Supported by:

Copyright © 2020 CDP Worldwide. All rights reserved.

CDP Climate Change Questionnaire Preview and Reporting Guidance 2020 - Version Control

| Version number

|

Release/Revision date

|

Revision summary

|

| 1.0

|

Released: December 16, 2019

|

The

2020 climate change questionnaire preview and preliminary version

of the reporting guidance was released.

|

| 2.0

|

Released: March 13, 2020

|

- C1.1a, C2.2a: Modification to “Requested content” for “Please explain”.

- C2.3a: Modification to “Requested content” for “Explanation of financial impact figure” and “Description of response and explanation of cost calculation”.

- C2.4a: Modification to “Requested content” for “Explanation of financial impact figure” and “Strategy to realize opportunity and explanation of cost calculation”.

- C3.1d, C3.1e: Modification to “Requested content” for “Description of influence”.

- C3.1f: Updated character limit to 7000 characters.

- C6.10: Modification to “Requested content” for “Reason for change”.

- C8.2e: Modification to “Requested content”.

Real estate and construction sectors:

- C-CN6.6c/C-RE6.6c, C-RE9.9a, C-CN9.10a/C-RE9.10a: Property classification updated in line with 2020 GRESB Real Estate Assessment – column header renamed to “Property sector” and drop-down options revised.

Financial services sectors:

- C2.3a: Modification to a drop-down option in ”Primary potential financial impact”.

- C-FS2.2f: Modification to “Please explain”.

|

| 2.1 |

Released: March 31, 2020 |

- C3.1d, C3.1e, C4.2a: Added "Example response".

|

| 2.2 |

Released: April 14, 2020 |

- The Terms were added for the 2020 Investor and Supply Chain questionnaires.

- The Deadline for submission was updated to: August 26, 2020.

|

| 2.3 |

Released: May 7, 2020 |

- C3.1e: Updated character limit to 7000 characters for "Description of influence".

|

| 2.4 |

Released: May 28, 2020 |

- C-EU8.2d: Modification to “Requested content” and “Change

from last year”.

- C-MM9.3a: Modification to “Requested content” for “Production, copper-equivalent units, metric tons”.

- C-MM9.3b: Modification to “Change from last year”.

|

| 2.5 |

Released: June 11, 2020 |

- C8.2e: Modification to “Requested content” for “General” and “MWh consumed accounted for at a zero emission factor”

|

CDP disclosure cycle 2020

Accessing questionnaire previews, reporting guidance, and scoring methodologies

CDP’s corporate questionnaire previews, reporting guidance, and scoring methodologies for climate change, forests and water security can be accessed from the guidance for companies page of CDP's website.

Submitting a response to the questionnaire(s)

Responses to questionnaires must be submitted via CDP's Online Response System (ORS), which is part of CDP's online disclosure platform. Please refer to Using CDP's Online Disclosure Platform for more details. Please note that while the questions themselves are the same in the questionnaire preview as they are in the ORS, the display format of some questions may differ, particularly for drop-down options and tables.

Sector-specific questions

Companies in high-impact sectors, in addition to the general questions, will be presented with questions specific to that sector. The rationale for developing a refined questionnaire for each of these sectors is outlined in the relevant sector introduction.

The sector-specific questions to companies are defined by CDP's Activity Classification System (CDP-ACS). This system categorizes companies by focusing on the activities from which they derive revenue and associating these with the impacts to their business from climate change, water security and deforestation.

Please note that since each questionnaire includes sector-specific questions throughout, and not all questions will be applicable to your organization, some question numbers may skip.

Full and Minimum versions of the questionnaire

All organizations completing the climate change, forests and water security questionnaires are eligible to complete the full questionnaire.

In some cases, organizations may be eligible to complete a minimum version which contains fewer questions, and no sector-specific questions or data points. Organizations are eligible to complete the minimum version in the following circumstances:

- They are disclosing to that questionnaire for the first time; OR

- They are not disclosing to that questionnaire for the first time, but have an annual revenue of less than EUR/US $250 million*

Organizations opting to complete a minimum version will only be eligible for scoring if they are submitting a response to customers (CDP Supply chain members). For more information on scoring eligibility and implications, please see our Scoring Introduction.

* For previous responders to a questionnaire with an annual revenue of less than EUR/US$250 million, CDP reserves the right to remove the option of a minimum version questionnaire due to the organization’s potential or existing environmental impact.

Timeline:

December 2019

|

- Preview of 2020 questionnaires and preliminary version of reporting guidance released on CDP website.

|

| March 2020

|

- Final version of reporting guidance and scoring methodologies released on CDP website.

|

| April 2020

|

- Online Response System (ORS) opens in the week commencing 13 April 2020.

|

| August 2020

|

- Companies must submit their responses to investors and/or customers using the ORS by 26 August 2020 to be eligible for scoring and inclusion in reports (where applicable).

|

For any disclosure-related enquiries, please contact your regional CDP contact, or [email protected].

CDP climate change questionnaire

This questionnaire is the property of CDP Worldwide, reproduction of all or part (including within software platforms) without permission of CDP Worldwide is prohibited. Please contact [email protected] for more information on this.

Introduction to CDP's climate change program and questionnaire

The 2015 Paris Agreement was a tipping point in the global approach to climate change. By agreeing to limit global temperature rises to well below 2°C, governments have committed to transforming to a low-carbon economy. This transition will create winners and losers within and across business sectors, as the manifestation of climate-related opportunities and risks accelerates in both size and scope. Business as usual will not be a good indicator of how companies will perform.

CDP believes that improving corporate awareness through measurement and disclosure is essential to the effective management of carbon and climate change risk. We request information on climate risks and low-carbon opportunities from the world’s largest companies on behalf of investors, customers, and policy makers.

Regulators have begun to respond to the risks, notably with the Task Force on Climate-related Financial Disclosures (TCFD). Established by the Financial Stability Board, the TCFD has moved the climate disclosure agenda forward by emphasizing the link between climate-related risk and financial stability. The Task Force has recommended that both companies and investors disclose climate change information. This includes whether they are conducting scenario analysis in line with a 2-degree pathway and then setting out how climate-related issues impact their strategy and financial planning. This amplifies the long-standing call from CDP’s investor signatories for companies to disclose comprehensive, comparable environmental data in their mainstream reports, driving climate-related risk management further into the boardroom.

Commit to Action

CDP and its partners in the We Mean Business coalition have created a central platform for companies to tackle key climate issues, with hundreds of companies from every economic sector and geography taking action to date. The We Mean Business “Take Action” platform gives companies a clear pathway for building the Paris Agreement into their business strategies and to future-proof growth, giving policy makers the confidence in raising their ambitions as governments prepare to ratchet up their national pledges in 2020.

Companies who have made commitments through We Mean Business can track progress against them via CDP’s annual disclosure requests. For example, companies can track their commitment to adopt a science-based emissions reduction target by answering C4.1 and C4.2 sub-questions in detail. For more specific information on each commitment and how companies can report on their progress in the relevant sections of CDP’s questionnaires, please refer to the "Commit to Action Technical Note".

Climate change questionnaire structure

There are 14 modules in the general climate change questionnaire, including the Introduction and Signoff modules, plus a module presented only to organizations that are responding to a customer request from one or more CDP Supply Chain Members. The journey through CDP’s general climate change questionnaire includes the following:

- Governance

- Risks and opportunities

- Business strategy

- Targets and performance

- Emissions methodology

- Emissions data

- Energy

- Additional metrics

- Verification

- Carbon pricing

- Engagement

Sector approach

The structure of the CDP climate change questionnaire was redesigned in 2018 in response to market needs and trends in corporate climate change reporting. Revisions included the inclusion of the TCFD recommendations, an increased emphasis on forward-looking metrics, improved alignment with other reporting frameworks, and the integration of sector-specific questions.

For climate change, CDP has incorporated sector-specific questions for 16 high-impact sectors.

Each question number in the climate change questionnaire begins with the letter C. Questions that are unique to companies in a particular sector are labelled using a two-letter abbreviation within the question number. These abbreviations are noted below.

2020 climate change sectors:

- Agriculture: Agriculture commodities (AC); Food, beverage & tobacco (FB); Paper & forestry (PF)

- Energy: Coal (CO); Electric utilities (EU); Oil & gas (OG)

- Financial: Financial services (FS)

- Materials: Cement (CE); Capital goods (CG); Chemicals (CH); Construction (CN); Metals & mining (MM); Real estate (RE); Steel (ST)

- Transport: Transport services (TS); Transport OEMs (TO)

Climate change questionnaire changes in 2020

The changes for 2020 complete CDP’s alignment with the sectors included in the TCFD recommendations. Other changes include revisions to simplify existing modules and questions, correct errors and improve alignment across CDPs questionnaires.

Modifications include:

- New sector-specific questions for the capital goods, construction, financial services, and real estate sectors.

- Modules C2, C3 and C4 revised to remove repetitions, clarify the data requested and improve question pathways.

- Some general questions removed for the electric utilities and financial services sectors.

Revisions and changes are indicated within the questionnaire as: “no change”, “minor change” or “modified question”. “Minor change” indicates wording edits and revisions to drop-down options or a simple clarification, while a “modified question” indicates that the data requested has been revised. A detailed document on climate change question changes from 2019 to 2020 can be found on the Guidance page of the website.

Preparing your CDP response

CDP disclosure support

CDP provides a variety of support materials to help organizations disclosing to our questionnaires. Before completing the corporate questionnaires, we strongly recommend you read the relevant Reporting Guidance, Scoring Introduction document, and relevant Scoring Methodology. Please also see our Frequently Asked Questions.

Reporting guidance

CDP's reporting guidance includes the following sections:

- Module-level guidance: for select modules this guidance provides an overview, key changes, sector-specific content for the module, and important disclosure notes. This section also presents question pathway diagrams showing the flow of questions through each module.

- Question-level guidance: at the question level, guidance is separated into the following components, to provide clarity around questions, terminology and requirements.

- Rationale: provides reasoning behind the inclusion of each question;

- Connections to other frameworks: notes connections to the Sustainable Development Goals (SDGs), RobecoSAM Corporate Sustainability Assessment (DJSI), and Task Force on Climate-related Financial Disclosures (TCFD) for each relevant question in the climate change questionnaire;

- Requested content: offers context around each question and requested criteria;

- Explanation of terms: provides detailed definitions for specific terminology;

- Example responses: for select questions, this provides an example of a response that would include all information requested; and

- Additional information: for select questions, this provides optional contextual information and sources related to the subject of the disclosure request.

- Glossary: viewable at the end of the reporting guidance, the glossary contains a subset of "Explanation of terms".

- Appendix A: Agricultural/Forestry management practices.

If you have any questions that are not answered in the reporting guidance, the additional guidance noted below, or our Frequently Asked Questions, please contact your local CDP office or [email protected].

Additional CDP guidance

In addition to the reporting guidance, scoring methodologies and a selection of technical notes can be found on the guidance for companies page of CDP's website. The full suite of technical notes and guidance materials are accessible from the guidance tool after signing in (updating in progress until March 2020).

Webinars and workshops

CDP hosts live webinars and workshops designed to aid you with environmental reporting.

Please visit the workshops and webinars and climate change pages of CDP's website for more details.

CDP Reporter Services

CDP Reporter Services program offers tailored support, enhanced data access and thought leadership on managing and reporting environmental risk to your business. Access the tools you need to move from disclosure to leadership on integrating climate, forests management, and water security into your wider business strategy. For year-round, personalized disclosure support from a dedicated CDP account manager, a gap analysis of your previous response, final review before submission, and analytics tools to benchmark yourself against peers and understand best practice contact [email protected]. Visit the Reporter Services page of CDP's website for more information.

CDP accredited solutions providers

CDP partners with leading environmental service providers that can support companies throughout all stages of the measurement, reporting and management of their climate and sustainability data and impacts. All CDP solutions providers have met specific accreditation criteria. See provider areas of expertise below, and visit the accredited solutions provider directory to search for the provider best able to support you:

- Carbon reduction solutions providers offer technology and services that can help your organization reduce carbon emissions and improve energy efficiency.

- Climate consultancy solutions providers have a wide range of technical expertise to support companies with establishing and implementing climate change and sustainability strategies.

- Science-based target (SBT) accredited providers have expertise in helping companies to set and implement targets in line with what the latest climate science says is necessary.

- Education & training service providers improve employee awareness and understanding of how climate change affects their organization through carbon management training programs.

- Renewable energy solutions providers provide expertise in procuring, tracking, and generating renewable power.

- Software solutions providers simplify the collection, monitoring, and reporting of sustainability, CSR, and environmental data through integrated sustainability software applications.

- Verification solutions providers help organizations disclose accurate data and improve internal processes by providing third-party verification and assurance of emissions data, a practice recommended by CDP.

As well as visiting our accredited solutions provider webpage, you can also contact [email protected] to find out more.

Notes for completing your disclosure

Acronyms

Avoid using bespoke internal acronyms unless required for your organization’s response, in which case please provide their meaning to enable correct analysis and scoring.

Blank responses

Leaving a response blank is interpreted as non-disclosure. For numeric fields, values of zero (0) imply a measurement has been made, and the value is zero (0). For numeric fields where no measurement has been made, please leave the field blank and provide an explanation in an open text field for that same question (e.g. "Comment" or "Please explain"). If there is no open text field for the question, you may provide an explanation in the "Further information" field in the ORS at the end of your disclosure. Leaving a response blank and entering a value of zero (0) have different scoring implications. Please see the scoring methodology for more details.

Character limits

Limits noted in the guidance and the ORS include spaces.

"Comment" column

Some questions include a column labelled as "Comment". Note that providing information in these columns is optional.

Company-specific information

Some questions request company-specific information. Be sure to include company-specific detail, such as references to activities, programs, products, services, methodologies, or operating locations unique to your company’s business or operations. A company-specific explanation should include details that make the answer true for the responding company and are distinct from other companies in the same industry and/or geography. This level of detail gives data users confidence that the issue at hand has been thoroughly considered in the context of the responder’s own business and not simply assessed in general terms.

Consistency

CDP encourages a comprehensive and consistent response. Please ensure there is no conflicting information in your responses, both within a question and across the questionnaire.

Copy from last year

The "copy from last year" functionality will be available in the ORS for companies that disclosed to CDP in the previous reporting year.

Note that this functionality may have been disabled for modified data points. The reporting guidance will indicate which questions have been modified. The Questionnaire Changes document on the guidance section of the CDP website lists all revisions. Your responses should always be checked before submission.

Data accuracy

CDP recognizes that there may be uncertainty linked to data – this can arise from data gaps, assumptions, metering/measurement constraints including equipment accuracy etc. CDP allows estimated data to be submitted. However, an emphasis is placed on reporting transparently and this means that a company should always provide an explanation when its reported data is not accurate and detail the uncertainty (use the "Please explain" or "Comment" columns provided in the question).

Drop-down options ("Other, please specify")

Please select from the options provided whenever possible, and only select "Other, please specify" when none of the listed options is appropriate. This greatly assists data analysis. If selecting "Other, please specify", you must add a label that describes the option you are providing data for.

"Further information" field

At the end of the questionnaire, there is an opportunity to provide additional information or context that you feel is relevant to your organization’s response. This field is optional and not scored.

Mergers and acquisitions (M&As)

All disclosure should be defined by the organizational boundary applicable at the time of the stated reporting period. (Note that for CDP disclosure, organizations are encouraged to align their reporting period and organizational boundaries with their financial reporting).

Regarding forward-looking disclosure, organizations should include information that was correct at the time of the stated reporting period (for example, for data points referring to the future or "the next two years"). Organizations undergoing (or that have undergone) M&As need to consider the timing of the M&As and reporting period as follows:

- Organizations that were acquired after the end of the current reporting period: these should respond with what was planned (strategy, targets, etc.) before being acquired (i.e., during the reporting period). For transparency, where possible they may state where they consider that the forward-looking information may be subject to change due to the very recent acquisition.

- Organizations that were acquired during the reporting period: these should provide information that was applicable and correct to the best of their knowledge at the end of the reporting period. At the time of submitting their response to CDP, this information may not be the most up to date due changes underway following the acquisition. For transparency, the company may state this in their disclosure where possible.

Personal data

It is important that you do not include the name of any individual or any other personal data in your response. For questions that ask for the positions of staff, out of respect for personal data privacy we are asking only for the position and not for the individual’s name or any other information relating to them.

Providing feedback to CDP

You can provide feedback to CDP on the content of our questionnaires and supporting documents through our online technical feedback form.

We are unable to respond individually to all feedback, but please be assured that all form submissions are reviewed and contribute towards our continuous improvement. However, if you represent a responding organization and would like to request a response, please email [email protected] or your local CDP contact.

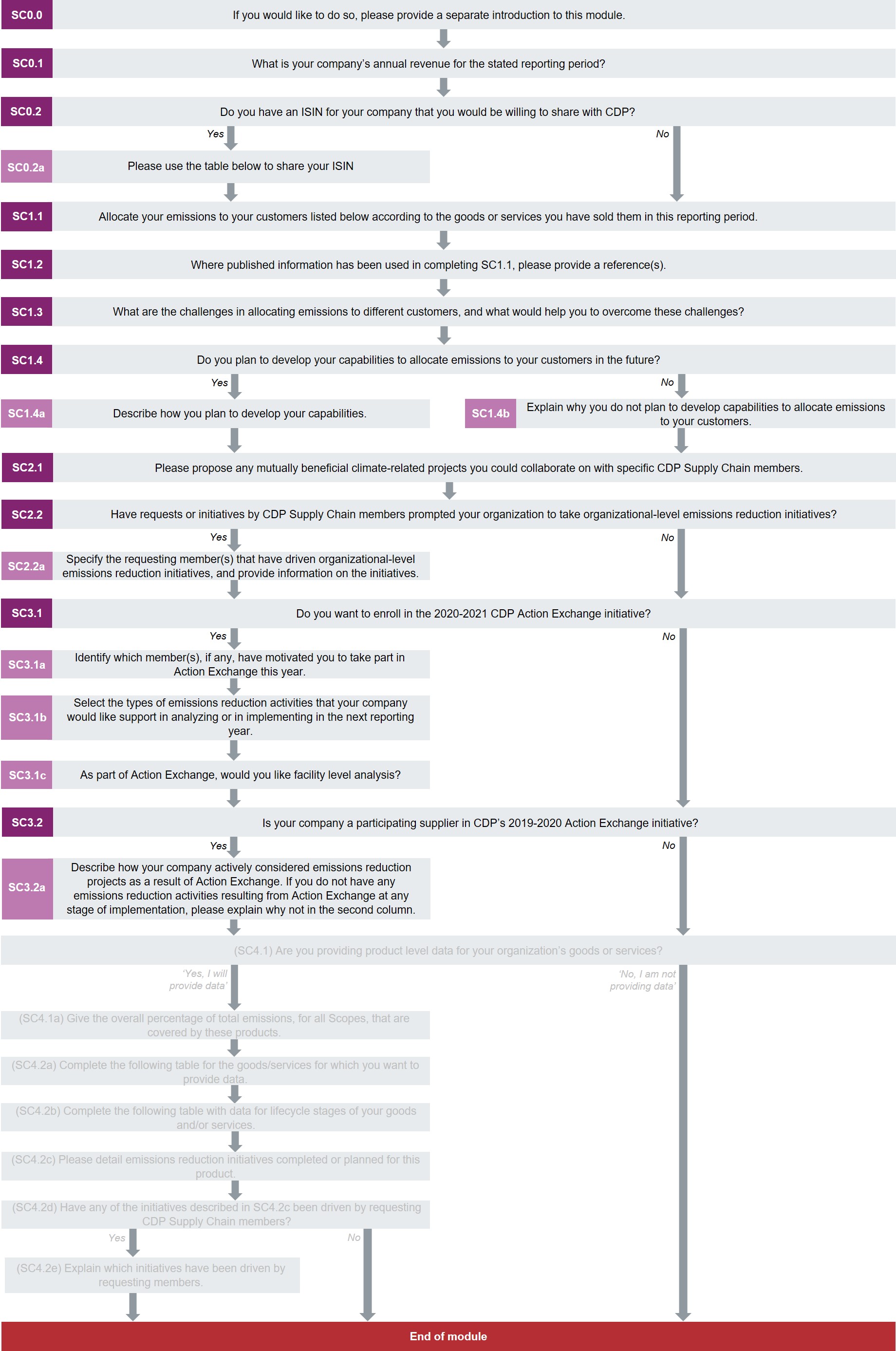

C0 Introduction

Module Overview

This module requests information about your organization’s disclosure to CDP and will help data users to interpret your responses in the context of your business operations, timeframe and reporting boundary.

The information provided here should apply consistently to your responses throughout the questionnaire and be complete and accurate as it may determine response options presented in subsequent modules.

For this reason, you should respond to every question in this module before accessing the rest of the questionnaire.

Key changes

- New questions have been added for the construction, real estate and financial services sectors: C-CN0.7/C-RE0.7 and C-FS0.7.

- Click here for a list of all changes made this year.

Sector-specific content

Additional questions on organizational activities for the following high-impact sectors:

- Agricultural commodities

- Capital goods

- Cement

- Chemicals

- Coal

- Construction

- Electric utilities

- Financial services

- Food, beverage and tobacco

- Metals & mining

- Oil & gas

- Paper & forestry

- Real estate

- Steel

- Transport original equipment manufacturers (OEMs)

- Transport services

Pathway diagram - questions for minimum version questionnaire

This diagram shows the questions contained in module C0 that are included in the minimum version of the questionnaire. To access question-level guidance, use the menu on the left to navigate to the question.

Introduction

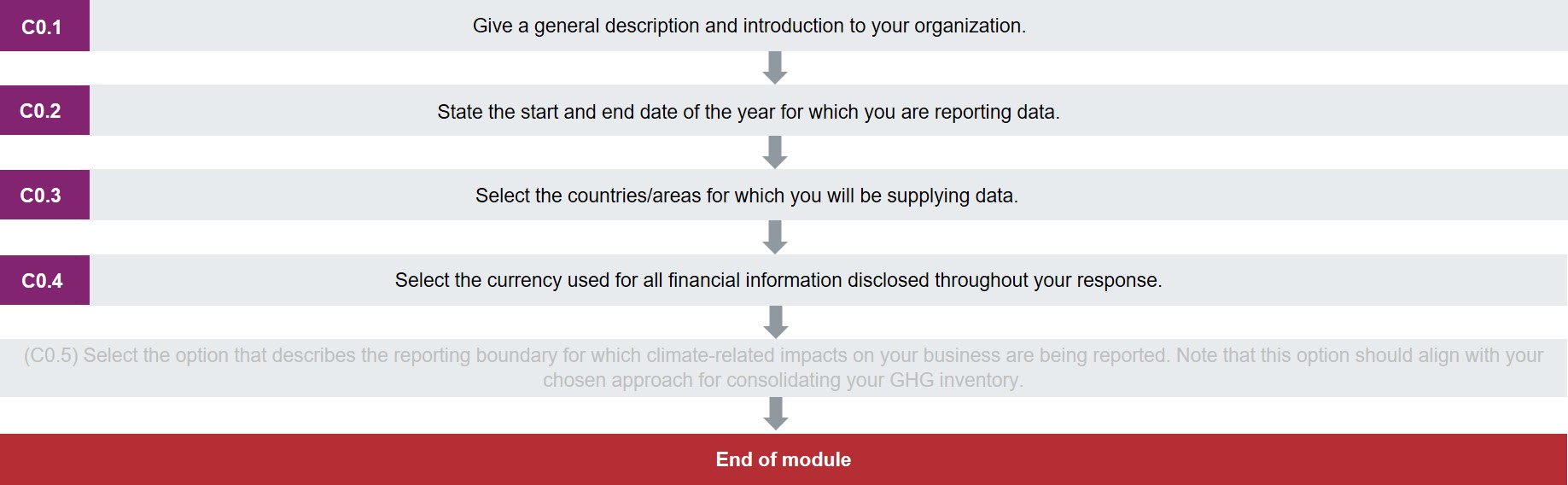

(C0.1) Give a general description and introduction to your organization.

Change from 2019

No change

Rationale

This will help data users interpret your responses.

Response options

This is an open text question with a limit of 5,000 characters.

Please note that when copying from another document into the ORS, formatting is not retained.

Requested content

General

- Provide information about your operations to help data users understand your greenhouse gas (GHG) emissions inventory and corporate climate change strategy. Include information on your business divisions and your emissions-generating activities (e.g. extraction and/or processing/refining of natural resources, electricity generation, transportation, manufacturing etc.).

-

This information helps data users understand your company’s emissions profile and differences in emissions figures between peer companies.

-

Note and explain any changes in your reporting year (C0.2) from previous CDP disclosures (e.g. from reporting calendar year to financial year, or vice versa).

Explanation of terms

- Organization: Throughout this questionnaire, “your organization” refers collectively to all the companies, businesses, other entities or groups that fall within the definition of your reporting boundary (provided in C0.5). This term is used interchangeably with “your company”, but CDP recognizes that some disclosing organizations may not consider themselves to be, or be formally classified, as “companies”.

(C0.2) State the start and end date of the year for which you are reporting data.

Change from 2019

No change

Rationale

This will help data users interpret your responses.

Response options

Please complete the following table.

| Start date

|

End date

|

Indicate if you are providing emissions data for past reporting years

| Select the number of past reporting years you will be providing emissions data for |

|

From: [DD/MM/YYYY]

|

To: [DD/MM/YYYY]

|

Select from: |

Select from:

|

Requested content

General

- Apply this reporting year to your answers for the entire questionnaire unless the ability is provided to specify other reporting periods.

- Please ensure that the reporting period represents only one full year that has already passed. Reporting periods should not be in the future. This information is important for others to understand the time dimension of your disclosure.

- If you are using the Export/Import functionality, please check that the imported date is correct.

- The current reporting year is the most recent 12-month period for which data is reported.

- This reporting period applies to all answers except where other reporting periods can be disclosed. CDP does not require companies to align their reporting year with their fiscal year. However, when organizations report emissions intensity using a financial metric, both emissions and financial information provided should align with the reporting year reported here.

- Note that the investment community generally prefers a company's disclosure period to match the fiscal year for their financial jurisdiction. This facilitates the assessment of environmental performance data in alignment with financial performance data.

- CDP recommends that companies provide a year for which they have complete data if possible. However, if you do not have data for the entirety of your reporting year, you have the following options:

- Extrapolate your data to cover the entire reporting year.

- Outline in C6.4 the sources of Scope 1 and 2 emissions within your selected reporting boundary and not included in your disclosure.

- Select "No" in column 3 (Indicate if you are providing data for past reporting years) unless you are a first time responder providing emissions from past years or a previous responder to CDP who is restating your emissions data. For more information on this see the note for first-time responders and the note for restating data below.

- If multiple years of data are provided, only data pertaining to the most recent reporting year will be scored.

Note for first-time responders:

- If you have not provided emissions data before, supply gross global Scope 1 and Scope 2 emissions data for the three years prior to the current reporting year in the emissions accounting questions (C6.1 and C6.3).

- To report emissions data for years prior to the current reporting year select "Yes" in column 3 (Indicate if you are providing emissions data for past reporting years). Then select how many years of emissions data you will be providing.

- This will enable you to enter multiple years of data when you reach questions C6.1 and C6.3.

Note for restating data:

- You may also choose to restate your emissions data previously supplied to CDP, for example to ensure that your historical data reflects your current organizational boundary.

- Reporting recalculated figures for these years is optional. However, if you wish to do this it can provide transparency to stakeholders using your data.

- If you choose to restate data previously supplied to CDP, report the dates of those reporting periods here by selecting "Yes" in column 3 (Indicate if you are providing emissions data for past reporting years). Then select how many years of emissions data you will be providing.

- This will enable you to enter multiple years of data when you reach questions C6.1 and C6.3.

- When you arrive at the relevant questions that need to be restated (C6.1 and C6.3), use the comment column to identify the reason for the restatement.

- For more information on restatements see CDP's technical note on restatements here.

(C0.3) Select the countries/areas for which you will be supplying data.

Change from 2019

Minor change

Rationale

This will help data users interpret your responses.

Response options

Please complete the following table:

| Country/area

|

|

Select all that apply:

[Country/area drop-down list]

|

Requested content

General

- Select all countries/areas in which you operate from the drop-down menu provided.

(C0.4) Select the currency used for all financial information disclosed throughout your response.

Change from 2019

No change

Rationale

CDP encourages companies to report financial figures associated with their impacts, risks, and opportunities. Establishing a single currency will facilitate the collection of comparable financial information. This will benefit investors and other data users when assessing the costs and benefits reported by your organization.

Response options

Please complete the following table:

| Currency

|

|

Select from:

[Currency drop-down list]

|

Requested content

General

- Select the currency to be applied to all financial information reported in this disclosure.

- For example, if you select USD($), provide metric tons CO2e per USD($) as the financial intensity metric in question C6.10.

C1 Governance

Module Overview

Board-level oversight of climate-related issues is considered best practice and provides an indication of the importance of climate-related issues to the organization.

This module is intended to capture the governance structure of your company with regard to climate change, and provides data users with an understanding of the organization's approach to climate-related issues at the board level and management level.

Key changes

For the financial services sector only:

- New question: C-FS1.4.

- Modified questions: C1.1b, C1.2 - new columns.

- New response options: C1.1a column 1, C1.3a columns 1 and 3.

- Click here for a list of all changes made this year.

Sector-specific content

Additional questions on retirement schemes for the following high-impact sectors:

Pathway diagram - questions for minimum version questionnaire

This diagram shows the questions contained in module C1 that are included in the minimum version of the questionnaire. To access question-level guidance, use the menu on the left to navigate to the question.

Board oversight

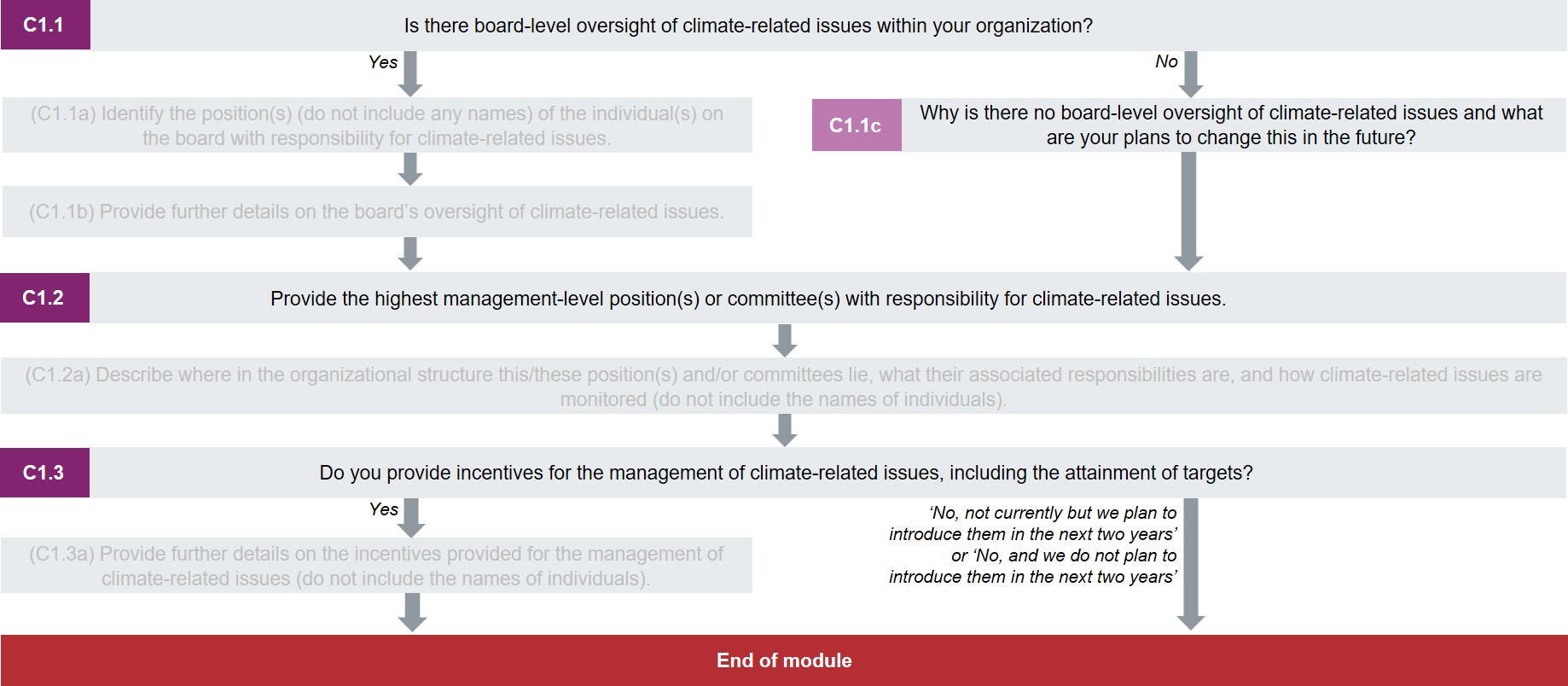

(C1.1) Is there board-level oversight of climate-related issues within your organization?

Change from 2019

No change

Rationale

This question provides an indication of the importance of climate-related issues to your business. Investors and other data users are interested in an organization's understanding and approach to climate-related risks at the board level; how aligned this is with business strategy, policies, and performance objectives; and how the board monitors progress against targets and goals. This question supports TCFD’s Governance recommendation a) Describe the board’s oversight of climate-related risks and opportunities.

Connection to other frameworks

SDG

Goal 12: Responsible consumption and production

Response options

Select one of the following options:

Requested content

General

- Consider whether the board and/or board committees take account of climate-related issues when reviewing and guiding their business strategy, major plans of action, risk management policies, annual budgets, and budget plans as well as setting the organization's performance objectives, monitoring implementation and performance, and overseeing major capital expenditures, acquisitions, and divestitures.

- If your organization has board-level oversight of risk assessment that includes climate-related risks, select "Yes". You'll be able to provide details in subsequent questions.

Note for financial services sector companies:

- Consider whether the board and/or board committees have oversight of climate-related issues in relation to the financial activities undertaken by your organization such as lending, financial intermediary, investment and/or insurance underwriting activities, in addition to operational activities.

- Further details can be provided in subsequent questions C1.1a and C1.1b

Explanation of terms

- Board: Or “Board of Directors” refers to a body of elected or appointed members who jointly oversee the activities of a company or organization. Some countries use a two-tiered system where “board” refers to the “supervisory board” while “key executives” refers to the “management board".

Additional information

For further information on board-level oversight in governance, see TCFD’s recommendations, CDP’s technical note on the TCFD’s recommendations and “How to Set Up Effective Climate Governance on Corporate Boards - Guiding principles and questions” (World Economic Forum, 2019).

(C1.1c) Why is there no board-level oversight of climate-related issues and what are your plans to change this in the future?

Question dependencies

This question only appears if you select “No” in response to C1.1.

Change from 2019

No change

Rationale

As board-level oversight of climate-related issues is considered best practice, this question allows organizations to explain why there is no board-level oversight.

Response options

Please complete the following table:

| Primary reason

|

Board-level oversight of climate-related issues will be introduced within the next two years.

|

Please explain

|

|

Text field [maximum 1,000 characters]

|

Select from:

- Yes, we plan to do so within the next two years

- No, we do not currently plan to do so

|

Text field [maximum 2,400 characters]

|

Requested content

Primary reason (column 1)

- Provide your organization's main rationale for not currently having board-level oversight of climate-related issues.

Please explain (column 3)

- Explain what you plan to implement in the next two years, or why you do not currently plan to do so.

Management responsibility

(C1.2) Provide the highest management-level position(s) or committee(s) with responsibility for climate-related issues.

Change from 2019

Modified question for FS only

Rationale

While it is most important for a member of the board to have responsibility for climate-related issues, assigning management-level responsibility indicates to CDP data users that the organization is committed to implementing its climate-related strategy.

Connections to other frameworks

TCFD

Governance recommended disclosure b) Describe management’s role in assessing and managing climate related risks and opportunities.

SDG

Goal 12: Responsible consumption and production

Response options

Please complete the following table. You are able to add rows by using the “Add Row” button at the bottom of the table.

| Name of the position(s) and/or committee(s)

|

[FINANCIAL SERVICES ONLY] Reporting line

|

Responsibility

|

[FINANCIAL SERVICES ONLY] Coverage of responsibility

|

Frequency of reporting to the board on climate-related issues

|

|

Select from:

- Chief Executive Officer (CEO)

- Chief Financial Officer (CFO)

- Chief Operating Officer (COO)

- Chief Procurement Officer (CPO)

- Chief Risks Officer (CRO)

- Chief Sustainability Officer (CSO)

- Chief Investment Officer (CIO) [Financial services only]

- Chief Credit Officer (CCO) [Financial services only]

- Chief Underwriting Officer (CUO) [Financial services only]

- Other C-Suite Officer, please specify

- President

- Risk committee

- Sustainability committee

- Safety, Health, Environment and Quality committee

- Corporate responsibility committee

- Credit committee [Financial services only]

- Investment committee [Financial services only]

- Responsible Investment committee [Financial services only]

- Audit committee [Financial services only]

- Other committee, please specify

- Business unit manager

- Energy manager

- Environmental, Health, and Safety manager

- Environment/Sustainability manager

- Facility manager

- Process operation manager

- Procurement manager

- Public affairs manager

- Risk manager

- Portfolio/Fund manager [Financial services only]

- ESG Portfolio/Fund manager [Financial services only]

- Investment/credit/insurance analyst [Financial services only]

- Dedicated responsible investment analyst [Financial services only]

- Investor relations manager [Financial services only]

- Risk analyst [Financial services only]

- There is no management level responsibility for climate-related issues

- Other, please specify

|

Select from:

- Reports to the board directly

- CEO reporting line

- Risk - CRO reporting line

- Finance - CFO reporting line

- Investment - CIO reporting line

- Operations - COO reporting line

- Corporate Sustainability/CSR reporting line

- Other, please specify

|

Select from:

- Assessing climate-related risks and opportunities

- Managing climate-related risks and opportunities

- Both assessing and managing climate-related risks and opportunities

- Other, please specify

|

Select all that apply:

- Risks and opportunities related to our bank lending activities

- Risks and opportunities related to our investing activities

- Risks and opportunities related to our insurance underwriting activities

- Risks and opportunities related to our other products and services

- Risks and opportunities related to our own operations

|

Select from:

- More frequently than quarterly

- Quarterly

- Half-yearly

- Annually

- Less frequently than annually

- As important matters arise

- Not reported to the board

|

[Add Row]

Requested content

General

- Please provide details of the highest management-level position or committee with a responsibility for climate-related issues.

- The responsibility may be for assessing and/or managing climate-related risks and opportunities, or have another primary focus.

- Note that this question asks about the position and not about the names of the staff holding these positions. Do not include the name of any individual or any other personal data in your response.

Name of the position(s) and/or committee(s) (column 1)

- Select the best match for the position/committee in your organization, or select "Other, please specify".

- The list includes senior positions that may sometimes but not always be at board level.

- Note that positions already listed in C1.1a are also listed here; select one of those positions only if the individual has effective management responsibility for climate-related issues.

- If there is more than one position/committee with high management-level responsibility and you would like to describe this, you may use the "Add Row button". This is optional.

- If you are selecting more than one position or committee by adding rows, make sure that the position/committee with the highest level of responsibility is in the top row of the table.

Reporting line [FINANCIAL SERVICES ONLY]

- Select the best match for the reporting line that is in charge of overseeing the positions with responsibility for climate-related issues.

Coverage of responsibility [FINANCIAL SERVICES ONLY]

- This column seeks to understand whether the highest management-level position or committee with responsibility for climate-related issues considers both climate-related risks and opportunities related to your own operations as well as core financing activities.

Explanation of terms

- Highest management-level position(s) or committee(s): The most senior individual or committee with operational responsibility for the implementation of decisions taken at the board level and day-to-day management.

Employee incentives

(C1.3) Do you provide incentives for the management of climate-related issues, including the attainment of targets?

Change from 2019

Modified question

Rationale

CDP data users aim to understand the degree to which companies encourage their employees to address climate-related issues and impacts of the business, as well as the mechanisms by which companies are incentivizing certain behaviors and performances.

Connection to other frameworks

SDG

Goal 12: Responsible consumption and production

Response options

Please complete the following table:

| Provide incentives for the management of climate-related issues

|

Comment

|

Select from:

- Yes

- No, not currently but we plan to introduce them in the next two years

- No, and we do not plan to introduce them in the next two years

|

Text field (maximum 1,000 characters)

|

Requested content

General

- Note that incentives can be positive (i.e. give people something) or negative (prevent access to something).

C2 Risks and opportunities

Module Overview

Evaluating exposure to climate-related risks and opportunities over a range of time horizons allows for a strategy for the transition to a low-carbon economy recognized in the Paris Agreement and UN SDGs. This module focuses on processes for identifying, assessing, and responding to climate-related issues as well as on the climate-related risks and opportunities identified by your organization. This information helps investors to assess the potential impacts to valuations and the adequacy of the company’s risk response.

Many of the challenges you face when reporting on climate-related issues are common to other aspects of corporate reporting, requiring you to provide statements about your prospective condition. Some organizations, particularly accounting firms and their governing bodies, have published guidance about how to prepare statements that contain forward-looking information.

You may wish to consult with your financial, legal, and/or compliance departments for advice on your company’s general approach to the provision of forward-looking statements and information concerning risks.

Note that the questions relate to “inherent” risk and not the “residual” risk that remains after management measures have been taken into account.

Note for financial services sector companies:

The TCFD recommendations highlight the importance of the financial sector considering the impacts of climate-related issues in the context of their financing activities. When evaluating exposure to climate-related risks and opportunities, financial services sector companies should primarily consider the impact on their lending, financial intermediary, investing and/or insurance underwriting activities, in addition to operational activities.

Key changes

This module has been restructured to improve the flow of questions, reduce repetitions, and to better align with CDP’s forests and water security questionnaires. As a result of this, the question numbering has changed.

- Two new questions: C2.1 and C2.1b. The request to provide a definition of a substantive financial or strategic impact has been broken out from 2019 C2.2b into C2.1b.

- Four 2019 questions merged: C2.2, C2.2a, C2.2b and C2.2d have been merged into C2.2.

- Two 2019 questions moved: C2.5 and C2.6 that requested information on impacts of climate-related issues on strategy and financial planning have been integrated into Module C3 Strategy.

- Click here for a list of all changes made this year.

Financial services sector:

- Five new questions: C-FS2.2b, C-FS2.2c, C-FS2.2d, C-FS2.2e, C-FS2.2f.

- Modified question: C2.3a – new column.

- New response options: C2.3a and C2.4a, columns 4 and 5.

Sector specific content

Additional questions for financial services sector companies.

Pathway diagram - questions for minimum version questionnaire

This diagram shows the questions contained in module C2 that are included in the minimum version of the questionnaire. To access question-level guidance, use the menu on the left to navigate to the question.

Management processes

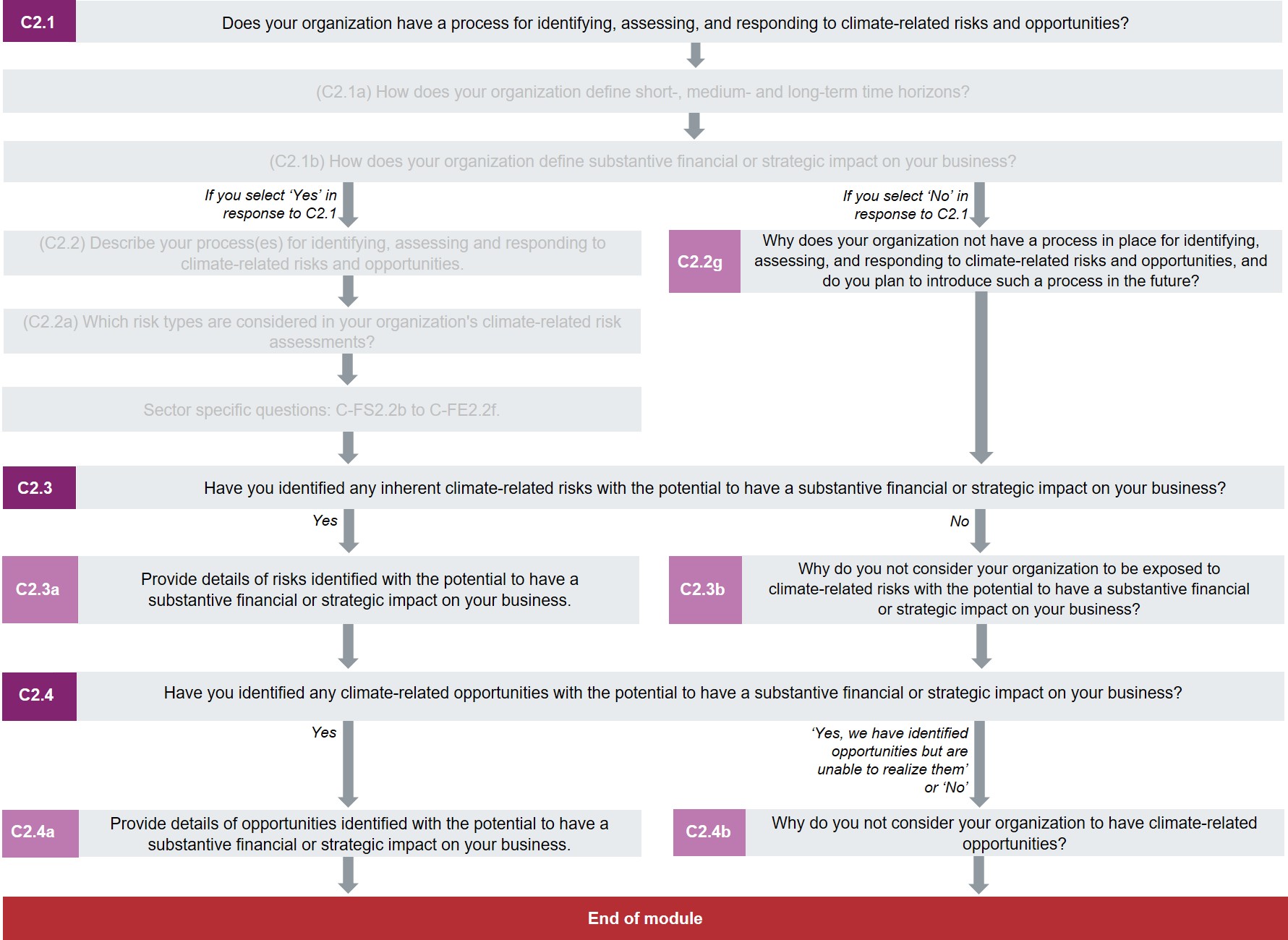

(C2.1) Does your organization have a process for identifying, assessing, and responding to climate-related risks and opportunities?

Change from 2019

New question

Rationale

For many companies, climate change poses significant financial challenges and opportunities, now and in the future. CDP asks about a process for identifying, assessing, and responding to climate-related risks and opportunities so that data users may gauge the thoroughness of your company's understanding of its exposure to climate-related issues.

Connection to other frameworks

TCFD

Risk Management recommended disclosure a) Describe the organization’s processes for identifying and assessing climate-related risks.

Risk Management recommended disclosure b) Describe the organization’s processes for managing climate-related risks

Risk Management recommended disclosure c) Describe how processes for identifying, assessing, and managing climate-related risks are integrated into the organization’s overall risk management.

Response options

Select one of the following options:

Requested content

General

- Select "Yes" if you have any process in place for identifying, assessing, and responding to climate-related risks and opportunities, regardless of how thorough it is. You will be able to provide further details in the subsequent questions.

- Only select "No" if you do not have any form of process for identifying, assessing, and responding to climate-related issues.

Explanation of terms

- Climate-related risk, in line with the TCFD, refers to the potential negative impacts of climate change on an organization. Physical risks emanating from climate change can be event-driven (acute) such as increased severity of extreme weather events (e.g., cyclones, droughts, floods, and fires). They can also relate to longer-term shifts (chronic) in precipitation, temperature and increased variability in weather patterns (e.g., sea level rise). Climate-related risks can also be associated with the transition to a lower-carbon global economy, the most common of which relate to policy and legal actions, technology changes, market responses, and reputational considerations.

- Climate-related opportunity, in line with the TCFD, refers to the potential positive impacts on an organization resulting from efforts to mitigate and adapt to climate change, such as through resource efficiency and cost savings, the adoption and utilization of low-emission energy sources, the development of new products and services, and building resilience along the supply chain. Climate-related opportunities will vary depending on the region, market, and industry in which an organization operates.

- Risk management: Risk management involves identifying, assessing and responding to risk to make sure organizations achieve their objectives. It must be proportionate to the complexity and type of organization involved (based on Institute of Risk Management, 2016).

(C2.2g) Why does your organization not have a process in place for identifying, assessing, and responding to climate-related risks and opportunities, and do you plan to introduce such a process in the future?

Question dependencies

This question only appears if you select “No” in response to C2.1.

Change from 2019

Minor change (2019 C2.2e)

Rationale

A thorough risk and opportunity assessment is integral to addressing climate-related issues. Therefore data users want to understand why your company does not carry out such assessments, as well as any plans to do so in the future. Without a process for managing risks and opportunities, companies may be unable to determine the best ways to prepare for future uncertainties and liabilities, or to capitalize on available opportunities.

Response options

Please complete the following table:

| Primary reason | Please explain |

| Select from: - We are planning to introduce a climate-related risk management process in the next two years

- Important but not an immediate business priority

- Judged to be unimportant, explanation provided

- Lack of internal resources

- Insufficient data on operations

- No instruction from management

- Other, please specify

| Text field [maximum 1,500 characters] |

Requested content

Primary reason (column 1)

- Select the primary reason why your company does not have a process in place to identify, assess, and respond to climate-related issues.

- Select only one option from the drop-down menu. If multiple options reasonably apply to your company, explain any additional reasons in column 2.

- If you select “Other, please specify”, provide a label for the primary reason.

Please explain (column 2)

- Ensure your explanation is company-specific and provides additional details as to why you do not have a process in place, including any specific plans to create a process and the anticipated timeline for its creation. For instance, you may include details on how you are exploring creating a process, using concrete examples from your company’s experience.

- Please also include details of how climate-related risks are addressed as they do arise (such as environmental legislation, weather-related events, or reputational risks related to climate change). Include company-specific examples in your description.

Risk disclosure

(C2.3) Have you identified any inherent climate-related risks with the potential to have a substantive financial or strategic impact on your business?

Change from 2019

No change

Rationale

Investors and data users are interested in learning whether your organization has knowledge at the corporate level of any substantive climate-related risks, across any part of your value chain.

Connection to other frameworks

TCFD

Strategy recommended disclosure a) Describe the climate related risks and opportunities the organization has identified over the short, medium, and long term.

SDG

Goal 13: Climate action

Response options

Select one of the following options:

Requested content

General

- Please indicate if you have identified any inherent climate-related risks.

- For the purposes of this response, the risks reported should only be those which:

- May pose substantive financial or strategic impacts, in line with your definition of substantive impact provided in C2.1b; and

- Are inherent (risks that exist in the absence of controls, i.e. not taking into account any potential mitigation or management measures that have been or could be implemented).

Note for financial services sector companies:

- For the purposes of this response, the risks reported should be inherent and have the potential for substantive impacts on your investing, financing, underwriting and/or operational activities. Further details can be provided in subsequent questions.

(C2.3a) Provide details of risks identified with the potential to have a substantive financial or strategic impact on your business.

Question dependencies

This question only appears if you select “Yes” in response to C2.3.

Change from 2019

Modified question

Rationale

Your response to this question will allow data users to see, in one place, details of the risks posed to your organization by climate-related issues, and also the estimated potential financial impact of these risks at the corporate level and your response strategy to manage these risks.

Connection to other frameworks

TCFD

Strategy recommended disclosure a) Describe the climate related risks and opportunities the organization has identified over the short, medium, and long term.

Strategy recommended disclosure b) Describe the impact of climate-related risks and opportunities on the organization's businesses, strategy and financial planning.

Please note: columns 1-7 align with the TCFD recommendations.

SDG

Goal 12: Responsible consumption and production

Goal 13: Climate action

Response options

Please complete the following table. The table is displayed over several rows for readability. You are able to add rows by using the “Add Row” button at the bottom of the table.

| Identifier

|

Where in the value chain does the risk driver occur?

|

Risk type

|

Primary climate-related risk driver

|

Primary potential financial impact

|

[Financial services only]

Climate risk type mapped to traditional financial services industry risk classification

|

Company- specific description

|

Time horizon

|

Select from:

|

Select from:

- Direct operations

- Upstream

- Downstream

|

Select from:

- Current regulation

- Emerging regulation

- Legal

- Technology

- Market

- Reputation

- Acute physical

- Chronic physical

|

See drop-down options below

|

See drop-down options below

|

Select from:

- Capital adequacy and risk-weighted assets

- Liquidity risk

- Funding risk

- Market risk

- Credit risk

- Reputational risk

- Policy and legal risk

- Systemic risk

- Operational risk

- Strategic risk

- Other non-financial risk

- None

|

Text field [maximum 2,500 characters]

|

Select from:

- Short-term

- Medium-term

- Long-term

- Unknown

|

| Likelihood

|

Magnitude of impact

|

Are you able to provide a potential financial impact figure?

|

Potential financial impact figure (currency)

|

Potential financial impact figure - minimum (currency)

|

Potential financial impact figure - maximum (currency)

|

|

Select from:

- Virtually certain

- Very likely

- Likely

- More likely than not

- About as likely as not

- Unlikely

- Very unlikely

- Exceptionally unlikely

- Unknown

|

Select from:

- High

- Medium-high

- Medium

- Medium-low

- Low

- Unknown

|

Select from:

- Yes, a single figure estimate

- Yes, an estimated range

- No, we do not have this figure

|

Numerical field [enter a number from 0 to 999,999,999,999,999 using up to 2 decimal places]

|

Numerical field [enter a number from 0 to 999,999,999,999,999 using up to 2 decimal places]

|

Numerical field [enter a number from 0 to 999,999,999,999,999 using up to 2 decimal places]

|

| Explanation of financial impact figure

|

Cost of response to risk

|

Description of response and explanation of cost calculation

|

Comment

|

| Text field [maximum 2,500 characters]

|

Numerical field [enter a number from 0-999,999,999,999,999 using a maximum of 2 decimal places]

|

Text field [maximum 2,500 characters]

|

Text field [maximum 2.500 characters]

|

[Add Row]

Primary climate-related risk driver drop-down options (column 4)

Select one of the following options:

Current regulation

- Carbon pricing mechanisms

- Enhanced emissions-reporting obligations

- Mandates on and regulation of existing products and services

- Regulation and supervision of climate-related risk in the financial sector [Financial services only]

- Other, please specify

Emerging regulation

- Carbon pricing mechanisms

- Enhanced emissions-reporting obligations

- Mandates on and regulation of existing products and services

- Regulation and supervision of climate-related risk in the financial sector [Financial services only]

- Other, please specify

Legal

- Exposure to litigation

- Regulation and supervision of climate-related risk in the financial sector [Financial services only]

- Lending that could create or contribute to systemic risk for the economy [Financial services only]

- Investing that could create or contribute to systemic risk for the economy [Financial services only]

- Insurance underwriting that could create or contribute to systemic risk for the economy [Financial services only]

- Other, please specify

Technology

- Substitution of existing products and services with lower emissions options

- Unsuccessful investment in new technologies

- Transitioning to lower emissions technology

- Other, please specify

|

Market

- Changing customer behavior

- Uncertainty in market signals

- Increased cost of raw materials

- Inability to attract co-financiers and/or investors due to uncertain risks related to the climate [Financial services only]

- Loss of clients due to a fund’s poor environmental performance outcomes (e.g. if a fund has suffered climate-related write-downs) [Financial services only]

- Contraction of insurance markets, leaving clients exposed and changing the risk parameters of the credit [Financial services only]

- Rise in risk-based pricing of insurance policies (beyond demand elasticity) [Financial services only]

- Other, please specify

Reputation

- Shifts in consumer preferences

- Stigmatization of sector

- Increased stakeholder concern or negative stakeholder feedback

- Lending that could create or contribute to systemic risk for the economy [Financial services only]

- Investing that could create or contribute to systemic risk for the economy [Financial services only]

- Insurance underwriting that could create or contribute to systemic risk for the economy [Financial services only]

- Negative press coverage related to support of projects or activities with negative impacts on the climate (e.g. GHG emissions, deforestation, water stress) [Financial services only]

- Other, please specify

Acute physical

- Increased severity and frequency of extreme weather events such as cyclones and floods

- Increased likelihood and severity of wildfires

- Other, please specify

Chronic physical

- Changes in precipitation patterns and extreme variability in weather patterns

- Rising mean temperatures

- Rising sea levels

- Deforestation [Financial services only]

- Water stress [Financial services only]

- Other, please specify

|

Primary potential financial impact drop-down options (column 5)

Select one of the following options:

- Increased direct costs

- Increased indirect (operating) costs

- Increased capital expenditures

- Increased credit risk

- Increased insurance claims liability

- Decreased revenues due to reduced demand for products and services

- Decreased revenues due to reduced production capacity

- Decreased access to capital

- Decreased asset value or asset useful life leading to write-offs, asset impairment or early retirement of existing assets

- Reduced profitability of investment portfolios [Financial services only]

- Devaluation of collateral and potential for stranded, illiquid assets [Financial services only]

- Other, please specify

Requested content

General

- For the purposes of this response, the risks reported should only be those which may pose inherently substantive impacts in your business operations, revenue, or expenditure, regardless of whether or not the company has taken action to mitigate the risk(s).

Identifier (column 1)

- Select a unique identifier from the drop down menu provided to identify the risk in subsequent questions, if required, and to track the status of the risk in subsequent reporting years. Please select from Risk1-Risk100 and use the same identifier in subsequent years for the same risk. For any new risks you are adding, always use a new identifier that you have not used previously.

Where in the value chain does the risk driver occur? (column 2)

- Upstream value chain refers to activities, products and services that are inputs to the activities of your business, sourced from third parties. This may include the regulations and policies applied by governments; the products and services provided by your suppliers (i.e. the supply chain).

- Downstream value chain refers to the third parties benefiting from the outputs, products and services of your business activities. This may be your customers and clients, or the organizations and projects your business invests in.

Note for financial services sector companies:

- Value chain: Upstream and downstream risks should reflect the risks in your customer and/or investment value chain, in addition to your operations. The downstream risks of your value chain relate to the risks for your clients/investee companies, while upstream risks include other transition risks that provide value to your products, services and/or investments e.g. policy and legal, market or technology.

Risk type (column 3)

- See explanation of terms for definitions of risk types.

- Note that a selection must be made for both column 3 and column 4. Your data will not be saved if either column is left blank.

Primary climate-related risk driver (column 4)

- Risk driver describes the source of the risk and will depend on the risk type chosen in column 3. Select an option that best describes the primary risk driver of the identified risk from the drop-down menu.

- Note that a selection must be made for both column 3 and column 4. Your data will not be saved if either column is left blank.

Primary potential financial impact (column 5)

- This column refers to the potential financial impact that the risk could have on your organization. The financial impacts of climate-related issues on organizations are not always clear or direct, and for many organizations there might be more than one financial impact associated with a climate-related risk. Select the option from the drop-down menu that you evaluate as having the biggest impact. You can provide additional details on other financial impacts in the column Explanation of financial impact figure (column 14).

Climate risk type mapped to traditional financial services industry risk classification [Financial services only]

- In this column consider how climate-related risks fit into your already existing organizational framework. Consider where in your traditional industry risk framework you classify the potential financial impact of the climate risk. As per the TCFD supplemental guidance to financial institutions, “Banks should consider characterizing their climate-related risks in the context of traditional banking industry risk categories such as credit risk, market risk, liquidity risk, and operational risk.” If an identified risk maps to multiple risk categories, choose the primary risk category.

Company-specific description (column 6)

- Provide further contextual information on the risk driver, including more detail on the exact nature, location and/or regulation of the effect concerned, as well as any notable geographic/regional examples.

- Be sure to include company-specific detail, such as references to activities, programs, products, services, methodologies, or operating locations specific to your company’s business or operations.

Likelihood (column 8)

- The likelihood of the impact occurring along with the magnitude of the impact are the building blocks of a risk/opportunity matrix – a common method of identifying and prioritizing risk and opportunities.

- The likelihood refers to the probability of the impact to your business occurring within the time horizon provided, which in the case of an inherent risk might be similar to the probability of the climate event itself.

- For example, if the risk relates to a piece of new legislation which has already been prepared in draft form, the likelihood of the impact associated with that risk occurring will be relatively high.

Magnitude of impact (column 9)

- The magnitude describes the extent to which the impact, if it occurred, would affect your business. You should consider the business as a whole and therefore the magnitude can reflect both the damage that may be caused and the exposure to that potential damage.

- For example, two companies may have identical facilities located on a coast in an area which is vulnerable to sea level rise. However, if company A relies on that facility for 90% of its production capacity and company B relies on it for only 40% of its production capacity, the magnitude of a sea level rise impact on company A will be comparatively higher than that on company B.

- It is not possible for CDP to accurately define terms for magnitude as they will vary from company to company. For example, a 1% reduction in profits will have different effects on different companies depending on the profit margins on which they work. Therefore, companies are asked to determine magnitude on a qualitative scale. Factors to consider include:

- The proportion of business units affected;

- The size of the impact on those business units; and

- The potential for shareholder or customer concern.

Are you able to provide a potential financial impact figure? (column 10)

- Your selection will determine whether columns 11,12, and 13 will be presented.

- It is acknowledged that these figures will be estimates.

- If you are unable to provide a figure for a financial impact, you may use column 14 "Explanation of financial impact" to provide a description of the impact in relative terms; for example, as a percentage relative to a stated or publicly available figure, or give a qualitative estimate of the financial impact.

Potential financial impact figure (currency) (column 11)

- Provide a single figure for the inherent financial impact of the risks (before taking into consideration any controls you may have in place to mitigate the impacts). This figure should be in the same currency that you selected in question C0.4 for all financial information disclosed throughout your response.

- An example would be the cost of destruction of facilities from extreme weather (before taking into consideration how much insurance coverage you have).

Potential financial impact figure - minimum/maximum (currency) (columns 12, 13)

- Provide the estimated range for the inherent financial impact (before taking into consideration any controls you may have in place to mitigate the impacts). This figure should be in the same currency that you selected in question C0.4 for all financial information disclosed throughout your response.

- Potential financial impact figure – minimum (currency): Use this field to report the lower point of your estimated financial impact associated with the risk. For example, if the range is from US $5,000 to $50,000, ‘5,000’ should be reported here.

- Potential financial impact figure – maximum (currency): Use this field to report the upper point of your estimated financial impact associated with the risk. For example, if the range is from US $5,000 to $50,000, ‘50,000’ should be reported here.

Explanation of financial impact figure (column 14)

- Use this open text field to explain the figure provided in the “Potential financial impact” (columns 10, 11, 12);

- Describe how you arrived at this figure (or range), including:

- What approach was employed to calculate the figure;

- The figures used in your calculation;

- Any assumption the figure is dependent on.

- If "We do not have this figure" was selected in column 10, use this column to provide a description of the financial impact in relative terms (for example as a percentage relative to a stated or publicly available figure) or give a qualitative estimate of the financial impact. Otherwise, if you have no information about the financial impact, please state “The impact has not been quantified financially”.

- You can also describe here other financial impacts of the selected climate-related risk (other than the main impact identified in column 5), and provide more details on the nature of the impact in case you selected “Other, please specify” in column 5.

Cost of response to risk (column 15)

- Provide a quantitative figure for the cost of your risk response actions. If there are no costs to responding to the risk, enter 0.

- If you cannot provide absolute values, you may provide a percentage value in the “Comment” column (column 17).

- This figure should be in the same currency that you selected in question C0.4 for all financial information disclosed throughout your response.

Description of response and explanation of cost calculation (column 16)

- Provide details of your organization’s response to mitigate, control, transfer or accept the risk.

- Include an example of company-specific risk responses actions (activities, projects, products and/or services).

- Provide an explanation of how the figure for the cost of managing the risk (in column 15) was calculated, including the figures used in your calculation.

Comment (column 17) (optional)

- You can use this text field to enter any additional relevant information.

Note for oil and gas sector companies:

- In answering the questions above, please consider the impact of national and international emissions targets and how those could affect demand for oil and gas products. Will they lead to your company having a less carbon-intensive fuel mix? Will fuel efficiency standards affect the demand for fuel? Are there other instances where demand is likely to reduce due to regulation?

- Is your company affected by other types of regulation such as restrictions on flaring, or by requirements for a certain level of climate-related performance in order to receive permission to operate and/or as a condition of accessing new oil & gas resources? (e.g. a requirement for carbon sequestration).

- Companies are encouraged to include these drivers in the response to this question and explain how their portfolio of reserves is evolving in response to these drivers (in the Comment column).

Note for electric utility sector companies:

- Electric utilities are asked to consider, among other issues:

- How national and international targets on demand management might affect demand for electricity;

- The impacts of related policies such as building regulations specifying more energy-efficient buildings;

- Policies to increase renewable electricity supply or to support developments that may result in GHG emissions reductions, e.g. CO2 capture and storage, clean coal technologies and energy storage;

- The impacts of any emissions trading schemes and any emissions reduction targets you have set or with which you have to comply, including the analysis of possible scenarios and their effect on the company;

- The effects on wholesale and retail power prices of carbon prices in the different markets in which you operate and the extent to which carbon prices are passed through, or may in the future be passed through, into electricity prices in the markets, based on current and anticipated regulatory requirements.

Note for auto and auto component manufacturing companies:

- Please consider the financial and strategic implications of current and planned national, regional, and international policies for increasing automobile fuel efficiency and developing “clean” engines for each of the markets in which you operate. You should also consider how other related environmental policies, such as regulations and standards regarding air quality, use of alternative fuels, and sustainable mobility could further impact your business.

- Specifically, you should take into account how climate change policy could impact you in terms of sales, the financial cost of any loss or potential loss of market share, additional costs of complying with regulation and, if applicable, how you have or will pass increased costs down the value chain.

Note for agricultural sector companies:

- Agricultural companies should report on risks that may affect the revenue associated with the agricultural/forestry, processing/manufacturing and/or distribution. These risk are often driven by:

- Physical factors, e.g. extreme weather events that disrupt production/supply of raw materials.

- Changes in regulation pertaining to agricultural, processing, manufacturing, distribution and/or consumption activities.

- Changes in consumer demands and new market trends

Note for companies with coal reserves:

Note for financial services sector companies:

- For the purposes of this response, the risks reported should be inherent and have the potential for substantive impacts on your investing, financing, underwriting and/or operational activities, regardless of whether any action has been taken to respond to the risk(s).

- Consider providing a description of risks by sector and/or geography, as appropriate. This can be provided in the "Company-specific description" (column 6).

- Both physical and transition risks in your investing, financing, underwriting, and/or operational activities should be considered, including the risk of stranded assets. These are assets that are no longer economically viable as a result of climate-related transition or physical risks.

- Banks:

- Banks should describe significant concentrations of credit exposure to carbon-related assets.

- Additionally, banks should consider disclosing their climate-related risks (transition and physical) in their lending and other financial intermediary business activities.

- Insurance companies should consider climate-related risks on re-/insurance portfolios by geography, business division, or product segments, including the following risks:

- Physical risks from changing frequencies and intensities of weather-related perils;

- Transition risks resulting from a reduction in insurable interest due to a decline in value, changing energy costs, or implementation of carbon regulation; and

- Liability risks that could intensify due to a possible increase in litigation. For example, the risk of an increase in claims for defense costs in relation to directors and officers (D&O) liability.

- Additionally, as an asset owner, please also describe the climate-related risks relevant to your investment portfolio.

- Asset managers should consider climate-related risks for each product or investment strategy.

Note for real estate companies:

- Since real estate is a location-bound and a long-term investment, it is highly exposed to climate-related risks. Commercial real

estate companies should consider stranding risks - the devaluation or

non-performance of assets, thus making them ‘stranded’.

- Stranded assets may be subject to write-downs due to:

- Demand shifts towards sustainable properties, putting pressure on ‘non-green’ assets;

- Higher exposure to acute physical risks (storms, flooding, wildfires, etc.);

Notes for capital goods sector companies:

- All the end markets supplied to by the capital goods sector face increasing regulation and decarbonization targets; from building standards to mandated technologies for power generation. Companies in this sector are therefore indirectly exposed to risks in their value chain, and should consider, among other issues, risks associated with: