnaire is the property of CDP Worldwide, reproduction of all or part (including within software platforms) without permission of CDP Worldwide is prohibited. Please contact [email protected] for more information on this.

Introduction to CDP's climate change program and questionnaire

Improving corporate awareness through measurement and disclosure is essential to the effective management of climate change risk. CDP’s climate change questionnaire collects climate-related data from the world’s largest companies on behalf of over 680 institutional investor signatories with a combined US$130 trillion in assets and 280+ major purchasers with over US$6.4 trillion in procurement spend. Since its launch in 2002, the questionnaire has helped thousands of companies to measure their impacts, set ambitious targets and demonstrate progress for key stakeholders.

The questionnaire has been evolving over time in line with the latest climate science and global policy development. The 2015 Paris Agreement was a tipping point in the global approach to climate change. By agreeing to limit global temperature rises to well below 2°C and pursue efforts to limit warming to under 1.5°C, governments have committed to a transition to a net-zero carbon economy. This transition will create winners and losers within and across business sectors, as the manifestation of climate-related opportunities and risks accelerates in both size and scope. Business as usual will not be a good indicator of how companies will perform.

Regulators have begun to respond to the climate risks, notably with the recommendations by the Task Force on Climate-related Financial Disclosures (TCFD). Established by the Financial Stability Board, the TCFD has moved the climate disclosure agenda forward by emphasizing the link between climate-related risk and financial stability. The Task Force has recommended that both companies and investors disclose climate change information. This includes whether they are conducting scenario analysis in line with a 1.5°C pathway and then setting out how climate-related issues impact their strategy and financial planning. This amplifies the longstanding call from CDP’s investor signatories for companies to disclose comprehensive, comparable environmental data in their mainstream reports, driving climate-related risk management further into the boardroom. CDP’s climate change questionnaire has been aligned with the TCFD recommendations since 2018 and prompts companies to disclose data on how climate-related issues are addressed in their governance, strategy, risk management, and metrics and targets.

In its first two decades, CDP’s climate change questionnaire focused on raising ambition around climate and providing data to improve governance and decision-making. But time is fast running out to prevent catastrophic climate change, and an irreversible loss of nature and habitats. There is now an urgent need to ensure that stated intentions are accompanied by concrete plans, with transition metrics, and evidence of progress against agreed goals. Accountability is needed to raise the bar to align with halving emissions, shifting towards nature positivity by 2030 and achieving net-zero emissions and full nature recovery by 2050. In line with CDP’s 2021-2025 strategy, the climate change questionnaire and scoring will be evolving to further encourage and support companies to set targets and create tangible climate transition plans, as well as to measure their performance against them.

Carbon emissions are only one part of the challenge. The climate and nature crises need to be addressed simultaneously, including by conserving, protecting, and restoring ecosystems, adopting more sustainable agriculture and forestry practices, and ensuring a circular economy. In line with the 2021-2025 strategy, CDP begins broadening the environmental issues covered in its questionnaires, starting with the inclusion of questions on companies’ approach to maintaining and addressing biodiversity. As a first step in 2022, broad questions around governance, commitments, monitoring and reporting on biodiversity issues were included in a new module in the climate change questionnaire. These questions are material to all sectors and geographies and responses will inform future biodiversity metrics, ensuring the relevance and usefulness of biodiversity corporate reporting to both financial institutions and policy makers. The new biodiversity questions were developed in alignment with the IUCN’s Corporate Reporting on Biodiversity Guidelines.

Climate change questionnaire structure

There are 15 modules in the general climate change questionnaire, including the Introduction and Signoff modules, plus a module presented only to organizations that are responding to a customer request from one or more CDP Supply Chain Members. The journey through CDP’s general climate change questionnaire includes the following:

- Governance

- Risks and opportunities

- Business strategy

- Targets and performance

- Emissions methodology

- Emissions data

- Energy

- Additional metrics

- Verification

- Carbon pricing

- Engagement

- Biodiversity

Sector approach

The structure of the CDP climate change questionnaire was redesigned in 2018 in response to market needs and trends in corporate climate change reporting. Revisions included the inclusion of the TCFD recommendations, an increased emphasis on forward-looking metrics, improved alignment with other reporting frameworks, and the integration of sector-specific questions.

For climate change, CDP has incorporated sector-specific questions for 16 high-impact sectors.

All question numbers in the general climate change questionnaire begin with the letter C. Introduced in 2022, question numbers in the new forests and water module for financial services organizations only, begin with the letters FW. Questions that are unique to companies in a particular sector are labelled using a two-letter abbreviation within the question number. These abbreviations are noted below.

2023 climate change sectors:

- Agriculture: Agriculture commodities (AC); Food, beverage & tobacco (FB); Paper & forestry (PF)

- Energy: Coal (CO); Electric utilities (EU); Oil & gas (OG)

- Financial: Financial services (FS)

- Materials: Cement (CE); Capital goods (CG); Chemicals (CH); Construction (CN); Metals & mining (MM); Real estate (RE); Steel (ST)

- Transport: Transport services (TS); Transport OEMs (TO)

Climate change questionnaire changes in 2023

In 2023, CDP has revised questions and introduced new questions on

topics which reflect the strategic priorities for CDP and its

stakeholders. However, 79% of the 2022 questions remain

unchanged. A detailed document on climate change question changes from 2022 to 2023 can be found on the

Guidance page of the website.

Key changes include:

Core and supply chain questions

- One removed question for all companies

- Seven new questions for all companies

- Twenty-five modified questions for all companies, including one modified supply chain question

RE100 companies

- Three modified questions on renewable energy sourcing

Financial services sector

- One sector-specific question removed for the financial services sector

- Four new questions for the financial services sector

- Fourteen modified questions for financial services sector organizations across the questionnaire

Other sector-specific changes

- One removed sector-specific question for the Agricultural commodities; Food, beverage and tobacco; and Paper and forestry sectors

- One new sector-specific question for the Oil & gas and Coal sectors

- Fourteen modified sector-specific questions for Agricultural commodities; Food, beverage and tobacco; Paper and forestry; Oil & gas; Cement; Electric utilities; Capital goods; Chemicals; Construction; Metals & mining; Real estate; Steel; Transport services; and Transport OEMs sectors

Revisions and changes are indicated for every question as: “no change”, “minor change”, “modified question”, “new question”, “modified guidance”, “additional guidance” or "revised question dependency". “Minor change” indicates wording edits and revisions to drop-down options or a simple clarification, while a “modified question” indicates that the data requested has been revised.

Preparing your CDP response

Please find below information on the support materials and options available to companies, and important notes for completing your disclosure. Please review these notes carefully as you prepare your response, even if you have responded to the questionnaire in previous years.

CDP disclosure support materials

CDP provides a variety of support materials to help organizations disclosing to our questionnaires. Before completing the corporate questionnaires, we strongly recommend you read this Reporting Guidance, the Scoring introduction, and relevant Scoring Methodology. Please also refer to the CDP Technical Notes and other guidance materials accessible from the guidance tool after signing in to the website, and see the Frequently Asked Questions on the website.

Reporting guidance

The reporting guidance in this document includes the following:

- Module-level guidance: for select modules, this guidance provides an overview of key changes, sector-specific content for the module, and important disclosure notes. This section also presents question pathway diagrams showing the flow of questions through each module.

- Question-level guidance: at the question level, guidance is separated into the following components to provide clarity around questions, terminology and requirements:

- Rationale: provides reasoning behind the inclusion of each question;

- Connections to other frameworks: notes for each relevant question in the climate change questionnaire, connections to the Sustainable Development Goals (SDGs), S&P Global Corporate Sustainability Assessment (S&P CSA), the Task Force on Climate-related Financial Disclosures (TCFD), RE100, and for financial services institutions only, the Net Zero Asset Managers (NZAM) initiative and CEO Water Mandate;

- Requested content: offers context around each question and requested criteria;

- Explanation of terms: provides detailed definitions for specific terminology;

- Example responses: for select questions, this provides an example of a response that would include all information requested; and

- Additional information: for select questions, this provides optional contextual information and sources related to the subject of the disclosure request.

- Glossary: viewable at the end of the reporting guidance, the glossary contains a subset of 'Explanation of terms'.

- Appendix: Agricultural/Forestry management practices.

If you have any questions that are not answered in the reporting guidance, the additional guidance noted below, or our Frequently Asked Questions, please contact your local CDP contact or visit the CDP Help Centre.

Webinars and workshops

CDP hosts live webinars and workshops designed to aid you with environmental reporting.

Please visit the workshops and webinars and climate change pages of CDP's website for more details.

CDP Reporter Services

CDP Reporter Services program offers tailored support, enhanced data access and thought leadership on managing and reporting environmental risk to your business. Access the tools you need to move from disclosure to leadership on integrating climate, forests management, and water security into your wider business strategy. For year-round, personalized disclosure support from a dedicated CDP account manager, a gap analysis of your previous response, final review before submission and analytics tools to benchmark yourself against peers and understand best practice contact [email protected]. Visit the Reporter Services page of CDP's website for more information.

CDP's Accredited Solutions Providers

CDP partners with leading environmental service providers that can support companies throughout all stages of the measurement, reporting and management of their climate and sustainability data and impacts. All CDP solutions providers have met specific accreditation criteria. See provider areas of expertise below, and visit the accredited solutions provider directory to search for the provider best able to support you:

- Carbon reduction solutions providers offer technology and services that can help your organization reduce carbon emissions and improve energy efficiency.

- Climate change consultancy solutions providers have a wide range of technical expertise to support companies with establishing and implementing climate change and sustainability strategies.

- Science-based target (SBT) solutions providers have expertise in helping companies to set and implement targets in line with what the latest climate science says is necessary.

- Education & training solutions providers improve employee awareness and understanding of how climate change affects their organization through carbon management training programs.

- Renewable energy solutions providers provide expertise in procuring, tracking, and generating renewable power.

- Software solutions providers simplify the collection, monitoring, and reporting of sustainability, CSR, and environmental data through integrated sustainability software applications.

- Verification solutions providers help organizations disclose accurate data and improve internal processes by providing third-party verification and assurance of emissions data, a practice recommended by CDP.

As well as visiting our accredited solutions provider webpage, you can also contact [email protected] to find out more.

Important notes for completing your disclosure

Acronyms

Avoid using bespoke internal acronyms unless required for your organization’s response, in which case please provide their meaning to enable correct analysis and scoring.

Blank responses

Leaving a response blank is interpreted as non-disclosure. For numeric fields, values of zero (0) imply a measurement has been made, and the value is zero (0). For numeric fields where no measurement has been made, please leave the field blank and provide an explanation in an open text field for that same question (e.g. 'Comment' (optional) or 'Please explain' (scored)). If there is no open text field for the question, you may provide an explanation in the Further information field in the ORS at the end of your disclosure. Leaving a response blank and entering a value of zero (0) have different scoring implications. Please see the scoring methodology for more details.

Character limits

The character limits noted in the reporting guidance and in the ORS include spaces.

'Comment' columns

Some questions include a column labelled as 'Comment'. Note that providing information in these columns is optional.

Company-specific information

Some questions request company-specific information, rationales, case studies and/or examples. This level of detail gives data users confidence that the issue at hand has been thoroughly considered in the context of the responding organization's own business and not simply assessed in general terms.

- Be sure to include company-specific detail, such as references to activities, programs, products, services, methodologies, or operating locations unique to your company’s business or operations. A company-specific explanation should include details that make the answer true for the responding company and are distinct from other companies in the same industry and/or geography.

- Clear rationales are those which provide logical reasoning for methodologies, descriptions, decision, and actions.

- Case studies are defined as a detailed description of the implementation of a process, strategy or decision to a specific situation and/or task. When formulating case studies, responders may find it helpful to consider a “Situation-Task-Action-Result” (STAR) approach :1) Situation: what was the context or background? 2) Task: what needed to be done or what was the problem to be solved? 3) Action: what was the course of action taken? 4) Result: what was the final outcome of the course of action?

- An example does not need to follow the STAR approach. It can be shorter than a case study but should include some company-specific detail.

For more details, refer to the Scoring Introduction on the CDP website.

Consistency

CDP encourages a comprehensive and consistent response. Please ensure there is no conflicting information in your responses, both within a question and across the questionnaire.

Copy forward

The 'copy forward' functionality will be available in the ORS for companies that disclosed to CDP in previous reporting years. This functionality auto-populates your most recent answers into your questionnaire where applicable.

Note that this functionality may have been disabled for modified data points. The reporting guidance will indicate which questions have been modified. The Questionnaire Changes document on the guidance section of the CDP website lists all revisions from the previous year.

Please review the auto-populated answers carefully. It is your responsibility to ensure your answers are updated for the accuracy and completeness of your response.

Data accuracy

CDP recognizes that there may be uncertainty linked to data – this can arise from data gaps, assumptions, metering/measurement constraints including equipment accuracy etc. CDP allows estimated data to be submitted. However, an emphasis is placed on reporting transparently and this means that a company should always provide an explanation when its reported data is not accurate and detail the uncertainty (use the 'Please explain' or 'Comment' columns provided in the question).

Drop-down options ('Other, please specify')

Please select from the options provided whenever possible, and only select 'Other, please specify' when none of the listed options is appropriate. This greatly assists data analysis. If selecting 'Other, please specify', you must add a label that describes the option you are providing data for.

'Further information' field

At the end of the questionnaire, there is an opportunity to provide additional information or context that you feel is relevant to your organization’s response. This field is optional and not scored.

Mergers and acquisitions (M&As)

All disclosure should be defined by the organizational boundary applicable at the time of the stated reporting period. (Note that for CDP disclosure, organizations are encouraged to align their reporting period and organizational boundaries with their financial reporting).

Regarding forward-looking disclosure, organizations should include information that was correct at the time of the stated reporting period (for example, for data points referring to the future or "the next two years"). Organizations undergoing (or that have undergone) M&As need to consider the timing of the M&As and reporting period as follows:

- Organizations that were acquired after the end of the current reporting period: these should respond with what was planned (strategy, targets, etc.) before being acquired (i.e., during the reporting period). For transparency, where possible they may state where they consider that the forward-looking information may be subject to change due to the very recent acquisition.

- Organizations that were acquired during the reporting period: these should provide information that was applicable and correct to the best of their knowledge at the end of the reporting period. At the time of submitting their response to CDP, this information may not be the most up to date due to changes underway following the acquisition. For transparency, the company may state this in their disclosure where possible.

Personal data

It is important that you do not include the name of any individual or any other personal data in your response. For questions that ask for the positions of staff, out of respect for personal data privacy we are asking only for the position and not for the individual’s name or any other information relating to them.

Providing feedback to CDP

You can provide feedback to CDP on the content of our questionnaires and supporting documents through our online general feedback form.

We are unable to respond individually to all feedback, but please be assured that all form submissions are reviewed and contribute towards our continuous improvement.

However, if you represent a responding organization and would like to request a response, please get in touch with your local CDP contact.

Sector introduction: Agricultural commodities (AC)

Activities in the agricultural commodities sector include producing, processing and distributing raw materials (crops and/or livestock) that will be used as ingredients in the manufacturing and packaging of consumer goods by the food, beverage and tobacco sector. This includes the small-scale production of non-timber forest products (e.g. rubber, nuts, seeds, etc.). The agricultural commodities sector is fundamentally dependent on natural resources, and thus directly affected by climate change. Climate-related risks associated with the sector include physical risks such as changing weather patterns, and regulatory risks relating to farm management practices (e.g. the use of fertilizers and pesticides, land use, livestock management etc.). Emissions are associated with the entire agricultural commodities value chain, therefore a whole value chain approach is advised; including consideration of emissions resulting from the consumption of products.

CDP’s agricultural commodities questions focus on the following topics:

- Land management practices with climate change mitigation/adaptation benefits;

- Biogenic carbon pertaining to direct operations;

- Commodity-specific emissions intensity data related to the activities performed by your organisation; and

- Scope 1 and Scope 3 emissions breakdowns by relevant business activity.

This CDP sector aligns with the TCFD’s Agriculture, Food, and Forest Products group, along with the food, beverage and tobacco (FB), and paper & forestry sectors (PF).

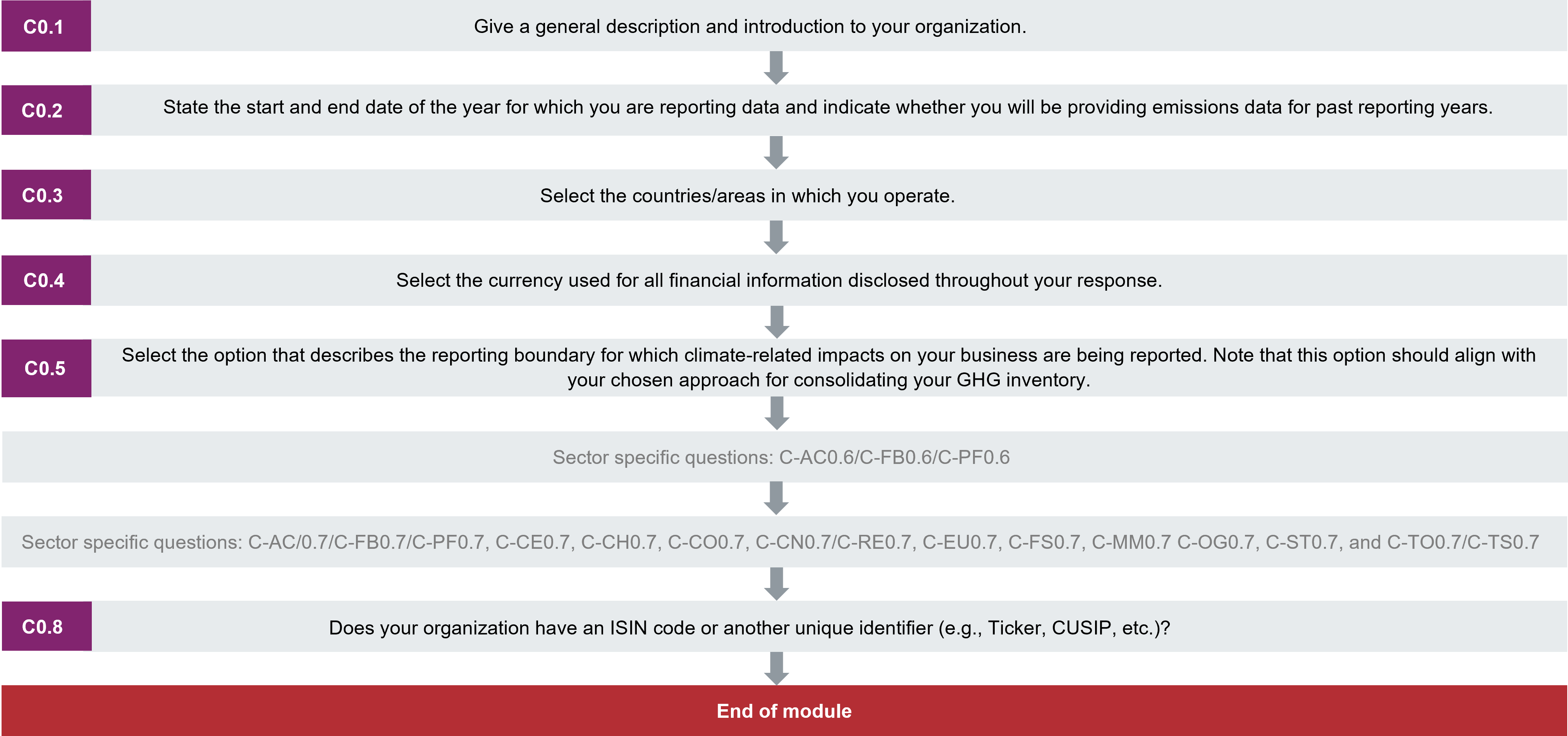

C0 Introduction

Module Overview

This module requests information about your organization’s disclosure to CDP and will help data users to interpret your responses in the context of your business operations, timeframe and reporting boundary.

The information provided here should apply consistently to your responses throughout the questionnaire and be complete and accurate as it may determine response options presented in subsequent modules.

For this reason, you should respond to every question in this module before accessing the rest of the questionnaire.

Key changes

- Modified questions:

- C0.2 – columns added to allow companies to restate a different number of years of data for each scope.

Click here for a list of all changes made this year.

Sector-specific content

Additional questions on organizational activities for the following high-impact sectors:

- Agricultural commodities

- Capital goods

- Cement

- Chemicals

- Coal

- Construction

- Electric utilities

- Financial services

- Food, beverage and tobacco

- Metals & mining

- Oil & gas

- Paper & forestry

- Real estate

- Steel

- Transport original equipment manufacturers (OEMs)

- Transport services

Pathway diagram - questions

This diagram shows the general questions contained in module C0. To access question-level guidance, use the menu on the left to navigate to the question.

Introduction

(C0.1) Give a general description and introduction to your organization.

Change from last year

No change

Rationale

This will help data users interpret your responses.

Response options

This is an open text question with a limit of 5,000 characters.

Please note that when copying from another document into the ORS, formatting is not retained.

Requested content

General

- Provide information about your operations to help data users understand your greenhouse gas (GHG) emissions inventory and corporate climate change strategy. Include information on your business divisions and your emissions-generating activities (e.g. extraction and/or processing/refining of natural resources, electricity generation, transportation, manufacturing etc.).

-

This information helps data users understand your company’s emissions profile and differences in emissions figures between peer companies.

- You may also provide any other information which is relevant to your disclosure.

Explanation of terms

- Organization: Throughout this questionnaire, “your organization” refers collectively to all the companies, businesses, other entities or groups that fall within the definition of your reporting boundary (provided in C0.5). This term is used interchangeably with “your company”, but CDP recognizes that some disclosing organizations may not consider themselves to be, or be formally classified, as “companies”.

(C0.2) State the start and end date of the year for which you are reporting data and indicate whether you will be providing emissions data for past reporting years.

Change from last year

Modified question

Rationale

This will help data users interpret your responses.

Ambition: Companies disclose historic data that enables progress over time to be tracked.

Connection to other frameworks

RE100

Response options

Please complete the following table. *Column/row appearance is dependent on selections in this or other questions.

| Start date

|

End date

|

Indicate if you are providing emissions data for past reporting years

|

Select the number of past reporting years you will be providing Scope 1 emissions data for*

|

Select the number of past reporting years you will be providing Scope 2 emissions data for*

|

Select the number of past reporting years you will be providing Scope 3 emissions data for*

|

|

From: [DD/MM/YYYY]

|

To: [DD/MM/YYYY]

|

Select from:

|

Select from:

- 1 year

- 2 years

- 3 years

- 4 years

- 5 years

- Not providing past emissions data for Scope 1

|

Select from:

- 1 year

- 2 years

- 3 years

- 4 years

- 5 years

- Not providing past emissions data for Scope 2

|

Select from:

- 1 year

- 2 years

- 3 years

- 4 years

- 5 years

- Not providing past emissions data for Scope 3

|

Requested content

General

- Apply this reporting year to your answers for the entire questionnaire unless the ability is provided to specify other reporting periods.

- Please ensure that the reporting period represents only one full year that has already passed. Reporting periods should not be in the future. This information is important for others to understand the time dimension of your disclosure.

- If you are using the Export/Import functionality, please check that the imported date is correct.

- The current reporting year is the most recent 12-month period for which data is reported.

- This reporting period applies to all answers except where other reporting periods can be disclosed. CDP does not require companies to align their reporting year with their fiscal year. However, when organizations report emissions intensity using a financial metric, both emissions and financial information provided should align with the reporting year reported here.

- Note that the investment community generally prefers a company's disclosure period to match the fiscal year for their financial jurisdiction. This facilitates the assessment of environmental performance data in alignment with financial performance data.

- CDP recommends that companies provide a year for which they have complete data if possible. However, if you do not have data for the entirety of your reporting year, you have the following options:

- Extrapolate your data to cover the entire reporting year.

- Outline in C6.4 the sources of Scope 1 and 2 emissions within your selected reporting boundary and not included in your disclosure.

- Select "No" in column 3 (Indicate if you are providing data for past reporting years) unless you are a first time responder providing emissions from past years or a previous responder to CDP who is restating your emissions data. For more information on this see the note for first-time responders and the note for restating data below.

- If multiple years of data are provided, only data pertaining to the most recent reporting year will be scored.

Note for first-time responders:

- If you have not provided emissions data before, supply gross global emissions data for the five years prior to the current reporting year in the emissions accounting questions (C6.1 and C6.3) for Scopes 1 and 2, and in C6.5a for Scope 3.

- To report emissions data for years prior to the current reporting year, select "Yes" in column 3 ("Indicate if you are providing emissions data for past reporting years"). Then select how many years of emissions data you will be providing for each Scope in columns 4-6. You should aim to provide the same number of past years of emissions data for all Scopes.

- This will enable you to enter the corresponding number of past years of data when you reach questions C6.1, C6.3, and C6.5a.

Note for restating data:

- You may also choose to restate your emissions data previously supplied to CDP, for example to ensure that your historical data reflects your current organizational boundary.

- Reporting recalculated figures for these years is optional. However, if you wish to do this it can provide transparency to stakeholders using your data.

- If you choose to restate data previously supplied to CDP, report the dates of those reporting periods here by selecting "Yes" in column 3 ("Indicate if you are providing emissions data for past reporting years"). Then select how many years of emissions data you will be providing for each Scope in columns 4-6.

- This will enable you to enter the corresponding number of past years of data when you reach questions C6.1, C6.3, and C6.5a.

- For more information on restatements see CDP's technical note on restatements here.

Note for financial services companies:

- The number of past years data for Scope 3 will also determine the number of past years data for portfolio emission data in question C-FS14.1c.

(C0.3) Select the countries/areas in which you operate.

Change from last year

No change

Rationale

This will help data users interpret your responses.

Connection to other frameworks

RE100

Response options

Please complete the following table:

| Country/area

|

|

Select all that apply:

[Country/area drop-down list]

|

Requested content

General

- Select all countries/areas in which you operate from the drop-down menu provided.

(C0.4) Select the currency used for all financial information disclosed throughout your response.

Change from last year

No change

Rationale

CDP encourages companies to report financial figures associated with their impacts, risks, and opportunities. Establishing a single currency will facilitate the collection of comparable financial information. This will benefit investors and other data users when assessing the costs and benefits reported by your organization.

Response options

Please complete the following table:

| Currency

|

|

Select from:

[Currency drop-down list]

|

Requested content

General

- Select the currency to be applied to all financial information reported in this disclosure.

- For example, if you select USD($), provide metric tons CO2e per USD($) as the financial intensity metric in question C6.10.

(C0.5) Select the option that describes the reporting

boundary for which climate-related impacts on your business are being reported. Note that this option should align with your chosen approach for consolidating your GHG inventory.

Change from last year

No change

Rationale

This will help data users interpret your responses.

Connection to other frameworks

RE100

Response options

Select one of the following options:

- Financial control

- Operational control

- Equity share

- Other, please specify

Requested content

General

- Use a consolidated approach when determining reporting boundaries. CDP recommends that you consult your legal or accounting advisors when doing so.

- The “consolidated approach” identifies which entities are included within the reporting boundary. Unless stated otherwise, the information you provide in response to the CDP climate change questionnaire should be presented as one “consolidated” result covering all of the companies, entities, businesses, etc., within your reporting boundary.

- To support the use, tracking, and comparability of reported GHG information, respondents are encouraged to adopt the consolidation approaches based on the GHG Protocol Corporate Standard, outlined in more detail in Chapter 3 of the Standard.

- If you have previously disclosed emissions data to CDP and your consolidation approach has changed in the current reporting year, select your new approach here and provide details of the change in C5.1b.

Further clarification of options

- The options in the drop-down for this question are based on the GHG Protocol Corporate Standard, and are described in more detail below (text adapted from the GHG Protocol Corporate Standard:

- Financial control: An organization has financial control over an operation if it has the ability to direct the financial and operating policies of the operation with a view to gaining economic benefits from its activities. Generally, an organization has financial control over an operation for GHG accounting purposes if the operation is treated as a group company or subsidiary for the purposes of financial consolidation.

- Companies using the CDSB framework should select this option.

- Operational control: An organization has operational control over an operation if it or one of its subsidiaries has the full authority to introduce and implement its operating policies at the operation.

- Most SMEs select this option.

- Equity share: Under the equity share approach, a company accounts for GHG emissions from operations according to its share of equity in the operation. The equity share reflects the economic interest, which is the extent of rights a company has to the risks and rewards flowing from an operation. Typically, the share of economic risks and rewards in an operation is aligned with the company’s percentage ownership of that operation, and equity share will normally be the same as the ownership percentage. Where this is not the case, the economic substance of the relationship the company has with the operation always overrides the legal ownership form to ensure the equity share reflects the percentage of economic interest. The principle of economic substance taking precedence over legal form is consistent with international financial reporting standards.

Explanation of terms

- Company: Throughout this questionnaire, “your company” refers collectively to all the companies, businesses, organizations, other entities or groups that fall within your definition of the reporting boundary. This term is used interchangeably with “your organization”, but CDP recognizes that some disclosing organizations may not consider themselves to be, or be formally classified, as “companies”.

- Consolidation approach: The identification of companies, businesses, organizations etc. for inclusion within the reporting boundary of the responding organization. The way in which you report information for the companies that are included within the reporting boundary is known as the “consolidation approach” because, unless stated otherwise, the information you provide in response to the questionnaire should be presented as one “consolidated” result covering all of the companies, entities, businesses etc within your reporting boundary. The GHG Protocol states that two distinct approaches may be used to consolidate GHG emissions; the equity share and the control approaches. Control can be defined in either financial (financial control) or operational (operational control) terms. This term is used interchangeably with “your organization”, but CDP recognizes that some disclosing organizations may not consider themselves to be, or be formally classified, as “companies”.

- GHG inventory: a quantified list of an organization’s greenhouse gas emissions and sources.

- Organization: Throughout this questionnaire, “your organization” refers collectively to all the companies, businesses, other entities or groups that fall within the definition of your reporting boundary (provided in C0.5). This term is used interchangeably with “your company”, but CDP recognizes that some disclosing organizations may not consider themselves to be, or be formally classified, as “companies”.

- Reporting boundary: This determines which organizational entities, such as groups, businesses and companies, are included in or excluded from your disclosure. These may be included according to your financial control, operational control, equity share or another measure. Please consistently apply this organizational boundary when responding to questions unless you are specifically asked for data about another category of activities.

Business activities emissions relevancy

(C-AC0.6/C-FB0.6/C-PF0.6) Are emissions from agricultural/forestry, processing/manufacturing, distribution activities or emissions from the consumption of

your products – whether in your direct operations or in other parts of your value chain – relevant to your current

CDP climate change disclosure?

Question dependencies

Your response to this question determines which questions will be shown throughout this questionnaire and which response options will be listed within these questions.

Change from last year

No change

Rationale

This question determines which agricultural business activities your organization performs and/or engages in that are relevant for this disclosure. This will provide context on your agricultural activities to investors and other data users as well as help your organization set reporting boundaries.

Response options

Please complete the following table:

| Business activity

|

Relevance

|

|

Agriculture/Forestry

|

Select from:

- Own land only

- Elsewhere in the value chain only

- Both own land and elsewhere in the value chain

- No

|

|

Processing/Manufacturing

|

Select from:

- Direct operations only

- Elsewhere in the value chain only

- Both direct operations and elsewhere in the value chain

- No

|

|

Distribution

|

Select from:

- Direct operations only

- Elsewhere in the value chain only

- Both direct operations and elsewhere in the value chain

- No

|

|

Consumption

|

Select from:

|

Requested content

General

- According to the GHG Protocol Corporate Accounting and Reporting Standards, the activity is relevant if it yields pertinent information to decision-making (for both internal and external users) regarding climate related issues.

- Note you should consider aspects associated with the listed business activities that are relevant to the agricultural sectors. For example, processing/manufacturing may refer to the processing of soft commodities or the manufacture of food, beverage, tobacco and/or wood-based goods.

Business activity (column 1)

- Provide an answer to each of the following activities listed regarding your business activities and considering your whole value chain.

- Consider the following regarding each activity:

- The sources of Agricultural/Forestry emissions predominantly comprise:

- Carbon dioxide from the decay or burning of biological or soil organic matter, fuel combustion and electricity generation in farm operations;

- Methane from the decomposition of organic materials in oxygen-deprived conditions, notably from the digestion of livestock, from stored manures, and from rice growing;

- Nitrous oxide from transformation of nitrogen in soils and manures (including fertilizer application and indirect emissions from fertilizer production in your supply chain).

- All these sources of emissions can be classified as either mechanical or non-mechanical emissions (See the GHG Protocol Agricultural Guidance for further details)

- Emissions from the processing of raw materials and wood, or the manufacture of food, beverage and tobacco products are associated with all processes adopted, and all methods and techniques used, to transform raw agricultural inputs/timber products into final products ready for human consumption, including:

- Pre-processing (relevant if companies use processed inputs, e.g. sugar)

- Primary grading/ screening to ensure uniformity

- Storage during different processing stages

- Cleaning to remove and separate off-specification material, organic and non-organic debris, metals, and pesticide residues among other contaminants

- Cutting, trimming, rolling and peeling to re-shape and remove inedible parts

- Cooking, canning, evaporating, drying and freezing

- Pulping and filtration

- Packaging of the final product to provide containment, protection, communication, and convenience

- Packaging for transport in, e.g. crates or pallets

- Waste generated during processing activities

- Distribution encompasses the entire network required to move products through the value chain from the farm/production unit to the retail location. You should consider all the stages of distribution in your disclosure, i.e.:

- Transportation of raw agricultural/forest products to processing facilities;

- Transportation of material inputs to processing facilities, for example, packaging materials, chemicals, wood and any other ingredients;

- Product distribution from processing facilities to the retailer/customer;

- Transportation of waste to disposal sites or to points of re-use;

- In each of the cases listed for transportation above, you should also account for emissions from: empty return journeys; the storage of goods during distribution, (as this can often require specific controls for humidity, temperature, atmospheric conditions and hygiene requirements); and the waste generated during transportation

- The consumption stage includes the use of goods in addition to waste disposal and end of life treatment of products sold by the reporting organization. You should consider:

- Emissions from the cooling, freezing and heating of sold products;

- Waste disposal and end of life treatment of products, i.e., emissions associated with land filling, incineration, composting, recycling and wastewater treatment.

- Note that the calculation of emissions associated with consumption and end life treatment may require reporting companies to make assumptions regarding how consumers use products; product lifetimes; and end of life treatment methods chosen by consumers.

Relevance (column 2)

- If an activity performed by/associated with your organization is relevant, specify which parts of your value chain this activity applies. For example, if all agricultural activities take place within your organizational boundary i.e. your organization grows all of its agricultural products on self-owned/managed farms, select “Own land only” for row Agriculture/Forestry. If you purchase all your agricultural inputs from agricultural suppliers, select “Elsewhere in value chain only.” If your organization grows some of its agricultural inputs and buys some from agricultural suppliers, select “Both own land and elsewhere in value chain.”

- Note that if you would like to add or delete a certain activity later in the questionnaire, return to this question and edit your response accordingly. If you decide to delete an activity by selecting "No" in this column, your previous responses to linked questions will be erased. For example, if you indicate that "Processing/Manufacturing" is not relevant anymore, the row associated with this activity will be erased in C-AC6.8a/C-FB6.8a/C-PF6.8a.

Explanation of terms

- Agriculture/Forestry: Agriculture is the cultivation and breeding of animals, plants, and fungi for food, fiber, biofuels, drugs or other purposes. While forestry is the creation and management of forests, including wood harvesting. These activities have a direct impact on land and thus are closely associated with deforestation and greenhouse gas emissions from land use.

- Consumption: Consumption includes the use of goods, waste disposal and end of life treatment of products sold by the reporting organization.

- Distribution (agriculture/forestry): Distribution encompasses the entire network required to move products through the value chain from the farm/forest to the retail location. The total travel distance and the mode of transport will impact the amount of emissions produced: air transport has by far the highest GHG emissions, followed by road, then ocean freight and rail (Source: Institute for Agriculture and Trade Policy, 2009).

- Processing/Manufacturing (agriculture/forestry): Includes all processes adopted, and all methods and techniques used, to transform raw agricultural or wood products inputs into final goods ready for human consumption. Direct and indirect emissions from processing result from the operation of machinery and equipment, as well as from heating, cooling, and refrigeration.

- Value chain: The entire sequence of activities or partners that provide value to or receive value from an organization's products and services, either within, upstream or downstream of direct operations. For further details on reporting boundaries please consult the GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard.

(C-AC0.6a/C-FB0.6a/C-PF0.6a) Why are agricultural/forestry activities not relevant to your current

CDP climate change disclosure?

Question dependencies

This question only appears if you select "No" in response to the "Agriculture/Forestry" row in C-AC0.6/C-FB0.6/C-PF0.6.

Change from last year

No change

Rationale

This question provides further context to data users about why you have indicated that agricultural/forestry activities are not relevant to this disclosure and whether you have fully assessed the potential climate-related risks and impacts to your business related to these activities.

Response options

Please complete the following table:

| Primary reason

|

Please explain

|

|

Select from:

- Outside the value chain of my organization

- Analysis in progress

- Evaluated but judged to be unimportant

- Not evaluated due to insufficient data on operations

- Not evaluated due to lack of internal resources

- No instruction from management

- Other, please specify

|

Text field [maximum 4,000 characters]

|

Requested content

Primary reason (column 1)

- Select the option that best describes the primary reason why you indicated that emissions from agricultural/forestry activities are not relevant.

- If none of the reasons apply to your organization, select "Other, please specify" and indicate the primary reason agricultural/forestry activities are not relevant for your organization. If you need more than 40 characters, please use column 2 "Please explain".

Please explain (column 2)

- If you selected "Outside the value chain of my organization" or "Evaluated but judged to be unimportant", describe your evaluation methods, indicating the procedures and tools used for evaluating the relevance of this activity. Specify parts of your business included in the analysis and the criteria used to decide that the activity was not relevant.

- If you selected the dropdown "Analysis in progress" in column 1, provide a date for when it will be finalized in this column.

- If you selected "Not evaluated due to lack of internal resources", specify the main challenges you experience to performing such analysis.

- If you selected "Not evaluated due to insufficient data on operations" or "Not evaluated due to lack of internal resources", indicate if you have any plans to evaluate the relevancy of this activity to your climate change disclosure in the next two years and if so, describe the methods and coverage for this upcoming analysis.

(C-AC0.6b/C-FB0.6b/C-PF0.6b) Why are emissions from agricultural/forestry activities undertaken on your own land not relevant to your current CDP climate change disclosure?

Question dependencies

This question only appears if you select "Elsewhere in the value chain only" in response to the "Agriculture/Forestry" row in C-AC0.6/C-FB0.6/C-PF0.6.

Change from last year

No change

Rationale

This information provides further context to data users as to why you have indicated agricultural/forestry activities pertaining to your own land are not relevant and whether you have fully assessed the potential climate-related risks and impacts to your business related to these activities.

Response options

Please complete the following table:

| Primary reason

|

Please explain

|

|

Select from:

- Do not own/manage land

- Analysis in progress

- Evaluated but judged to be unimportant

- Not evaluated due to insufficient data on operations

- Not evaluated due to lack of internal resources

- No instruction from management

- Other, please specify

|

Text field [maximum 4,000 characters]

|

Requested content

Primary reason (column 1)

- Select the option that best describes the primary reason for why you indicated that emissions from agricultural/forestry activities performed on owned/managed land are not relevant to this disclosure.

- If none of the reasons apply to your organization, select "Other, please specify" and indicate the primary reason agricultural/forestry activities performed on owned/managed land are not relevant for your organization. If you need more than 40 characters, please use column 2 "Please explain".

Please explain (column 2)

- If you selected "Do not own/manage land", "Analysis in progress" or "Evaluated but judged to be unimportant", describe your evaluation methods, indicating the procedures and tools used for evaluating the relevance of this activity. Specify parts of your business included in the analysis and the criteria used to decide that the activity was not relevant.

- If you selected the dropdown "Analysis in progress" in column 1, provide a date for when it will be finalized in this column.

- If you selected "Not evaluated due to lack of internal resources", specify the main challenges you experience to performing such analysis.

- If you selected "Not evaluated due to insufficient data on operations" or "Not evaluated due to lack of internal resources", indicate if you have any plans to evaluate the relevancy of this activity to your climate change disclosure in the next two years and if so, describe the methods and coverage for this upcoming analysis.

(C-AC0.6c/C-FB0.6c/C-PF0.6c) Why are processing/manufacturing activities not relevant to your current CDP climate change

disclosure?

Question dependencies

The question only appears if you select "No" in response to the "Processing/Manufacturing" row in C-AC0.6/C-FB0.6/C-PF0.6.

Change from last year

No change

Rationale

This question provides further context to data users as to why you have indicated that processing/manufacturing activities are not relevant and whether you have fully assessed the potential climate-related risks and impacts to your business related to these activities.

Response options

Please complete the following table:

| Primary reason

|

Please explain

|

|

Select from:

- Outside the value chain of my organization

- Analysis in progress

- Evaluated but judged to be unimportant

- Not evaluated due to insufficient data on operations

- Not evaluated due to lack of internal resources

- No instruction from management

- Other, please specify

|

Text field [maximum 4,000 characters]

|

Requested content

Primary reason (column 1)

- Select the option that best describes the primary reason why you indicated that emissions from processing/manufacturing activities are not relevant to this disclosure.

- If none of the reasons apply to your organization, select "Other, please specify" and indicate the primary reason processing/manufacturing activities performed are not relevant for your organization. If you need more than 40 characters, please use column 2 "Please explain".

Please explain (column 2)

- If you selected "Outside the value chain of my organization", "Analysis in progress" or "Evaluated but judged to be unimportant", describe your evaluation methods, indicating the procedures and tools used for evaluating the relevance of this activity. Specify parts of your business included in the analysis and the criteria used to decide that the activity was not relevant.

- If you selected the dropdown "Analysis in progress" in column 1, provide a date for when it will be finalized in this column.

- If you selected "Not evaluated due to lack of internal resources", specify the main challenges you experience to performing such analysis.

- If you selected "Not evaluated due to insufficient data on operations" or "Not evaluated due to lack of internal resources" indicate if you have any plans to evaluate the relevancy of this activity to your climate change disclosure in the next two years and if so, describe the methods and coverage for this upcoming analysis.

(C-AC0.6d/C-FB0.6d/C-PF0.6d) Why are emissions from processing/manufacturing activities

within your direct operations not relevant to your current CDP climate change

disclosure?

Question dependencies

This question only appears if you select "Elsewhere in the value chain only" in response to the "Processing/Manufacturing" row in C-AC0.6/C-FB0.6/C-PF0.6.

Change from last year

No change

Rationale

This information provides further context to data users about why you have indicated that processing/manufacturing activities, pertaining to your direct operations, are not relevant to this disclosure and whether you have fully assessed the potential climate-related risks and impacts to your business related to these activities.

Response options

Please complete the following table:

| Primary reason

|

Please explain

|

|

Select from:

- Outside the direct operations of my organization

- Analysis in progress

- Evaluated but judged to be unimportant

- Not evaluated due to insufficient data on operations

- Not evaluated due to lack of internal resources

- No instruction from management

- Other, please specify

|

Text field [maximum 4,000 characters]

|

Requested content

Primary reason (column 1)

- Select the option that best describes the primary reason for why you indicated that emissions from processing/manufacturing activities pertaining to your direct operations are not relevant to this disclosure.

- If none of the reasons are suitable, select “Other, please specify” and indicate the primary reason processing/manufacturing activities pertaining to your direct operations are not relevant for your organization. If you need more than 40 characters, please use column 2 “Please explain”.

Please explain (column 2)

- If you selected "Outside the direct operations of my organization", "Analysis in progress" or "Evaluated but judged to be unimportant", describe your evaluation methods, indicating the procedures and tools used for evaluating the relevance of this activity. Specify parts of your business included in the analysis and the criteria used to decide that the activity was not relevant.

- If you selected the dropdown "Analysis in progress" in column 1, provide a date for when it will be finalized in this column.

- If you selected "Not evaluated due to lack of internal resources", specify the main challenges you experience to performing such analysis.

- If you selected "Not evaluated due to insufficient data on operations" or "Not evaluated due to lack of internal resources" indicate if you have any plans to evaluate the relevancy of this activity to your climate change disclosure in the next two years and if so, describe the methods and coverage for this upcoming analysis.

(C-AC0.6e/C-FB0.6e/C-PF0.6e) Why are distribution activities not relevant

to your current CDP climate change disclosure?

Question dependencies

This question only appears if you select "No" in response to the "Distribution" row in C-AC0.6/C-FB0.6/C-PF0.6.

Change from last year

No change

Rationale

This information provides further context to data users about why you have indicated that distribution activities are not relevant to this disclosure and whether you have fully assessed the potential climate-related risks and impacts to your business related to these activities.

Response options

Please complete the following table:

| Primary reason

|

Please explain

|

|

Select from:

- Outside the value chain of my organization

- Analysis in progress

- Evaluated but judged to be unimportant

- Not evaluated due to insufficient data on operations

- Not evaluated due to lack of internal resources

- No instruction from management

- Other, please specify

|

Text field [maximum 4,000 characters]

|

Requested content

Primary reason (column 1)

- Select the option that best describes the primary reason for why you indicated that emissions from distribution activities are not relevant to this disclosure.

- If none of the reasons are suitable, select "Other, please specify" and indicate the primary reason distribution activities are not relevant for your organization. If you need more than 40 characters, please use column 2 "Please explain".

Please explain (column 2)

- If you selected "Outside the value chain of my organization", "Analysis in progress" or "Evaluated but judged to be unimportant", describe your evaluation methods, indicating the procedures and tools used for evaluating the relevance of this activity. Specify parts of your business included in the analysis and the criteria used to decide that the activity was not relevant.

- If you selected the dropdown "Analysis in progress" in column 1, provide a date for when it will be finalized in this column.

- If you selected "Not evaluated due to lack of internal resources", specify the main challenges you experience to performing such analysis.

- If you selected "Not evaluated due to insufficient data on operations" or "Not evaluated due to lack of internal resources", indicate if you have any plans to evaluate the relevancy of this activity to your climate change disclosure in the next two years and if so, describe the methods and coverage for this upcoming analysis.

(C-AC0.6f/C-FB0.6f/C-PF0.6f) Why are emissions from distribution activities within your direct

operations not relevant to your current CDP climate change disclosure?

Question dependencies

This question only appears if you select "Elsewhere in the value chain only" in response to the "Distribution" row in C-AC0.6/C-FB0.6/C-PF0.6.

Change from last year

No change

Rationale

This information provides further context to data users about why you have indicated that distribution activities, pertaining to your direct operations, are not relevant to this disclosure and whether you have fully assessed the potential climate-related risks and impacts to your business related to these activities.

Response options

Please complete the following table:

| Primary reason

|

Please explain

|

|

Select from:

- Outside the direct operations of my organization

- Analysis in progress

- Evaluated but judged to be unimportant

- Not evaluated due to insufficient data on operations

- Not evaluated due to lack of internal resources

- No instruction from management

- Other, please specify

|

Text field [maximum 4,000 characters]

|

Requested content

Primary reason (column 1)

- Select the option that best describes the primary reason for why you indicated that emissions from distribution activities pertaining to your direct operations are not relevant to this disclosure.

- If none of the reasons are suitable, select "Other, please specify" and indicate the primary reason distribution activities pertaining to your direct operations are not relevant for your organization. If you need more than 40 characters, please use column 2 "Please explain".

Please explain (column 2)

- If you selected "Outside the direct operations of my organization", "Analysis in progress" or "Evaluated but judged to be unimportant", describe your evaluation methods, indicating the procedures and tools used for evaluating the relevance of this activity. Specify parts of your business included in the analysis and the criteria used to decide that the activity was not relevant.

- If you selected the dropdown "Analysis in progress" in column 1, provide a date for when it will be finalized in this column.

- If you selected "Not evaluated due to lack of internal resources", specify the main challenges you experience to performing such analysis.

- If you selected "Not evaluated due to insufficient data on operations" or "Not evaluated due to lack of internal resources", indicate if you have any plans to evaluate the relevancy of this activity to your climate change disclosure in the next two years and if so, describe the methods and coverage for this upcoming analysis.

(C-AC0.6g/C-FB0.6g/C-PF0.6g) Why are emissions from the consumption of your products not relevant

to your current CDP climate change disclosure?

Question dependencies

This question only appears if you select "No" in response to the "Consumption" row in C-AC0.6/C-FB0.6/C-PF0.6.

Change from last year

No change

Rationale

This information provides further context to data users about why you have indicated that the consumption and end of life treatment of your products are not relevant to this disclosure and whether you have fully assessed the potential climate-related risks and impacts to your business related to these activities.

Response options

Please complete the following table:

| Primary reason

|

Please explain

|

|

Select from:

- Analysis in progress

- Evaluated but judged to be unimportant

- Not evaluated due to insufficient data on operations

- Not evaluated due to lack of internal resources

- No instruction from management

- Other, please specify

|

Text field [maximum 4,000 characters]

|

Requested content

Primary reason (column 1)

- Select the option that best describes the primary reason for why you indicated that emissions from the consumption of your products are not relevant to this disclosure.

- If none of the reasons are suitable, select "Other, please specify" and indicate the primary reason emissions from the consumption of your products are not relevant for your organization. If you need more than 40 characters, please use column 2 "Please explain".

Please explain (column 2)

- If you selected "Analysis in progress" or "Evaluated but judged to be unimportant", describe your evaluation methods, indicating the procedures and tools used for evaluating the relevance of this activity. Specify parts of your business included in the analysis and the criteria used to decide that the activity was not relevant.

- If you selected the dropdown "Analysis in progress" in column 1, provide a date for when it will be finalized in this column.

- If you selected "Not evaluated due to lack of internal resources", specify the main challenges you experience to performing such analysis.

- If you selected "Not evaluated due to insufficient data on operations" or "Not evaluated due to lack of internal resources", indicate if you have any plans to evaluate the relevancy of this activity to your climate change disclosure in the next two years and if so, describe the methods and coverage for this upcoming analysis.

Agricultural commodity dependency

(C-AC0.7/C-FB0.7/C-PF0.7) Which agricultural commodity(ies)

that your organization produces and/or sources are the most significant to your

business by revenue? Select up to five.

Change from last year

No change

Rationale

This question gathers information that enables CDP data users to understand how reliant your business is on agricultural commodities that:

- are highly dependent on natural capital and its associated ecosystem services that are under risk due to climate change; and/or

- are closely associated with high CO2e emissions, either from their production/exploitation or from processing/manufacturing/distribution activities.

This information signals your organization’s exposure to climate-related risks.

Revenue has been chosen as the unique metric to express business dependency, as it is already calculated by many organizations and provides a clear message to investors about an organization's financial dependency. CDP acknowledges that this metric may have caveats, including the impact of yearly fluctuations in currency, which could represent a challenge to responders. However, establishing a standard metric helps data users evaluate and compare various organizations within the sector.

Response options

Please complete the following table. You are able to add rows using the "Add Row" button at the bottom of the table.

| Agricultural commodity

|

% of revenue dependent on this agricultural commodity

|

Produced or sourced

|

Please explain

|

|

Select from:

- Cattle products

- Cotton

- Fish and seafood from aquaculture

- Palm Oil

- Rice

- Soy

- Sugar

- Timber

- Tobacco

- Wheat

- Rubber

- Other, please specify

|

Select from:

- Less than 10%

- 10-20%

- 20-40%

- 40-60%

- 60-80%

- More than 80%

- Don’t know

|

Select from:

|

Text field [maximum 4,000 characters]

|

[Add Row]

Requested content

General

- Organizations are expected to report information for a maximum of five commodities.

- CDP recognizes that some organizations may not be able to report their top five commodities in terms of revenue dependency. If that is the case, respondents should still select their commodities and explain why revenue information is not available.

Agricultural commodities (column 1)

- Select the top five commodities according to their percentage of revenue associated.

- If none of the options apply to your organization, select "Other, please specify" and specify your commodity. Note that you should specify only one additional commodity.

% of revenue dependent on these agricultural commodities (column 2)

- If you do not know or do not calculate the percentage of revenue dependent upon these commodities, please select "Don’t know" and explain why in column 4 "Please explain".

Please explain (column 4)

- Provide details on how the "% of revenue" in column 2 that was dependent on the commodity was calculated. Specify if there are any exclusions and the rationale for such exclusions.

- If you select the option "Don’t know" in column 2 (% of revenue…), explain why you listed that agricultural commodity as one of the five most important for your business.

- If you are unable to provide revenue data because you use a different metric to evaluate your key agricultural commodities, please explain why this is the case and specify the metric you use.

- If you do not consider any of your key commodities under risk due to climate change or large CO2e emissions, provide an explanation here and specify if this statement is the result of an evaluation made.

Example response

| Agricultural commodity | % of revenue dependent on this agricultural commodity | Produced or sourced | Please explain |

|---|

| Cattle products | 20-40% | Produced | The largest percentage of our revenue (approximately

39%) is associated with beef and other cattle products that are produced in our

own farms. To calculate this figure, we have considered all of our own-branded cattle

products and their associated revenue in the past financial year. |

| Soy | 10-20% | Produced; Sourced | Soybeans for animal feed constitute 12% of our

total revenue. To calculate this figure, we have considered all of our soy-based

animal feed production and its associated revenue in the past financial year. |

Explanation of terms

- Revenue: Income arising in the course of an entity’s ordinary activities (less returns, allowances and discounts) - before deducting costs for the goods/services sold and operating expenses to arrive at profit (based on the International Financial Reporting Standard)