CDP Water Security Questionnaire Preview and Reporting Guidance 2018 - Version Control

Version control table will be updated weekly, so on Monday you can view all updates relevant to the previous week.

| Version number

|

Release/Revision date

|

Revision summary

|

| 0.1

|

Released: Dec 13, 2017

|

Questionnaire preview

This version was released to allow CDP stakeholders to see the 2018 water security questionnaire, including sector-specific requests for CDP’s high-impact sectors, ahead of the information request sent in February 2018.

|

| 0.2

|

Revised: Feb 7, 2018

|

Questionnaire preview

The following sections were updated for 2018:

- Important Information

- Terms for responding to Investors (2018 Water Security)

- Terms for responding to Supply Chain Members (2018 Water Security)

|

| 0.3

|

Revised: Jan - Mar 2018

|

Questionnaire preview

The following revisions were made to the water security questions:

General questions

- Facility accounting: W5.1b (discharge destinations). Columns merged to match the discharge destination options for the corporate level disclosure.

- Facility accounting: W5.1c (recycling). Column deleted and question wording modified; to reduce reporting effort we no longer request volumes recycled/reused for facilities at risk.

All high-impact sectors

- Incentives for senior management: W-FB6.4a/W-CH6.4a/W-EU6.4a/W-OG6.4a/W-MM6.4a. Drop-down options modified (column 3 – from ‘Efficiency project or target – downstream‘ to ‘Efficiency project or target – downstream in the value chain’ and ‘Efficiency project or target – upstream’ to ‘Efficiency project or target – upstream in the value chain’). Drop-down option deleted (‘No indicator for incentivized performance’).

Chemicals sector

- Water intensity: W-CH1.3a. Header modified (column 3). Drop-down options deleted (column 1 ‘No potential water pollutants identified’ and column 5 - ‘Not applicable’).

- Potential water pollutants: W-CH3.1a. Drop-down option deleted (column 2 - ‘Does not apply’).

Food, beverage & tobacco sector

- Dependency on water intensive crops: W-FB1.1a. Drop-down options deleted (column 1 - ‘None’, column 2 - ‘Not relevant’ and ‘Don´t know’).

- Produced/sourced from stressed areas: W-FB1.2e. Drop-down option added (column 1 - from ‘Other commodities from W-FB1.1a, please specify’); W-FB1.2f. Question text corrected. Drop-down option added (column 1 – ‘Other produced commodities from W-1.2e, please specify’); W-FB1.2g. Drop-down option added (column 1 - ‘Other sourced commodities from W-1.2e, please specify’).

- Water intensity: W-FB1.3. Drop-down option added (column 1 - ‘Other commodities from W-FB1.1a, please specify); W-FB1.3a. Headers modified (columns 2 and 5). Drop-down option added (column 1 ‘Other produced commodities from W-1.3, please specify’); W-FB1.3b. Headers modified (columns 3, 4 and 5). Drop-down option added (column 1 - ‘Other sourced commodities from W-1.3, please specify’).

- Sector-specific drop-down options modified for: Business impacts W-2.1 (columns 5 and 7); Water risks and responses W4.2 and W4.2a; Corporate water targets W8.1a; Linkages and trade offs W9.1a.

Metals & mining sector

- Water recycling & reuse: W-MM1.2j. Column 2 - modified from numerical field to selection of intervals Drop down option deleted (column 3 - ‘Not applicable’).

- Tailings dams management procedures: W-MM3.2. Drop-down option added (column 1 - ‘Other, please specify’) and drop-down option modified (column 1 - from ‘Country drop-down list’ to ‘Organization-specific country list’); W-MM3.2a. Drop-down options deleted (column 2).

- Sector-specific drop-down option added for: Business impacts W2.1a (column 4); Water risks and responses W4.2 (column 4) and W4.2a (column 5).

Electric utilities sector

- Monitoring water aspects in hydroelectric operations: W-EU1.2a. Response options modified (column 2 - modified from numerical field to selection of intervals).

- Facility accounting: W5.1 Drop-down option added (column 7 - ‘Other non-renewable’)

Oil & gas sector

- Water volumes by business division: W-OG1.2c. Merged columns (‘Water aspect’ & ‘Business division’ into column 1 - ‘Water aspect by business division’). Column header modified (column 4 - from ‘Comment’ to ‘Please explain’).

- Water recycling & reuse: W-OG1.2j. Question wording modified from “What proportion of water do you recycle…” to “What proportion of your total water use do you recycle…”. Column 2 - modified from numerical field to selection of intervals Drop down option deleted (column 3 - ‘Not applicable’).

- Water intensity: W-OG1.3a. Response option modified (column 1 from ‘Select from’ to ‘Select all that apply’).

- Management procedures for potential water pollutants: W-3.1a. Header modified (column 6 - from ‘Description of response’ to ‘Please explain’). Drop-down options added (column 4 – ‘No formal management procedure in place’ and ‘Management procedure under development’).

|

| 0.4

|

Revised: Mar 28, 2018

|

Questionnaire preview, Reporting guidance

The following details were released, to assist companies in preparing their disclosures:

- Question ‘Rationales’ and ‘Requested content’ for all general water security questions

- ‘Preparing and submitting your CDP response’ section

|

| 0.5

|

Revised: Apr 5, 2018

|

Questionnaire preview, Reporting guidance

The following sections were added:

- 'Version control – water security’

- ‘Introduction to CDP water security reporting guidance’

- 'Appendix: River basin list'

Reporting guidance

The following details were added to assist companies in preparing their disclosures:

- Question ‘Rationales’ and ‘Requested content’ for all sector-specific water security questions

- ‘Pathway diagrams’ for all general water security questions

|

| 0.6

|

Revised: Apr 9, 2018

|

Questionnaire preview, Reporting guidance

The following revisions were made to the water security questions:

General questions

- Facility-level water accounting: W5.1 and W5.1a-c. Changed to 'Add Row' tables.

Food, beverage & tobacco sector

- Dependency on water intensive crops: W-FB1.1a. Drop-down options deleted

Reporting guidance

The following changes were made to the 'Requested content' section:

- Dependence: W1.1. Added clarification around the definition of 'good quality freshwater' (Requested content, General).

- Facility-level water accounting: W5.1 and W5.1a-c. Changed guidance for companies exporting their response from the ORS to a spreadsheet (Requested content, General)

|

| 0.7

|

Revised: Apr 13, 2018

|

Reporting guidance

The following change was made to the 'Requested content' section:

|

| 0.8

|

Revised: Apr 20, 2018

|

Questionnaire preview, Reporting guidance

The following details were released, to assist companies in mapping their CDP responses to other frameworks:

- Connections to other frameworks, including the Sustainable Development Goals (SDGs) and CEO Water Mandate.

The following changes were made to the ‘Response options’ section:

- Risks and opportunities: W4.2 and W4.2a. ‘All countries in which we operate’ removed from the list of countries.

The following changes were made to the 'Question dependencies' section:

General questions

- Company-wide water accounting: W1.2b. Corrected the route from W1.1.

- Value chain engagement: W1.4d. Corrected the route from W1.4.

Oil & gas sector

- Company-wide water accounting: W-OG1.2c. Corrected the route from W1.1.

Electric utilities sector

- Water intensity: W-EU1.3. Corrected the route from W-EU0.1a.

Chemicals sector

- Water intensity: W-CH1.3. Corrected the route from previous questions.

The following change was made to the 'minimum version' of the 2018 Water Security Questionnaire:

- Risks and opportunities: W4.1c. This question was added to the ‘minimum version’.

|

| 0.9

|

Revised: Apr 27, 2018

|

Questionnaire preview, Reporting guidance

The following changes were made to the ‘Response options’ section:

Food, beverage & tobacco sector

- Produced/sourced from stressed areas: W-FB1.2f-g. Reworded drop-down options in column 1.

- Water intensity: W-FB1.3a-b. Reworded drop-down options in column 1.

The following changes were made to the 'Question dependencies' section:

General questions

- Compliance impacts: W2.2b. 'Question dependencies' corrected to reflect the 'Response options' presented in W2.2.

Food, beverage & tobacco sector

- Produced/sourced from stressed areas: W-FB1.2f-g. 'Question dependencies' revised.

- Water intensity: W-FB1.3a-b. 'Question dependencies' revised.

The following change was made to the 'minimum version' of the 2018 Water Security Questionnaire:

- Country: W0.3. This question was added to the 'minimum tier' version.

Reporting guidance

The following change was made to the 'Requested content' section:

- Value chain engagement: W1.2b. Corrected guidance for column 5 which refers to columns 3 and 4.

|

| 1.0

|

May 4, 2018

|

Questionnaire preview, Reporting guidance

The following change was made to the ‘Response options’ section:

- Water policy: W6.1a. Table was changed from 'Add Row' to fixed row.

The following changes were made to the ‘Question dependencies’ section:

- Country: W0.3. Removed 'Question dependencies'

section.

- Water-related risks and response: W4.2a. Corrected route from W4.1.

Reporting guidance

The following was released, to provide an overview

of each module, as well as key changes, questions with "copy from last

year" functionality in the ORS, sector modifications, and important

disclosure notes:

The following changes were made to the ‘Requested content’ section:

General

questions

- Water recycling & reuse: W-1.2j. The

following text was added. ‘…of water used in your operations. This can be

calculated as the sum…’ and ‘(minus any sent to storage)'.

Electric

utilities sector

- Monitoring hydroelectric operations: W-EU1.2a. The following text was deleted: ‘Please provide a label for the water aspect in

the text field provided. If you need more than 40 characters, please use the

comment box by clicking on the “speech bubble” icon.'

Oil & gas sector

- Recycling & reuse: W-OG1.2j. The following

text was added: 'business division' in column 1.

Food, beverage, &

tobacco sector

- Produced from stressed areas: W-FB1.2f. Column 3:

character limit changed from 1,000 to 1,500.

|

| 1.1

|

May 18, 2018

|

Questionnaire preview, Reporting guidance

Disclosure deadlines were updated in the 'CDP disclosure cycle 2018' section.

The following changes were made to the ‘Question text’ section:

Oil & gas sector

- Potential water pollutants: W-CH3.1a. The question text was corrected.

The following changes were made to the ‘Response options’ section:

General questions

- Impacts section: W2.1a. Added sector-specific drop-down options in column 7 ('Primary response') for food, beverage, & tobacco sector.

- Company-wide water accounting: W1.2j. Added ’76-99’ to the list of percentages in column 1 ('% recycled or reused').

- Facility-level water accounting: W5.1c. Added ’76-99’ to the list of percentages in column 3 ('% recycled or reused').

- Risk identification and assessment: W3.3a. Removed 'Water risks are not assessed at this stage of the value chain' from column 3 ('Risk assessment procedure').

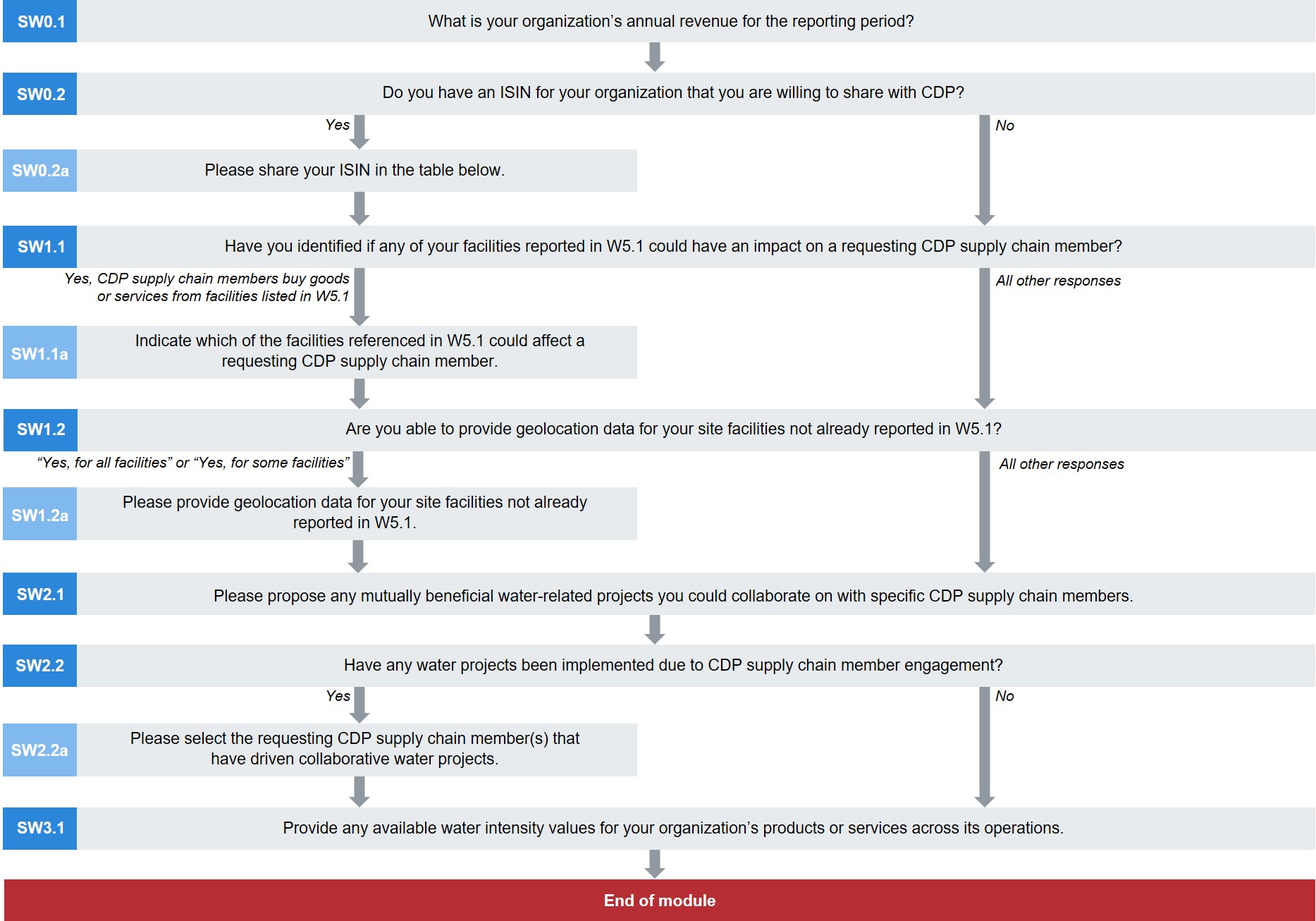

- Facility details: SW1.2a. Changed column 1 to a text field with the heading: ‘Identifier’.

Food, beverage & tobacco sector

- Water intensity: W-FB1.3a and W-FB1.3b. The headers from columns 4 and 5 respectively have been changed from to “Comparison with previous reporting year”.

Metals & mining sector

- Water reuse & recycling: W-MM1.2j. The response options were corrected.

The following changes were made to the ‘question dependencies’ section:

- Facility details: SW1.1a. Clarified the route from SW1.1.

Reporting guidance

The following details were released, to assist companies in preparing their disclosures:

- ‘Example responses’ for select questions.

- ‘Explanation of terms’, or detailed definitions for specific terminology, for select questions.

- A ‘Glossary’, consisting of a subset of ‘Explanation of terms’.

The following changes were made to the ‘Requested content’ section:

- Company-wide water accounting: W1.2h-i. New guidance for column 2 (‘Relevance’) and column 4 (‘Comparison from last year’).

Chemicals sector

- Water intensity: W-CH1.3a. The guidance was corrected.

|

| 1.2

|

Revised: May 25, 2018

|

Questionnaire preview, Reporting guidance

The following sections were updated:

- ‘Terms for responding to Investors (2018 Water Security)’

- ‘Terms for responding to Supply Chain Members (2018 Water Security)’

- ‘CDP disclosure cycle 2018’: details on the full and minimum versions of the questionnaire were added

Reporting guidance

The following sections were updated:

- ‘Preparing and submitting your CDP response’: details were added under Reporting guidance, Notes for completing your disclosure, and Submitting your response through CDP’s online response system (ORS)

- References to ‘Copy from last year’ were removed throughout the reporting guidance as this feature will not be available until 2019

The following details were released, to assist companies in preparing their disclosures:

General questions

- ‘Example responses’ for questions: W0.6a; W3.3c; W4.2; W5.1; W9.1a; SW0.2a.

- 'Additional information' for questions: W0.5; SW0.2; SW1.2a; SW2.1; SW2.2a; SW3.1.

Chemical sector

- ‘Example responses’ for questions: W-CH3.1; W-CH3.1a.

Electric utilities sector

- ‘Example responses’ for questions: W1.2; W1.2b.

Food, beverage & tobacco sector

- ‘Example responses’ for questions: W-FB1.3; W-FB1.3a; W-FB1.3b.

Metals & mining sector

- ‘Example responses’ for questions: W-MM3.2; W-MM3.2a.

Revisions were made to the ‘Requested content’ section to clarify that the potential financial impact figure could also be a range.

|

| 1.3

|

Revised: Jun 1, 2018

|

Version Control

The following revision summary was added to this table for version 1.0:

The following change was made to the ‘Response options’ section:

- Water policy: W6.1a. Table was changed from 'Add Row' to fixed row.

|

| 1.4

|

Revised: Jun 15, 2018

|

Reporting guidance

The following changes were made to the 'Question pathway - questions' section:

- Dependence: W1.1: The diagram was corrected to reflect the changes made to the 'Question dependencies' section in version 0.8.

- Facility level water accounting: W5.1: Corrected the question text for W5.1 to refer to W4.1c.

The following changes were made to the 'Requested content' section:

Metals & mining sector:

- Company wide water accounting: W1.2: the subject of the 'Water consumption' definition was corrected.

|

| 1.5

|

Revised: Jun 22, 2018

|

Questionnaire preview, Reporting guidance

The following change was made to the 'minimum version' of the 2018 Water Security questionnaire:

Metals & mining sector:

- Introduction: W-EU0.1a: Removed from the 'minimum version.

|

| 1.6

|

Revised: Jul 27, 2018

|

Reporting guidance

The following change was made to the introduction to the reporting guidance:

- Preparing and submitting your response: Updates regarding the Export/Import functionality in the ORS were added.

|

| 1.7

|

Revised: Aug 10, 2018

|

Questionnaire preview, Reporting guidance

The following details were added to the "Response options" section:

- W3.3e: Water-related risk assessment:

Note: The drop-down list presented in the ORS is missing two options.

'We are planning to introduce a risk assessment process within the next two years’, is incorrectly authored as ‘Water risk assessment in progress’. Companies wishing to respond with that option should select ‘Water risk assessment in progress’ and use the Please explain column to provide the information requested. (Scoring for the selection of this option will be as set out in the Scoring Methodology for the option ‘We are planning to introduce a risk assessment process within the next two years’).

‘Insufficient data on operations’ is missing. Companies wishing to respond with that option should select ‘Other, please specify’. (There are no scoring implications).

|

CDP disclosure cycle 2018

New for 2018: In response to market needs, CDP has developed questions specific to high-impact sector activities across its climate change, forests and water security programs. The 2018 questionnaires also include more forward-looking metrics, are further harmonized with other reporting frameworks, and include TCFD recommendations for climate-related disclosure.

Accessing questionnaire previews, reporting guidance, and scoring methodologies

CDP’s 2018 corporate questionnaire previews, reporting guidance, and scoring methodologies can be accessed by program (climate change, forests, and water security) from the guidance for companies page of CDP's website. You will be presented with three prompt screens that allow you to select the sectors and other details relevant to your organization. Questionnaires are valid for information requests from investors, as well as from customers that are members of CDP’s supply chain program. As there are sector-specific questions throughout the questionnaires, you might find that question numbers skip since not all questions will be applicable to your organization.

Responses to questionnaires are submitted via CDP's online response system (ORS), which is part of CDP's online disclosure platform. Please refer to Using CDP's Online Disclosure Platform for more detail. Note that while the questions themselves are the same in the questionnaire preview as they are in the ORS, the format may differ, particularly for drop-down options and tables.

Full and Minimum versions of the questionnaire

For all CDP questionnaires, there are two versions: minimum and full. The minimum version contains identical but fewer questions, and no sector-specific questions or data points.

- The minimum version of a questionnaire can by completed by:

- Organizations disclosing to that questionnaire for the first time; OR

- Organizations who are not disclosing to that questionnaire for the first time, but who have an annual revenue of less than EUR/US$250 million

- For previous responders with an annual revenue of less than EUR/US$250 million, CDP reserves the right to remove the option of a minimum version questionnaire due to the organization’s potential or existing environmental impact.

- Companies with an annual revenue of over EUR/US$250million that are disclosing for the first time and responding to the minimum version will not be eligible for scoring.

- Companies responding to the minimum version that have an annual revenue of less than EUR/US$250million will be eligible for scoring and will be scored using the minimum version of the methodology. They will not be eligible for the A list as the scores are not

comparable to scores resulting from the full version of the scoring methodology.

Note that companies eligible to complete the minimum version of a questionnaire can choose to answer the full version if they consider this to provide greater benefit to their organization or stakeholders. For more information on scoring eligibility and implications, please see Scoring Introduction 2018.

Timeline:

January

|

- Options to export content from this online preview into Word or PDF made available.

|

| February

|

- Organizations notified of the specific sector and program questionnaire(s) they need to complete for requesting investors.

- Comprehensive details of changes to the CDP questionnaires from 2017 to 2018 shared.

|

| March

|

- Guidance and information on scoring methodologies made available.

|

| April

|

- Some organizations will be asked to provide additional information to their customers that are members of CDP’s supply chain program.

|

| May

|

- Access will be provided to CDP’s new disclosure platform.

|

| August

|

- Responses to investor requests must be submitted by August 15, 2018 to be automatically eligible for scoring and inclusion in CDP reports (where applicable).

- Responses to supply chain requests must be submitted by August 29, 2018.

|

For any disclosure-related questions, please contact [email protected].

CDP water security questionnaire

CDP’s water security program and water security questionnaires

CDP’s water security program works to catalyze action to improve water security across the globe by collecting information for investors, customer and policy makers on a company’s management, governance, use and stewardship of water resources.

The CDP water security questionnaire provides data users and the companies themselves with an insight on current and future water-related risks and opportunities. Along with CDP’s water scoring methodology, the water security questionnaire helps companies to drive improvements in water management and enables benchmarking against leading practice.

The water security program has grown significantly since it was established in 2010, in terms of the numbers of companies disclosing, the value of associated assets and the number of investors and customers requesting the data. CDP now holds the world’s largest corporate water dataset, with more companies reporting than ever before. In 2017, 2,025 companies worth approximately US$20 trillion in market capitalization disclosed through us.

Commit to Action

CDP and its partners in the We Mean Business coalition have created a central platform for companies to take action on key climate issues. Hundreds of companies representing every economic sector and geography have taken action to date.

The leadership these companies demonstrated formed a critical part of the package of solutions reached in Paris at COP21 in 2015 and has continued to grow, now playing a critical role as the Paris Agreement moves from agreement to implementation. The We Mean Business “Take Action” platform gives companies a clear pathway for building the Paris Agreement into their business strategies and to future-proof growth, sending a strong signal that companies are making the transition to a low-carbon world and giving policy makers the confidence in raising their ambitions as governments prepare to ratchet up their national pledges in 2020.

One initiative companies can commit to on the We Mean Business platform is to improve water security. This commitment can be tracked in CDP’s water security questionnaire:

- Overview: We Mean Business and the Business Alliance for

Water and Climate invite companies to commit to taking a specific set of

actions around water use measurement, management, and reporting to ensure they

are following best practice on corporate water stewardship.

- Reporting: Companies can report progress against this

commitment in the following questions:

- Analyzing water-related risks (W3.3a, W3.3b, W3.3c) and implementing collaborative response strategies (W1.4a, W4.1b, W4.2a, W4.3, W8.1, W8.1b);

- Measuring and reporting water use data (W1.2b, W1.2h, W1.2i, W8.1); and

- Reducing impacts on water availability and quality in direct operations and along the value chain (W1.4a, W8.1, W4.2, W4.2a, W4.3a)

General water security questionnaire structure

The structure of the water security questionnaire was revised in 2014 to improve alignment with the CEO Mandate Water Guidelines and has been stable since then.

From 2018, revisions to the questionnaire structure and content reflect trends in corporate water reporting, the evolving needs of water data users, developments in public policy agendas, greater alignment with CDP’s climate change and forests questionnaires, and CDP’s move to sector questionnaires.

The modular structure still broadly reflects the narrative of the CEO Water Mandate Guidelines, assisting companies on a water stewardship journey. However, there are revised module and section headings, and some sections and questions have moved position. There are new and revised modules, sections and questions to improve the discloser's experience and provide more robust and relevant data.

There are 11 water modules, including the Signoff, plus a module presented only to organizations that supply goods or services to the member companies of CDP’s supply chain program.

The journey through CDP’s general water questionnaire includes the following:

- water dependence and water accounting metrics

- value chain engagement activities

- business impacts

- risk assessment procedures

- risks, opportunities and responses to them

- facility water accounting

- water governance and business strategy

- targets and environmental linkages

General water security questionnaire developments

A detailed document on water security question changes from 2017 to 2018 is now available. Revisions and changes to questions are also indicated by “Change from 2017” as: no change, minor change, modification, or new question. Minor changes indicate wording edits and revisions to drop-down options, while a modification indicates where a new or revised data point has been added or removed from an existing question.

The main substantive changes to the water questionnaire include:

| Forward-looking focus

and financial information

|

- Data points throughout reflect CDP’s move to more forward-looking disclosure, and CDP data users’ need for more financial information on the impacts of water-related risks and opportunities.

|

| From supply chain to

value chain

|

- The scope of questions that previously asked about dependency, water management or water risks in the supply chain now include all phases of the value chain. This is in recognition that water availability or quality downstream of direct operations (in product use, for example) as well as upstream is increasingly an issue for many companies.

|

| Water accounting

|

- Companies

are asked to indicate the percentage of withdrawals from stressed basins,

reflecting a move towards more context-based water reporting,

- In

recognition of the SDGs and the trend in corporate water management, a question

has been included on the recycling and reuse of water.

|

| Risk disclosure

tables:

|

- The

tables for disclosing risks have been extended and clarified. Information is requested

about potential impacts to the business arising from risk drivers either within

direct operations or elsewhere in the value chain (and no longer simply the

supply chain). Companies are requested to provide a numerical financial value

for the potential impact.

|

| Facility level data

|

- Geolocation

data is requested for facilities exposed to risks that could generate a

substantive change to the business.

|

| Governance

|

- Revised

and new data points, on oversight and public policy influence, allow companies

to show how water matters are considered as part of corporate governance

mechanisms.

|

| Strategy

|

- A

section on strategy asks companies to disclose how water has been integrated

into long-term strategic business plans (including their use of scenario

analysis and water pricing).

|

| Targets and goals

|

- Companies

are asked about their approach to setting targets and goals at any level of the

organization. Details are requested only for targets and goals that are

monitored at the corporate level.

|

Sector approach

- From 2018, companies in high-impact sectors for water will be presented with sector specific requests for information, either in addition to or instead of the general water data points.

- The rationale for developing a refined questionnaire for each of these sectors is outlined in each sector introduction.

- Questions that are unique to companies in a particular sector are labeled using a two-letter abbreviation within the question number (see below). Some general water questions, beginning with the letter W, may include sector-specific data requests. In the disclosure platform these will be presented only to companies in the relevant sector.

2018 water sectors:

- Agriculture: Food, beverage & tobacco (FB)

- Energy: Electric utilities (EU); Oil & gas (OG)

- Materials: Chemicals (CH); Metals & mining (MM)

Preparing and submitting your CDP response

Correction: The ability to import data into the ORS will not be available for the 2018 reporting cycle. The CDP reporting guidance refers to this ability but we ask that you disregard these instructions. We apologize for the inconvenience caused. The questions affected are: W0.2, W5.1, W5.1a, W5.1b, W5.1c, SW1.1, SW1.1a, and SW1.2a.

CDP disclosure support

Reporting guidance

CDP reporting guidance includes the following sections. Please be sure to review the guidance for all questions to which you are submitting a response, even if you have previously disclosed to CDP.

- Module-level guidance: for select modules this guidance provides an overview, key changes, sector-specific modifications for the module, and important disclosure notes. This section also presents question pathway diagrams showing the flow of questions through each module.

- Question-level guidance: at the question level, guidance is separated into the following components, to provide clarity around questions, terminology and requirements.

- Rationale: provides reasoning behind the inclusion of each question;

- Connections to other frameworks: notes linkages to the SDGs and The CEO Water Mandate for each relevant question in the water security questionnaire;

- Requested content: offers context around each question and requested criteria;

- Explanation of terms: provides detailed definitions for specific terminology;

- Example responses: forthcoming by May 31 for select questions; and

- Additional information: forthcoming by May 31 for select questions

- Glossary: viewable at the end of the reporting guidance, the glossary contains a subset of "Explanation of terms"

- Appendix: River basin list — and South African Water Management Areas — by country

If you have any questions that are not answered in the reporting guidance, or the additional guidance noted below, please contact your local CDP office or [email protected].

Additional CDP guidance

Links to CDP questionnaires, guidance, scoring methodologies, and select technical notes can be found on the guidance for companies page of CDP's website. The full suite of these materials will also be accessible from the guidance tool, after signing in.

Webinars and workshops

CDP is hosting a series of events through May, online and in person, to help companies with their disclosure in 2018. Visit the workshops and webinars and water security pages of CDP's website for more details.

CDP reporter services

CDP reporter services offers tailored support, enhanced data access and thought leadership on managing and reporting environmental risk to your business. Access the tools you need to move from disclosure to leadership on integrating climate, water security and forests management into your wider business strategy. For year-round, personalized disclosure support from a CDP account manager, a gap analysis of your previous response, and analytics tools to benchmark yourself against peers and understand best practice, contact [email protected] and visit the reporter services page of CDP's website for more information.

CDP water consultancy solutions providers

CDP accredited water consultancy solutions providers support companies looking to engage with and improve their water management. Partners are subject to strict selection criteria and once approved are able to work closely with companies to provide expertise on critical topics including: water accounting, water risk assessment, the development of water strategies and development and implementation of corporate water stewardship plans. Visit the accredited solutions providers page of CDP's website or contact [email protected] to learn more.

Notes for completing your disclosure

Acronyms

Avoid using bespoke internal acronyms unless required for your organization’s response, in which case please provide their meaning to enable correct analysis and scoring.

Blank responses

Leaving a response blank is interpreted as non-disclosure. For numeric fields, values of zero (0) imply a measurement has been made, and the value is zero (0). For numeric fields where no measurement has been made, please leave the field blank and provide an explanation in an open text field for that same question (e.g. 'Comment' or 'Please explain'). If there is no open text field for the question, you may provide an explanation in the 'Further information' field in the online response system (ORS) at the end of your disclosure. Leaving a response blank and entering a value of zero (0) have different scoring implications. Please see the scoring methodology for more details.

Character limits

Limits noted in the guidance and the online response system (ORS) include spaces.

Company-specific information

Some questions request company-specific information. Be sure to include company-specific detail, such as references to activities, programs, products, services, methodologies, or operating locations specific to your company’s business or operations. A company-specific explanation should include details that make the answer true for the responding company and are distinct from other companies in the same industry and/or geography. This level of detail gives data users confidence that the issue at hand has been thoroughly considered in the context of the responder’s own business and not simply assessed in general terms.

Consistency

CDP encourages a comprehensive and consistent response. Please ensure there is no conflicting information in your responses, both within a question and across the questionnaire.

Drop-down options ('Other, please specify')

Please select from the categories provided whenever possible, and only select 'Other, please specify' when none of the listed options is appropriate. This greatly assists data analysis.

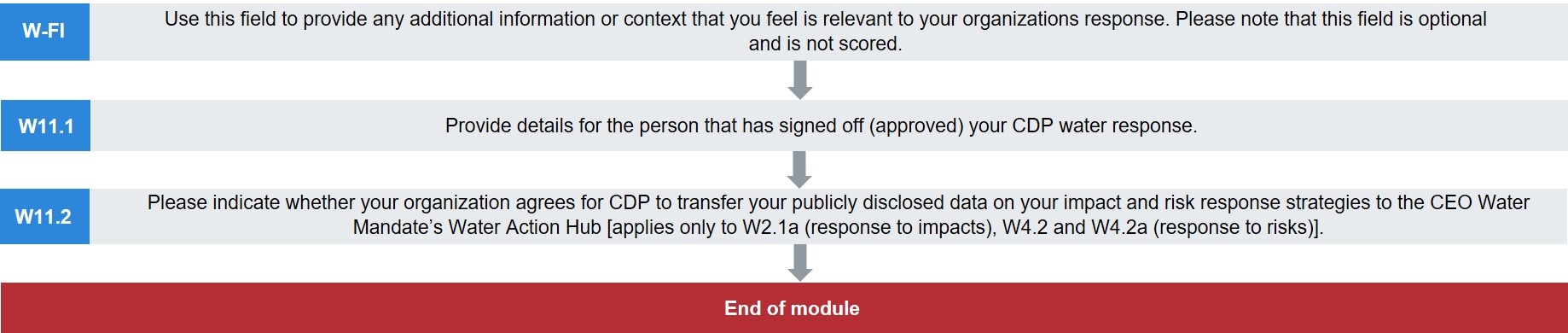

'Further information' field

At the end of the questionnaire, there is an opportunity to provide additional information or context that you feel is relevant to your organization’s response. This field is optional and not scored.

Personal data

It is important that you do not include the name of any individual or any other personal data in your response. For questions that ask for the positions of staff, out of respect for personal data privacy we are asking only for the position and not for the individual’s name or any other information relating to them.

Submitting your response through CDP's online response system (ORS)

Please refer to Using CDP's Online Disclosure Platform for more details.

Introduction to CDP water security reporting guidance

Water reporting

Water presents a unique set of measurement and reporting challenges on both the local and global scales.

- First and foremost, water management is a local or regional issue. Local contexts matter. Challenges and opportunities depend on patterns of local precipitation, watersheds and aquifers, as well as the degree and nature of local use, and the extent and efficacy of water governance and regulation. Unlike a ton of carbon dioxide that will have the same impact whether emitted in Stockholm or Sydney, the geographical scale, location and timing of water use is critical. A cubic meter of water used in Sydney has very different consequences from a cubic meter used in Stockholm. This creates complexities in managing water use in a way that progresses water security for all, as well as in creating meaningful corporate water indicators.

- Standards for water reporting are not yet as consistently or universally established as those for GHG emissions.

- While GHG emissions which can be expressed in tons of CO2e, there is no single or interchangeable quantitative unit of measurement for tracking the risks and impacts associated with water. Factors that must be considered include available volumes, water quality, the degree of competition in the region concerned, as well as future scenarios for physical, regulatory, market and technological changes.

- Compounding this complexity, the global nature of business and supply chains mean that water use is linked across multiple geographies. Even when their own operations or assets are not affected, many businesses may be exposed to and significantly affected by changing patterns of water availability. For large companies with complex supply chains containing potentially thousands of suppliers, assessing water use and related product or supply chain issues can be highly complex.

CDP’s approach to water reporting

Alignment

To support the development of standards that are both valuable for companies and provide investors, policy makers and other data-users with meaningful information, CDP works with a range of organizations; such as the CEO Water Mandate, the World Resources Institute, WWF, World Business Council for Sustainable Development, the Global Reporting Initiative, the Alliance for Water Stewardship, Ceres, Sustainability Accounting Standards Board (SASB) and similar organizations. Standardization is needed to facilitate transparency and reporting as well as to support consistency and comparability for data users.

CDP’s water security request and our reporting guidance draw on reporting principles, frameworks definitions and standards from these and other organizations and align wherever possible. Where differences remain, they reflect each organization’s particular approach and aims.

Note on 2018 alignment with the GRI standards: GRI 303: Water is under review and publication of the new standard is planned for May 2018. CDP’s 2018 water security questionnaire incorporates some changes anticipated for the GRI standard, but due to differing timelines it has not been possible to assess and review alignment at this stage. In 2017, we published a document setting out the linkages with GRI 303 and GRI 306, but this is not valid for CDP’s 2018 questionnaire. CDP will review the new GRI standard after publication, and wherever feasible may consider revisions to our questions and guidance for our 2019 disclosure.

For CDP’s 2018 disclosure cycle, companies must consult our revised question-level reporting guidance when responding to our water security questionnaire as the guidance has been updated.

Journey to water security

Our water security questionnaire is structured from start to finish as framework to assist organizations to progress the maturity of their water management and corporate reporting. It presents a journey to water stewardship and water security.

Collecting and disclosing information on management and governance responses to risk and opportunities, as well as the integration of water into long term strategic objectives, provides data for decision making and catalyzes corporate action. This is the value of disclosure.

Accounting

To progress water security for all and to minimize water-related risks, organizations must eliminate any detrimental impact on water ecosystems and resources. Impact and risk exposure occurs as water flows into and out of a company’s boundaries, so CDP’s collects information to determine how well a company understands this flow. Companies are encouraged to account for all their interaction with water, and to minimize that interaction (e.g. through reduced withdrawals, efficiency improvements, or by changing their business activities). This means that CDP seeks more nuanced information than volumetric reductions in freshwater removal or consumption. Most important is that companies have robust monitoring and accounting in place for all aspects of their corporate hydrology, and that they demonstrate an understanding of their dependence on water.

Measurements of withdrawal, discharge and consumption take place as water crosses the company boundary, at either the corporate level or facility level. This makes the concept of the organizational boundary central to our disclosure request at the corporate and the facility level.

Context and geographic scale

Water presents local issues which need to be understood and managed at a local level; typically at river basin, or at least a country level, rather than the corporate level. Investors are increasingly interested in this type of granularity when it comes to assessing the water risk within their portfolios.

Some CDP data users wish to asses an organization’s ability to access the granular data needed for mature water management and sound risk management across all its operations and locations. This is deemed to be best practice. A separate module (W5) requests water accounting data for any facilities exposing the company to substantive water-related risk (note that we do not ask for data for all facilities).

In addition, CDP invites companies to report their risks at the river basin level and several questions include a column so that companies can indicate the location associated with their data. An organization will not have a comprehensive understanding of its risk exposure and the most appropriate response unless it is able to take account of local basin context and conditions. River basin level risk assessment is particularly relevant to a water stewardship approach to securing water resources as collaboration with other basin users and external stakeholders is central to understanding and managing risk.

Building on this, CDP is partnering in a multi-organization initiative to provide companies with guidance on setting context-based water targets (see Exploring the case for context based water targets, April 2017).

Reporting risk

CDP provides its data users with information about the inherent risks faced by companies. This allows them to independently assess the appropriateness and adequacy of the management and governance response, and thus the residual risk and resilience of the business.

To provide data users with confidence in their disclosure, companies are encouraged to give a full picture of their approach to risk assessment and how water-related issues have been integrated into their business strategy.

Reporting impacts

When referring to ‘impacts’, some frameworks and standards use the term to mean the effects of a business on communities and ecosystems, such as the CEO Water Mandate Guidelines and the GRI standards. For CDP, this term refers to the effects of water challenges on the business, i.e. ‘business impacts’, be they due to physical, regulatory or market drivers.

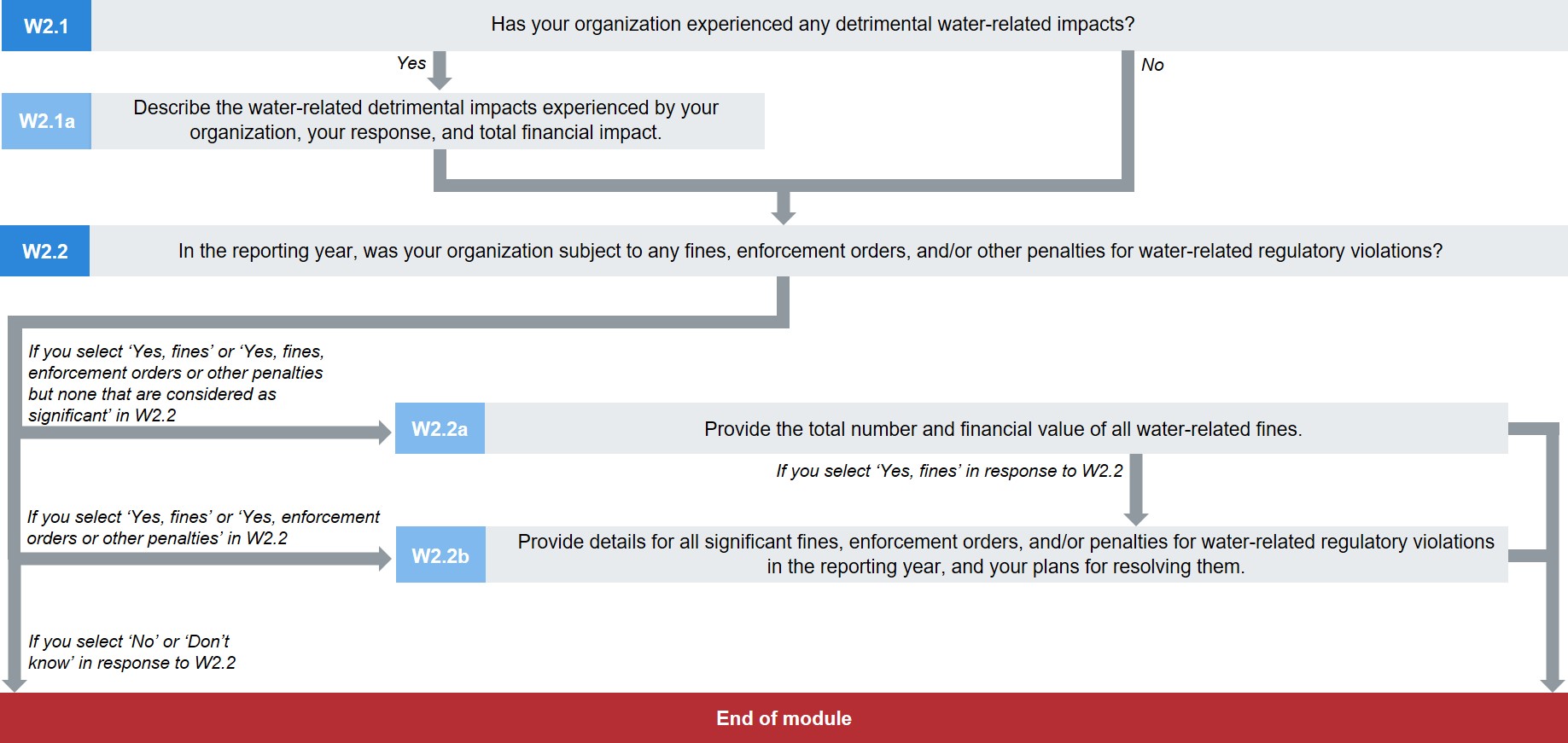

CDP asks for information about past water-related impacts on the business and responses to them (in module W1 ‘Current State’). Data users may judge a company’s potential future performance using this data.

Principles of true and fair reporting

The GHG Protocol outlines five principles to ensure a true and fair account of a company’s GHG emissions (see The Greenhouse Gas Protocol: A Corporate Accounting and Reporting Standard developed by the World Resources Institute and the World Business Council for Sustainable Development). CDP suggests that all of these principles be adopted for the purpose of water reporting. These principles are as follows:

- Relevance: Ensure the water use inventory appropriately reflects actual water use and serves the decision-making needs of users – both internal and external to the company.

- Completeness: Account for and report on all water activities within the chosen inventory boundary. Disclose and justify any specific exclusion(s).

- Consistency: Use consistent methodologies to allow for meaningful comparisons of company’s use of water over time.

- Transparency: Address all relevant issues in a factual and coherent manner, based on a clear audit trail. Disclose any relevant assumptions and make appropriate references to the accounting and calculation methodologies and data sources used. Transparently document any changes to the data, inventory boundary, methods, or any other relevant factors in the time series.

- Accuracy: Ensure the quantification of water use is sufficiently accurate to enable users to make decisions with reasonable assurance as to the integrity of the reported information.

Information is considered relevant if it contains the detail that users, both internal and external to the company, need for their decision-making. When considering what to disclose, please identify and report information that is likely to be of use and benefit to the audience requesting it (for example, the investment community and your customers).

Instructions for responding to the water security questionnaire

1. Units: Volumes must be reported in megaliters per year (1 megaliter = 1 million liters or 1,000 m3) in all questions, unless otherwise stated.

2. Blank cells: Please ensure that fields and cells in tables are only intentionally left blank if you have no data to disclose. Blank cells are interpreted as non-disclosure, i.e. information is not available due to lack of measurement or choosing not to disclose. They are therefore awarded no points by the scoring methodology.

3. Values of zero: Entering a 0 (zero) figure implies that a measurement has been made, and the value being disclosed is 0(zero).

4. Data accuracy: CDP recognizes that there may be uncertainty linked to data – this can arise from data gaps, assumptions, metering/measurement constraints including equipment accuracy etc. CDP allows estimated data to be submitted. However, an emphasis is placed on reporting transparently and this means that companies should always provide an explanation when its reported data is not accurate and detail the uncertainty (use the “please explain” or “comment” columns provided in the question).

5. River basins: From the drop-down list in specific questions, select the river basin associated with the disclosure, or select “Other, please specify” and provide the name of the river basin. CDP’s dropdown list of river basins aligns with the CEO Water Mandate’s Interactive Database of the World’s River Basins. For companies operating in South Africa, the list also includes the nine Water Management Areas for South Africa (see CDP’s Appendix: River basin list — and South African Water Management Areas — by country).

You may wish to enter a sub-basin of a listed river basin. In this case use the “Other, please specify” option in the following format: “Putumayo, Amazon”.

For companies withdrawing water from large confined aquifers that do not discharge to the river basin they are located in, e.g. Ogallala aquifer in the United States, please select “Other, please specify” and type in the name of the local aquifer source.

If you do not know the river basin associated with the data you are disclosing, the following tools have the functionality to identify the river basin locations of facilities by typing in geolocation coordinates, for example:

- The CEO Water Mandate Interactive Database of the World’s River Basins

- The Water Footprint Assessment Tool developed by the Water Footprint Network (WFN)

- The Water Risk Filter developed by WWF and DEG

- The WRI Aqueduct Water Risk Atlas Tool developed by the World Resources Institute (WRI)

- The Global Water Tool developed by the World Business Council for Sustainable Development (WBCSD)

W0 Introduction module

Module Overview

This module requests information about your organization’s disclosure to CDP and will help data users to interpret your responses in the context of your business operations, timeframe and reporting boundary.

The information provided here should apply consistently to your responses throughout the questionnaire and be complete and accurate as it may determine response options presented in subsequent modules.

For this reason, you should respond to every question in this module and save your response before accessing the rest of the questionnaire.

Key changes

- New question asks companies to state the countries in which they operate.

- New question asks companies to state the currency in which they will disclose financial figures. This is to standardize all financial information you provide.

- New questions for high-impact sectors.

Sector modifications

- Additional questions for: Chemicals, Electric Utilities, Food, Beverage & Tobacco, Metals & Mining, Oil & Gas.

Pathway diagram - questions

This diagram shows the general questions contained in module W0. To access question-level guidance, use the menu on the left to navigate to the question.

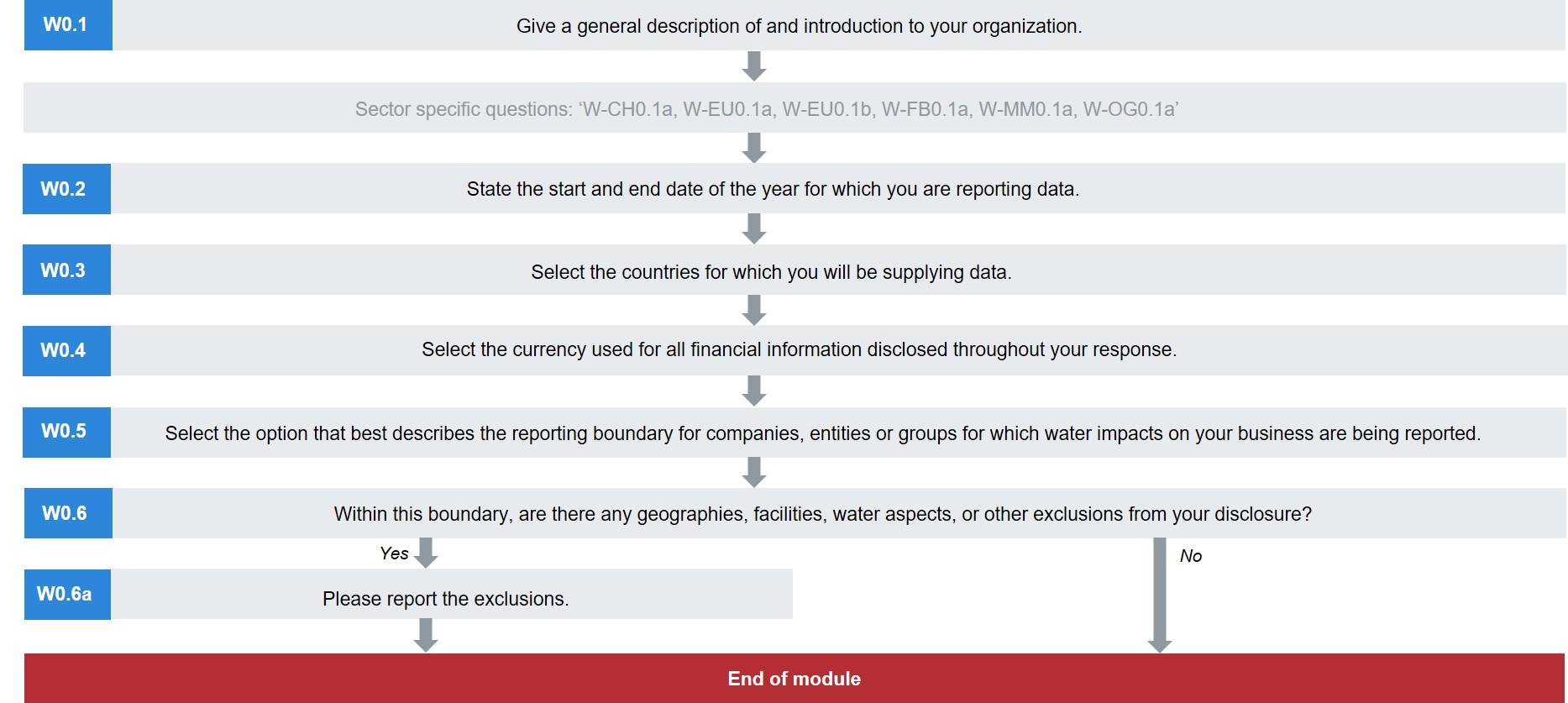

Introduction

(W0.1) Give a general description of and introduction to your organization.

Change from 2017

No change (2017 W0.1)

Rationale

This will help data users interpret your responses within the context of your business activities and sector.

Response options

This is an open text question with a limit of 5,000 characters.

Please note that when copying from another document into the disclosure platform, formatting is not retained.

Requested content

General

- Provide information about your operations and business activities to help data users understand your business and how it relates to water risk and corporate strategy. This information provides context for your answers throughout this disclosure.

Explanation of terms

- Organization: Throughout this information request, “your organization” refers collectively to all the companies, businesses, other entities or groups that fall within the definition of your reporting boundary (provided in W0.5). This term is used interchangeably with “your company”, but CDP recognizes that some disclosing organizations may not consider themselves to be, or be formally classified, as “companies”.

(W0.2) State the start and end date of the year for which you are reporting data.

Change from 2017

No change (2017 W0.2)

Rationale

This will help data users interpret your responses in relation to the timeframe reported.

Response options

Please complete the following table:

| Start date

|

End date

|

|

From: [MM/DD/YYYY]

|

To: [MM/DD/YYYY]

|

Requested content

General

- Apply this reporting year to your answers for the entire questionnaire.

- If you are using the Export/Import functionality, please check that the imported date is correct.

- The current reporting year is the most recent 12-month period for which data is reported.

- The investment community generally prefers a company's disclosure period to match the fiscal year for their financial jurisdiction. This facilitates the assessment of environmental performance data in alignment with their financial performance data.

- CDP recommends companies provide a year for which they have complete data for their response if possible. If you do not have data for the entirety of your reporting year, you have the option to extrapolate or estimate your data to cover the entire reporting year.

(W0.3) Select the countries/regions for which you will be supplying data.

Change from 2017

New question

Rationale

This will help data users interpret your responses and enables the auto-population of country/region drop-down lists in subsequent questions.

Response options

Please complete the following table:

| Country/Region |

|

Select all that apply:

- Country/region drop-down list

- Other, please specify

|

Requested content

General

- Select all countries/regions in which you operate from the drop-down list provided.

- If your organization operates in an area not included in the drop-down list of countries/regions, please select “Other, please specify” to provide a country/region label. If adding more than one area, please separate with a comma. If you need a total of more than 40 characters, you should use the comment box by clicking on the “speech bubble” icon. When applicable, you will need

to include these additional areas in subsequent questions requesting that you

select a ‘country/region’.

(W0.4) Select the currency used for all financial information disclosed throughout your response.

Question dependencies

- All disclosed financial figures throughout the questionnaire will be in the same currency. The currency reported in this question will apply to all reported figures throughout this request.

Change from 2017

New question

Rationale

CDP encourages companies to report financial figures associated with impacts, risks, and opportunities. Establishing a single currency will facilitate the collection of comparable financial information. This will benefit investors and other data users when assessing the costs and benefits reported by your organization.

Response options

Please complete the following table:

Requested content

General

- The currency you select will be applied to all financial information and metrics reported in your disclosure.

- For example, if you select USD ($) here, this will determine the currency applied to the figure you give for ‘Financial impact’ reported in W2.1a.

(W0.5) Select the option that best describes the reporting boundary for companies, entities, or groups for which water impacts on your business are being reported.

Change from 2017

No change (2017 W0.3)

Rationale

This will help data users interpret how your responses relate to your business operations.

Response options

Select one of the following options:

- Companies, entities or groups over which financial control is exercised

- Companies, entities or groups over which operational control is exercised

- Companies, entities or groups in which an equity share is held

- Other, please specify

Requested content

General

- References in the questionnaire to “your organization” are to the entities within your organizational boundary for which you are providing information.

- This question asks you to define the organizational boundary for which you are supplying data. This indicates the way your organizational entities such as groups, businesses, and companies have been identified for inclusion within your reporting boundary. Please apply this definition consistently when responding to questions.

- The options in the drop-down for this question are based on the GHG Protocol Corporate Standard:

- Financial control: An organization has financial control over an operation if it has the ability to direct the financial and operating policies of the operation with a view to gaining economic benefits from its activities. Generally, an organization has financial control over an operation for GHG accounting purposes if the operation is treated as a group company or subsidiary for the purposes of financial consolidation.

- Operational control: An organization has operational control over an operation if it or one of its subsidiaries has the full authority to introduce and implement its operating policies at the operation.

- Equity share: Under the equity share approach, a company accounts for GHG emissions from operations according to its share of equity in the operation. The equity share reflects the economic interest, which is the extent of rights a company has to the risks and rewards flowing from an operation. Typically, the share of economic risks and rewards in an operation is aligned with the company’s percentage ownership of that operation, and equity share will normally be the same as the ownership percentage. Where this is not the case, the economic substance of the relationship the company has with the operation always overrides the legal ownership form to ensure the equity share reflects the percentage of economic interest. The principle of economic substance taking precedence over legal form is consistent with international financial reporting standards.

- Other, please specify: select this only if none of the other options apply. If you select this option, provide a label in the text field provided. If you need more than 40 characters to explain how your reporting boundary is defined, please use the comment box by clicking on the “speech bubble” icon.

- Note: throughout this information request, when calculating figures for corporate level reporting take a “consolidation approach”, unless stated otherwise. The information you provide throughout the information request should be one “consolidated” result, covering all of the companies, entities, or businesses within your reporting boundary and aggregating more granular data at facility/business level, for example. Please consistently apply this organizational boundary when responding to questions unless specifically asked for data about another category of activities.

- Note: in W0.6a you have the opportunity to explain any data you have excluded from the reporting boundary you select here.

Explanation of terms

- Company: throughout this information request, “your company” refers collectively to all the companies, businesses, organizations, other entities or groups that fall within you’re the definition of your reporting boundary. It is used interchangeably with "your organization".

- Organization: this term is used interchangeably with “your company”. CDP recognizes that some disclosing organizations may not consider themselves to be, or be formally classified, as “companies”.

- Reporting boundary: this determines which organizational entities, such as groups, businesses and companies, are included in or excluded from your disclosure. These may be included according to your financial control, operational control, equity share, or another measure.

(W0.6) Within this boundary, are there any geographies, facilities, water aspects, or other exclusions from your disclosure?

Change from 2017

Minor change (2017 W0.4)

Rationale

CDP seeks to share comprehensive and representative water data. If companies do need to exclude areas of their business from their disclosure, data users must be informed of the exclusions as this may affect their analysis.

Response options

Select one of the following options:

Requested content

General

- References throughout the questionnaire to “your organization” include all the entities within your reporting boundary for which you are providing information. Please apply this logic consistently when responding to questions. However, you may exclude particular geographies, business activities, and/or small facilities for which it is difficult to gather data when water impacts are sufficiently small. This also applies to selected water inputs/outputs.

- In all cases, the following principles of relevance and transparency must apply to all disclosures (adapted from the GHG Protocol):

- Relevance: Ensure the disclosure appropriately reflects the water use of the company and serves the decision-making needs of users – both internal and external to the company.

- Transparency: Address all relevant issues in a factual and coherent manner, based on a clear audit trail. Disclose any relevant assumptions and make appropriate references to the accounting and calculation methodologies and data sources used.

- Any groups, companies, businesses or organizations falling within your organizational boundary but not included in your disclosure should be reported in W0.6a.

- Note that in some questions, e.g. in the facility level water accounting section, we will ask you to provide data only for facilities where significant water risk has been identified, rather than all facilities within your reporting boundary.

Explanation of terms

- Facilities: “Facilities” may be used throughout this questionnaire as a broad term and not restricted to a particular site or grouping of fixed buildings and factories. For example, if your organization is in the extractive industries you might normally collate business information for assets or business units, and so you may wish to define ‘facility’ information in this way.

Additional information

The GHG Protocol states that an acknowledgement of all exclusions should be made each year to enhance transparency despite disclosure of the same exclusion in previous years. This ensures all data users are always aware of what data has been included in your response.

For further information on allowable exclusions, please refer to the GHG Protocol and the CDP 2018 Water Scoring Methodology.

(W0.6a) Please report the exclusions.

Question dependencies

- This question only appears if you select “Yes” in response to W0.6.

Change from 2017

Minor change (2017 W0.4a)

Rationale

CDP seeks to share comprehensive and representative water data. Data users need to be informed of exclusions that may affect their analysis.

Response options

Please complete the following table. You are able to add rows by using the “Add Row” button at the bottom of the table.

| Exclusion

|

Please explain

|

|

Text field [maximum of 2,500 characters]

|

Text field [maximum of 2,500 characters]

|

[Add Row]

Requested content

General

- Identify and explain when any of the following are being excluded from your disclosure:

- Geographical locations, e.g. low water usage or data limitations may make reporting infeasible for operations in a country or region;

- Activities, e.g. a product line, type of business process, or type of supplier, may be excluded due to limited data or reporting feasibility;

- Facilities may be excluded due to recent mergers, acquisitions and divestitures, outsourcing and in-sourcing of activities (smaller facilities for which it is not currently possible to track water use may also be considered for exclusion); and

- Water inputs and outputs, e.g. a company may use rainwater at some facilities but not track the quantity or quality of this source in which case the source may be considered for exclusion.

- Any groups, companies, businesses or organizations that fall within your organizational boundary but are not included in your disclosure.

- For all exclusions, clearly explain why they are not included in your disclosure. Provide a reasonable explanation as to how you arrived at this exclusion; e.g., as a result of a high-level risk scanning exercise.

Example response

| Exclusion

|

Please explain

|

| Distribution Centers

|

Our company has not yet implemented a system to track the water impact in its distribution centers. We expect this to be a small fraction of our total water consumption and provide little exposure to water risk. This will be incorporated from 2019.

|

| Offices

|

Small leased office spaces (fewer than 50 employees) where water use is minimal. It is provided through the lease and managed by our landlord.

|

W1 Current state Test 08Oct

Module Overview

The promotion of water security for all is supported when companies:

- reduce their dependency on fresh water sources and track their progress; this is additionally important where fresh water scarcity may pose water quality risks and impacts.

- collect and share volumetric data on their interactions with water resources.

- consider water throughout their value chain, beyond the fence-line of their direct operations.

Clean freshwater is becoming increasingly scarce, and this can impact operations relying on large volumes of water – either through absolute availability or through rising costs for water. The information in this module allows CDP data users to build a picture of the dependence of your direct operations and your wider value chain on sufficient amounts of water of a particular quality, currently and for future growth, and where in the value chain most dependence on water lies. To understand an organization’s resilience, it is important to understand the potential to reduce reliance on freshwater sources.

The questions allow your company to demonstrate how well it understands its corporate hydrology by providing information on the monitoring of relevant water aspects, and volumetric data on withdrawals - including withdrawals in water stressed areas, discharges, consumption, and recycling. CDP also requests companies to comment on their projections for water accounting data.

The module also asks about your engagement activity around water in your value chain and a rationale for it. In regions where water sources are highly restricted, your organization’s water consumption patterns can influence relations with other stakeholders and your access to water can be dependent on those relationships. Engagement can also identify opportunities, such as innovation in your supply chain to reduce dependency and in product design to reduce water-related impacts.

Investors use this current state information to better assess the adequacy, robustness and relevance of your water governance, management and stewardship activities, as well as your disclosure of your water risks and opportunities.

The information requested in sections W1.1 and W1.2 may help companies with their climate-related disclosures in line with the TCFD recommendations which recognise that a reliance on the availability of water exposes a company to climate-related, financial risk.

Note:

- Throughout the water security questionnaire, CDP has broadened the scope of questions about the supply chain to include other phases of the value chain. This will be particularly relevant to companies whose activities may be constrained or otherwise affected by water related issues beyond their direct operations and supply chains. It reflects a widening of company focus to, and greater investor interest in, risk exposure, opportunities and impacts within the value chain.

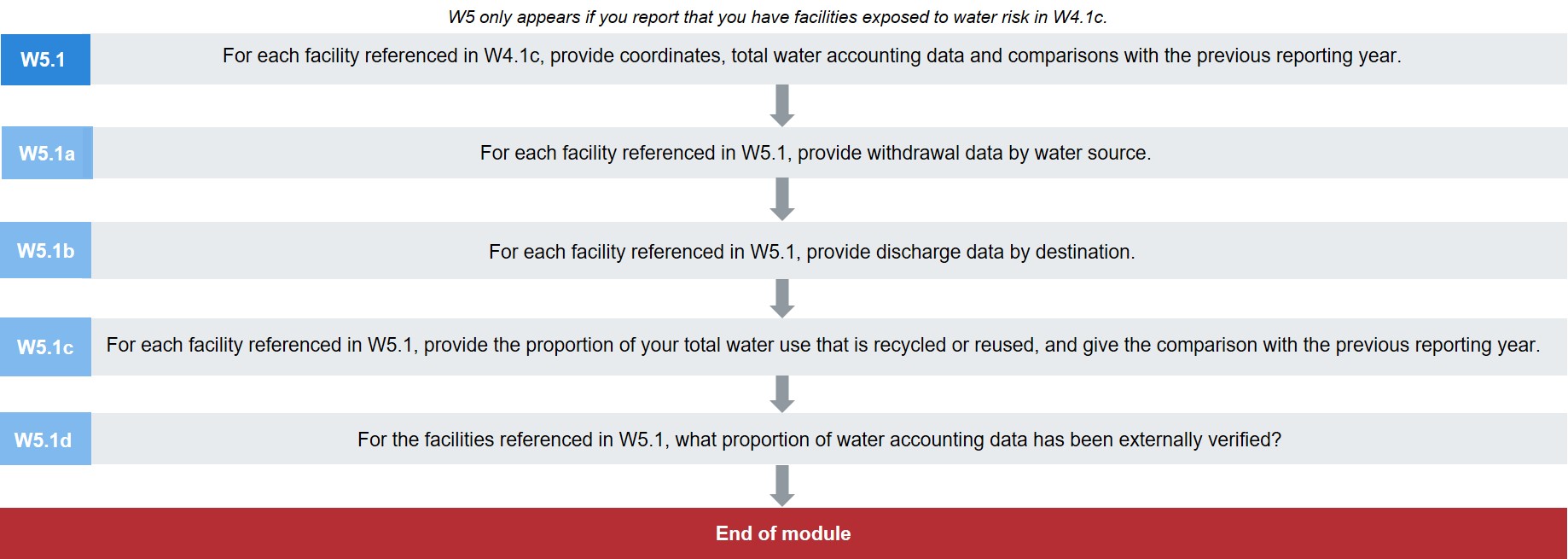

- W1.2 requests water accounting information at the corporate level. Module 5 asks for facility-level volumetric data - only for facilities that expose your organization to substantive financial or strategic risks, and so it is requested after you have reported your risk exposure in W4.

Disclosure note

CDP’s approach to reporting water accounting data

- When reporting volumetric data please read the guidance for each question as well as the CDP Technical Note on water accounting definitions.

- To reduce their impact on water ecosystems and resources as well as their need to manage water-related risks, organization should minimize and be able to account for all their interaction with water. For this reason, CDP’s focus is the collection of information to determine how well a company understands the flow of water into and out of its boundaries, and whether they have robust monitoring and accounting in place for all aspects of their water use.

- Definitions: CDP is looking for comparable data, reported against a standard methodology/definition. To ensure the quality of our data and a fair scoring methodology, CDP definitions should be used for all disclosures. This is particularly relevant where there is a lack of standardization. Companies must not provide water accounting data that does not align with the definitions given. Please refer to CDP’s Technical Note on water accounting.

- Units: Volumes must be reported in megaliters per year (1 megaliter = 1 million liters or 1,000 m3) in all questions, unless otherwise stated.

- Blank cells: Please ensure when responding to these water accounting questions that cells are only intentionally left blank if you have no data to disclose. Blank cells are interpreted as non-disclosure, i.e. information is not available due to lack of measurement or choosing not to disclose, and are therefore awarded no points by the scoring methodology.

- Values of zero: entering a zero implies a measurement has been made, and the value is zero. For example, a value of zero consumption reported indicates that no water is incorporated into products or waste products or lost by evaporation from the company. Do not use a zero to indicate a lack of data. If a company enters a zero for discharge, it should provide an explanation.

- Data accuracy: CDP recognizes that there may be uncertainty linked to water accounting information that could impact on data accuracy. Uncertainty can arise from data gaps, assumptions, metering/measurement constraints including equipment accuracy, data management, etc. The emphasis should be on reporting transparently and on providing an explanation for why reported data is uncertain or wholly or partially estimated or modelled, rather than sourced from direct measurements.

Key changes

- Revised definitions - refer to CDP’s Technical Note on water accounting.

- Section heading changed from ‘Context’ to ‘Dependence’ as this provides information on how dependent a company’s activities are on water resources. Furthermore, the term ‘context’ is being increasingly used to signify the local nature of water issues and the need to take account of specific contextual information when addressing water challenges.

- W1.1 - ‘Indirect use’ now refers to all stages of the value chain.

- W1.2b – ‘Total volumes’ for water withdrawals, discharges and consumption are reported together.

- New questions in section W1.2 on withdrawals from stressed areas, and recycling and reuse.

- New section W1.3 requests water intensity information from companies requested to respond to a CDP sector questionnaire.

- Section W1.4 on value chain engagement replaces the 2017 “Supplier reporting” section.

Sector modifications

- Additional questions presented for in section W1.1 for Food, Beverage & Tobacco, and section W1.2 for Electric Utilities, Oil & Gas, Food, Beverage & Tobacco.

- Additional response options presented in W1.2 for Oil & Gas and Metals & Mining.

- Replacement questions presented for W1.2j for Oil & Gas and Metals & Mining.

- Section W1.3 requests water intensity information only for companies responding to CDP sector questions.

- Additional drop-down options presented in W1.4b for Food, Beverage & Tobacco.

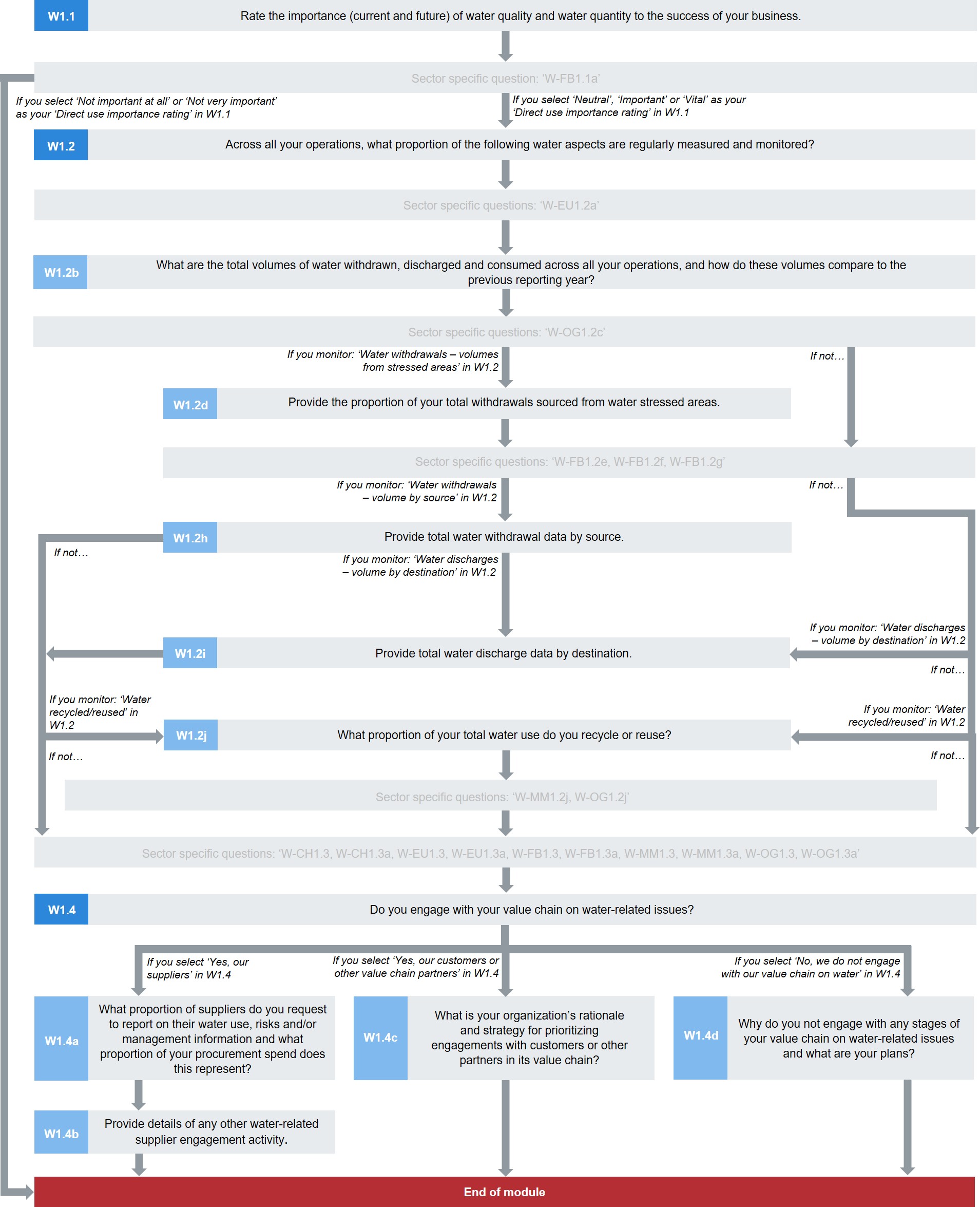

Pathway diagram - questions

This diagram shows the general questions contained in module W1. To access question-level guidance, use the menu on the left to navigate to the question.

Dependence

(W1.1) Rate the importance (current and future) of water quality and water quantity to the success of your business.

Question dependencies

- Your response to W1.1 prompts subsequent questions. If your response to W1.1 is amended, data in those dependent questions may be erased. In this case, be sure to re-enter data for all relevant questions. The guidance for each question indicates if it is a dependent question.

Change from 2017

Modified question (2017 W1.1)

Rationale

A dependence on good quality freshwater resources may pose a risk to companies where there is social, ecological or economic competition for those resources, or an otherwise unreliable supply. An ability to switch to using lower grade water mitigates that dependence, could improve a company’s water security and reduces pressure on freshwater sources.

This question asks companies to disclose their dependence on access to good quality freshwater as this could limit their ability to switch to using lower quality water without incurring a cost to the business through having to treat the water, for example.

Importance is independent of absolute volumes. For example, a company could require only a small amount of water used for an integral part of production for which access to alternative water sources could be restricted due to other local demands. The relative importance of access to that small volume would be considered as high.

Assessing how important access to good and lower quality water is to your organization is the first step to deciding how water-related issues may potentially present a risk to your company.

This information helps investors to understand why you have disclosed certain risks later in this questionnaire. It also demonstrates the ways that water could potentially constrain or enhance your business strategy.

Response options

Please complete the following table:

| Water quality and quantity

|

Direct use importance rating

|

Indirect use importance rating

|

Please explain

|

|

Sufficient amounts of good quality freshwater available for use

|

Select from:

- Not important at all

- Not very important

- Neutral

- Important

- Vital

- Have not evaluated

|

Select from:

- Not important at all

- Not very important

- Neutral

- Important

- Vital

- Have not evaluated

|

Text field [maximum 1,000 characters]

|

|

Sufficient amounts of recycled, brackish and/or produced water available for use

|

|

|

|

Requested content

General

- When answering this question, consider your organization’s dependence on good quality freshwater versus lower quality water and how this has changed or might change over time.

- ‘Good quality freshwater’ is any water used for your organization’s activities that must be of a quality requiring only minimal treatment to be acceptable for domestic, municipal or agricultural uses or safe for freshwater ecosystems. A company is considered dependent on this if it is not possible to use a lower quality water instead.

- ‘Importance’ should be considered in terms of the need for secure access to, and the availability at certain times of, an amount of water (large or small) that is sufficient for your operations; and not simply in terms of your net water consumption. So, activities involving large volumes of water would be expected to answer “Vital” or “Important” because large withdrawals would be required, even if discharges were also large resulting in relatively low consumption.

- Metals & mining sector only: Organizations dependent on freshwater of low quality (categories 2 and 3 of the Water Accounting Framework from the Mineral Council of Australia) should indicate this dependency in row 2 (…recycled, brackish and/or produced water sources). Dependency on low rather than high quality water reduces pressure on good quality freshwater sources.

Importance rating (columns 2-3)

- CDP recognizes that the importance ratings are subjective. The following description of the categories aims to assist with comparability rather than providing rigid definition and general examples are given.

- Vital: Water is of ‘vital’ importance when future production could be compromised, and output and finances affected at the corporate level, if the water supply was insufficient – either in terms of quantity and quality - in the locations of your production processes or your value chain. When water is vital for product use, scarcity may curtail sales or have reputational implications.

- Important: access to sufficient volumes and good quality water is required in direct or indirect operations, though these operations may not be water intensive and/or diversification of supply chain could mediate risk.

- Neutral: water quality can be poor as long as enough water is available.

- Not very important: water is not a key component of operations directly or indirectly but a local issue e.g. drought or poor water quality, or localized flooding may impact on local operations or supply chain. However, this would not affect the business overall.

- Not important at all: water is not a key component of operations directly or indirectly and water quantities in particular are of less concern.

- Have not evaluated: have not evaluated how much water or the quality of water required for operations and/or value chain.

- When considering the importance rating for indirect use, you should include the importance of water in all stages of your value chain that are upstream and downstream of your direct operations; e.g. within your supply chain, and also for the use/consumption of your products or services.

Please explain (column 4)

- State the primary use of water for both the direct and indirect parts of your value chain, for both good quality freshwater and lower quality options. Describe how water use is distributed across the value chain; giving percentages if possible.

- Describe how you have determined your stated importance ratings for water quality and quantity for both good quality and lower quality options.

- Specify how future water dependency is likely to differ from the current, and provide an explanation for your answer.

Explanation of terms